Publication number: ELQ-32326-1

View all versions & Certificate

Turn Overheads into Insight: Absorption Costing Model

A great tool for any manufacturer of goods. Produce per-unit costing and periodic pricing / volume analysis.

Why mastery of absorption costing matters for manufacturers

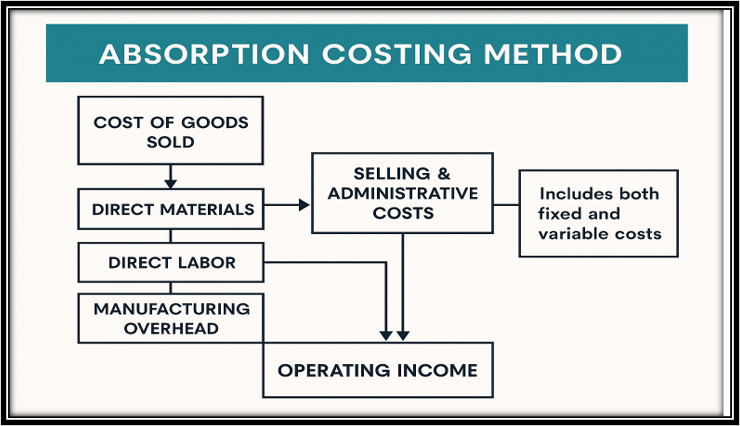

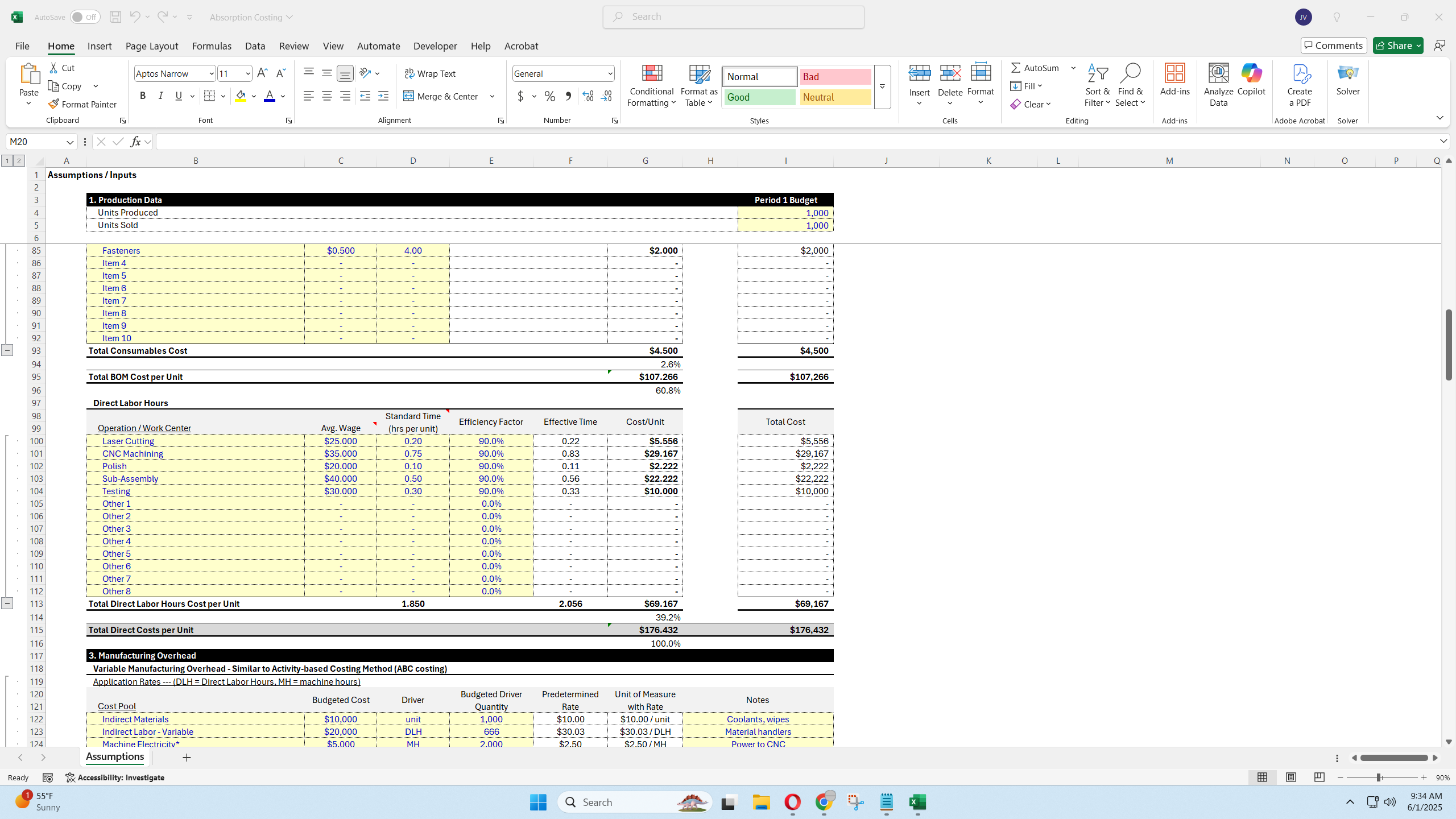

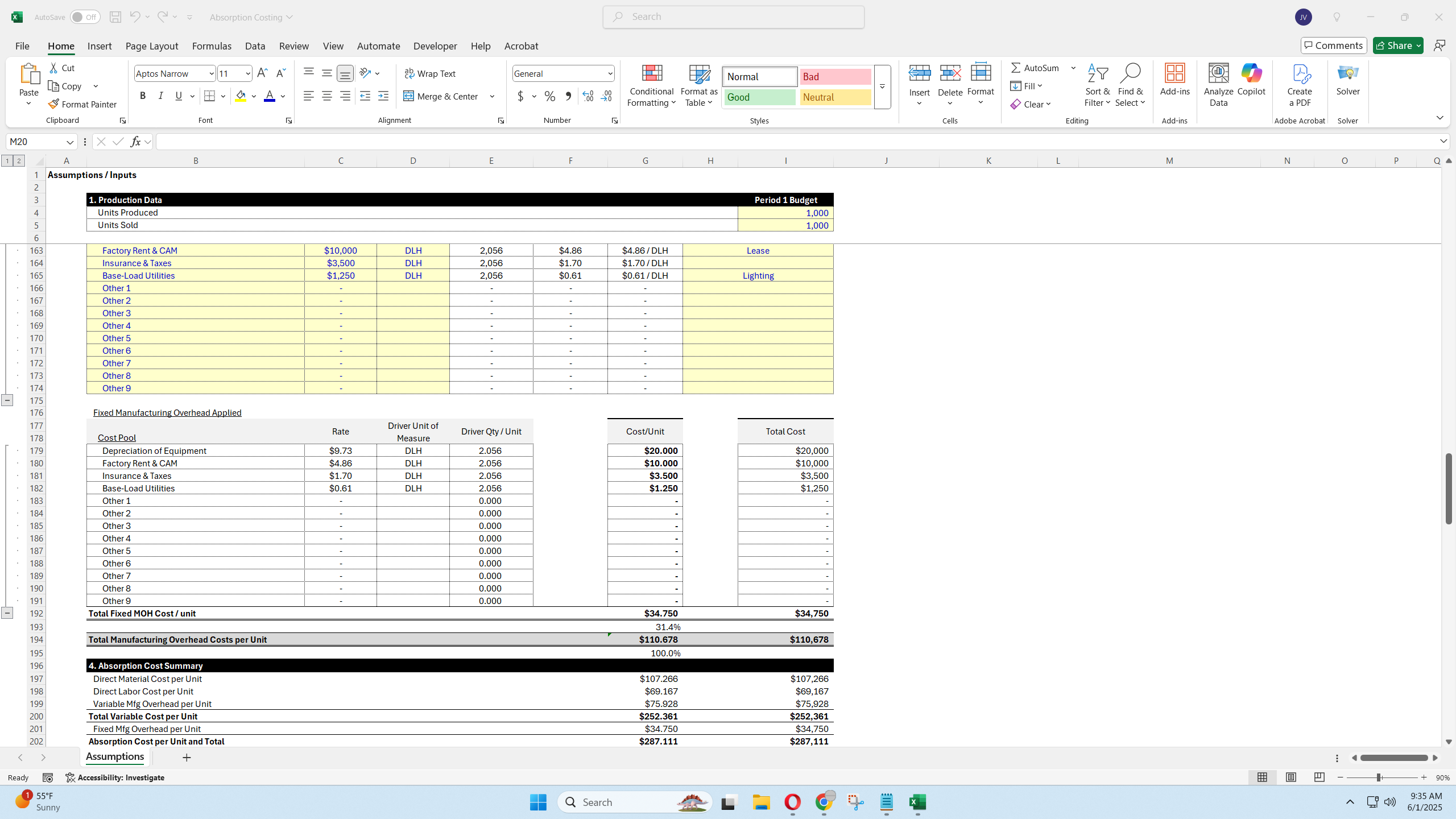

In absorption costing—sometimes called “full costing”—every manufacturing cost that is causally traceable to a finished good travels with that good until it is sold. Direct materials and direct labor are obvious inclusions, but less visible items such as machine maintenance, factory rent, depreciation, and quality-control salaries are also “absorbed” into inventory. Because U.S. GAAP and most global accounting standards require this treatment for external reporting, managers who misunderstand absorption costing risk misstating both inventory on the balance sheet and cost of goods sold (COGS) on the income statement. Beyond compliance, absorption costing reveals how unit economics shift with capacity utilization: as production volume rises, fixed‐overhead cost per unit falls, altering margin, pricing power, and capital-budget decisions.

Template benefits (college-level perspective)

Unified economic picture – The workbook collapses the entire cost build-up—from raw inputs to finished goods—into a single absorption cost per unit and per period. Students of managerial accounting will recognize this as converting the traditional “four-schedule cost of goods manufactured” statement into a dynamic model where one change propagates through the whole system.

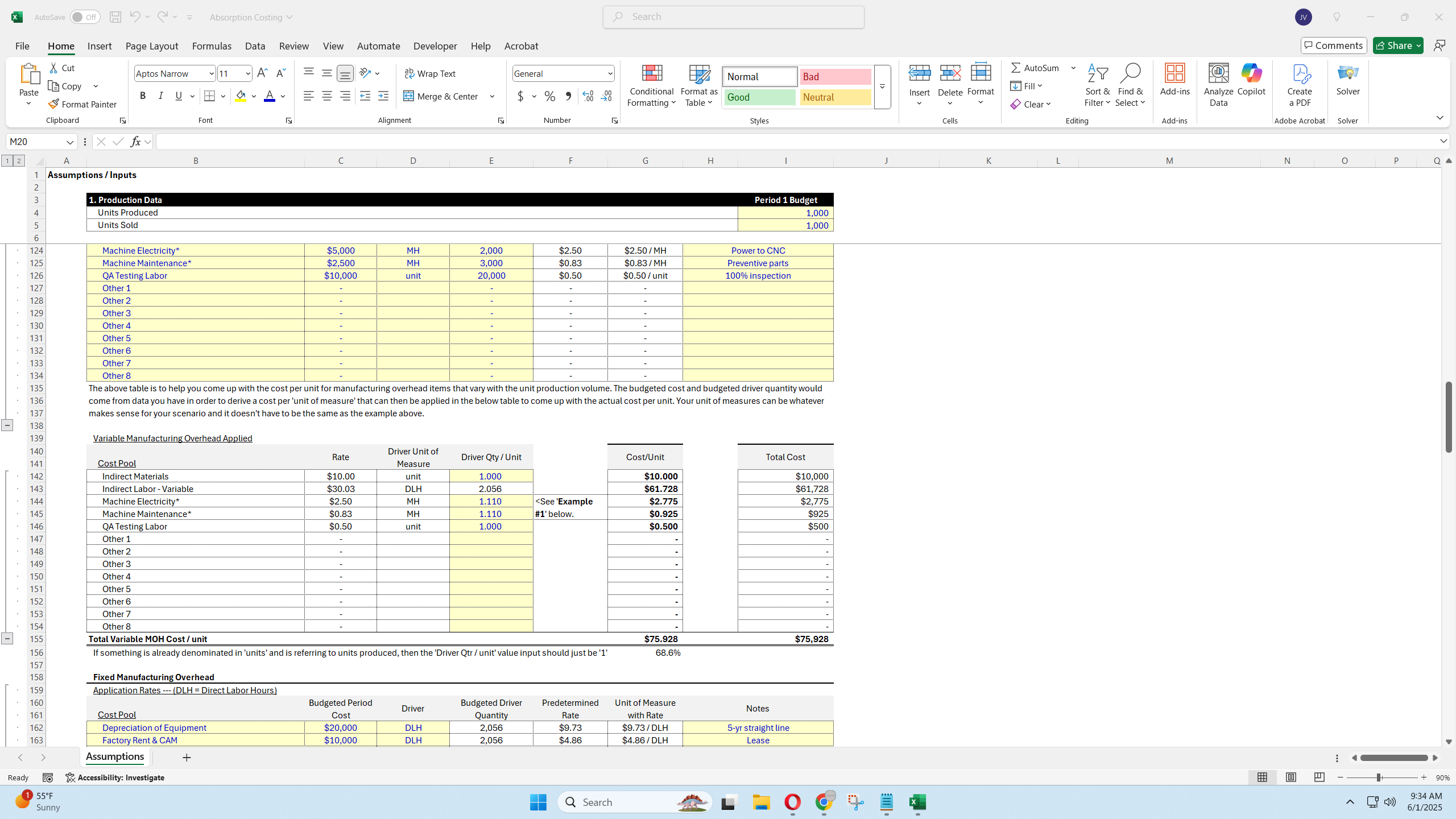

Driver-based overhead logic – Variable overhead items attach to cost drivers (e.g., direct-labor hours, machine hours), mirroring an activity-based-costing framework. This transforms what is often a flat percentage “loading” into a transparent, behaviorally sound allocation that cost‐accounting texts argue produces more accurate product costs and avoids cross-subsidization between high- and low-volume products.

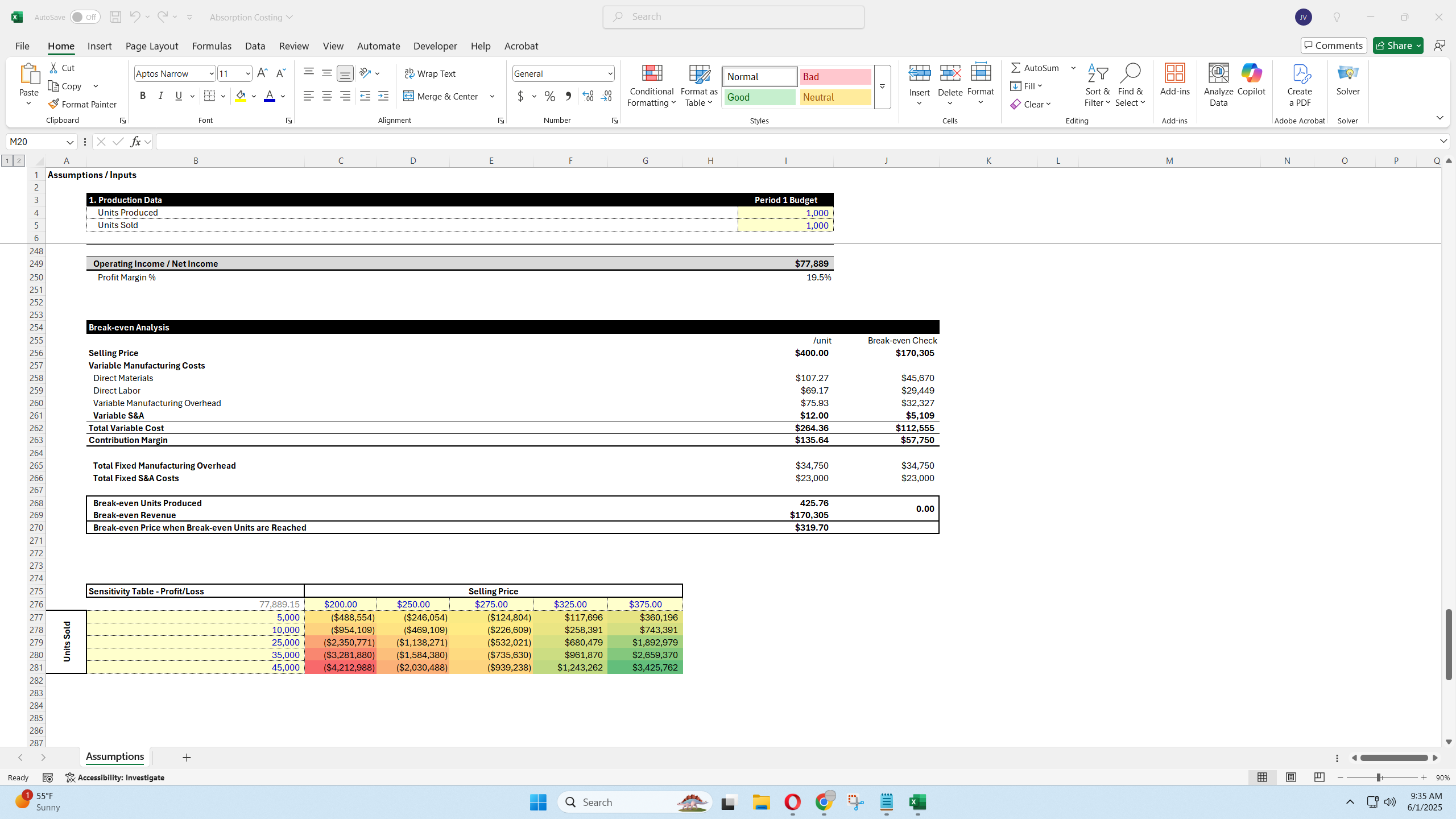

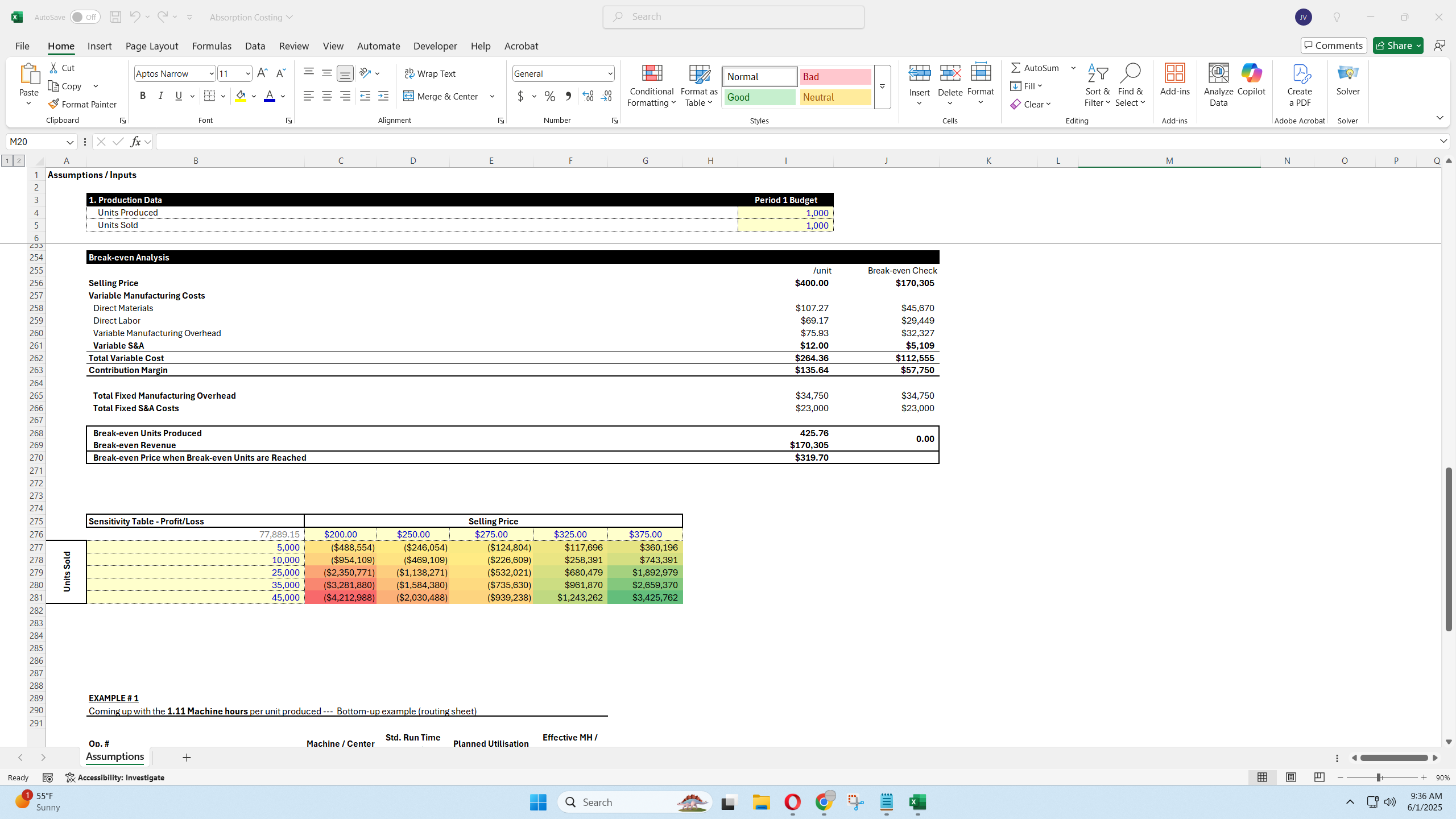

Embedded decision analytics – Break-even calculations and a two-way sensitivity table (selling price × units sold) convert historical cost data into forward-looking insights. Finance majors will immediately see the link to CVP (cost-volume-profit) analysis: the model shows how margin, operating leverage, and price elasticity interact without building a second spreadsheet.

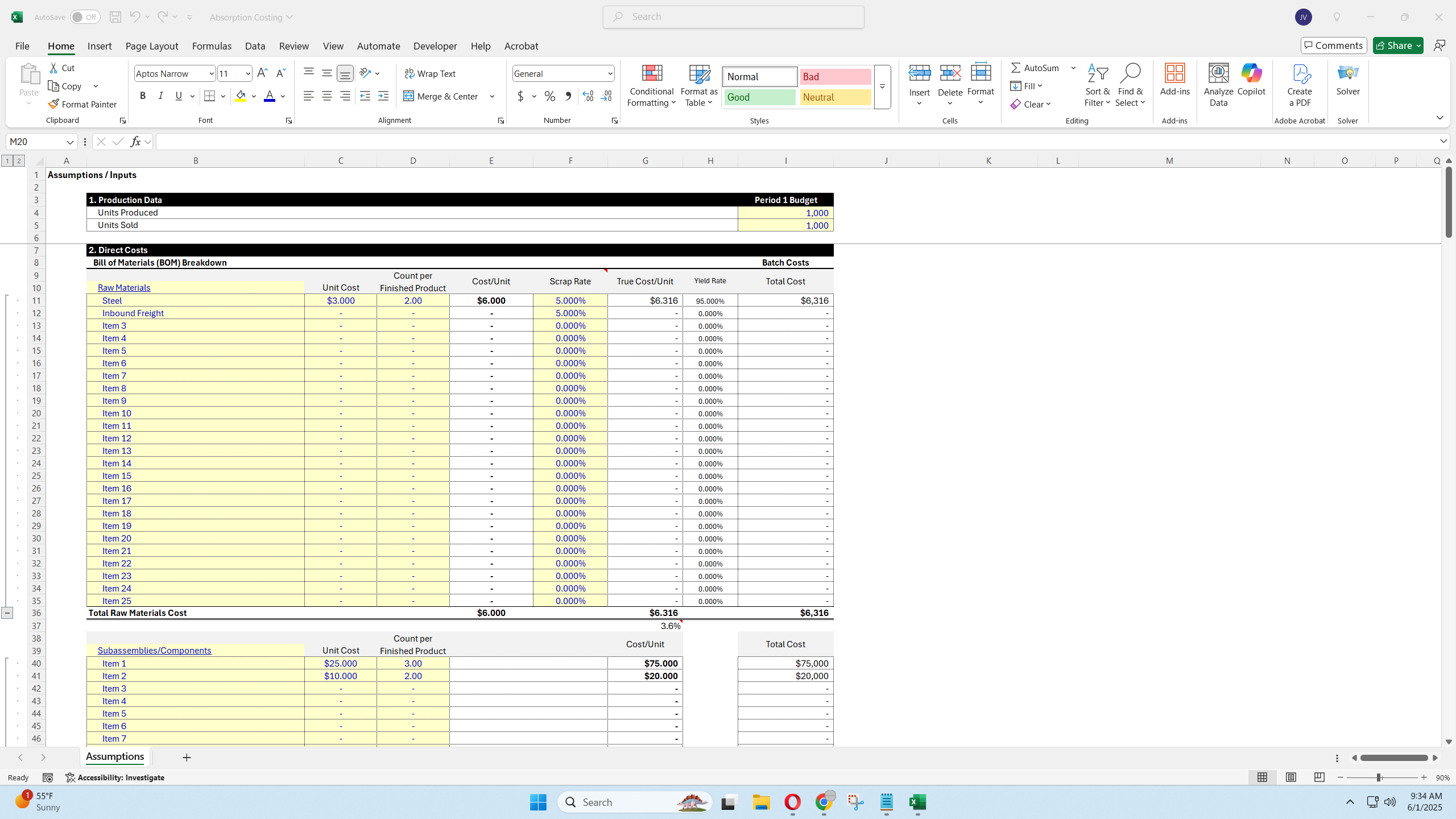

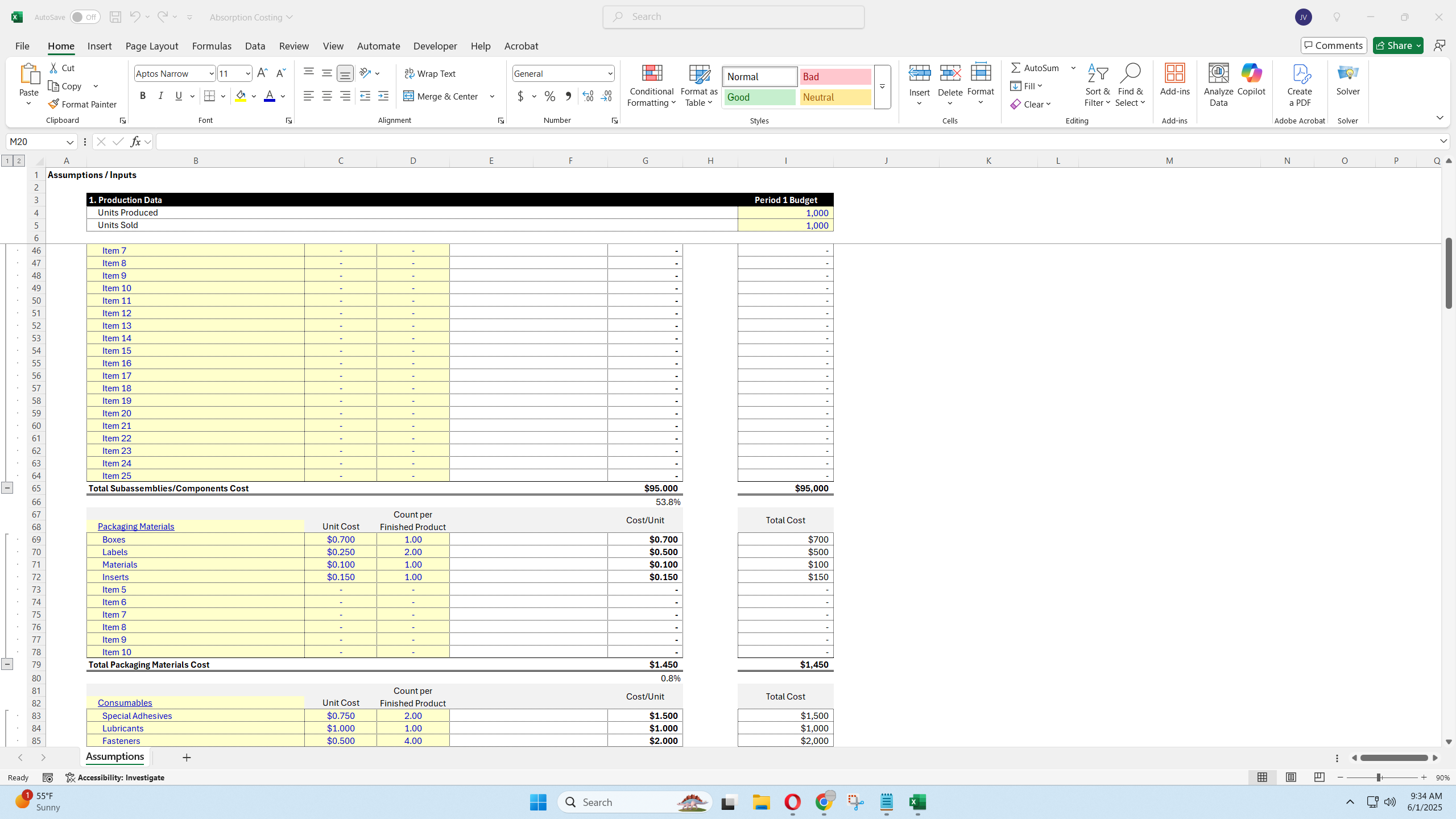

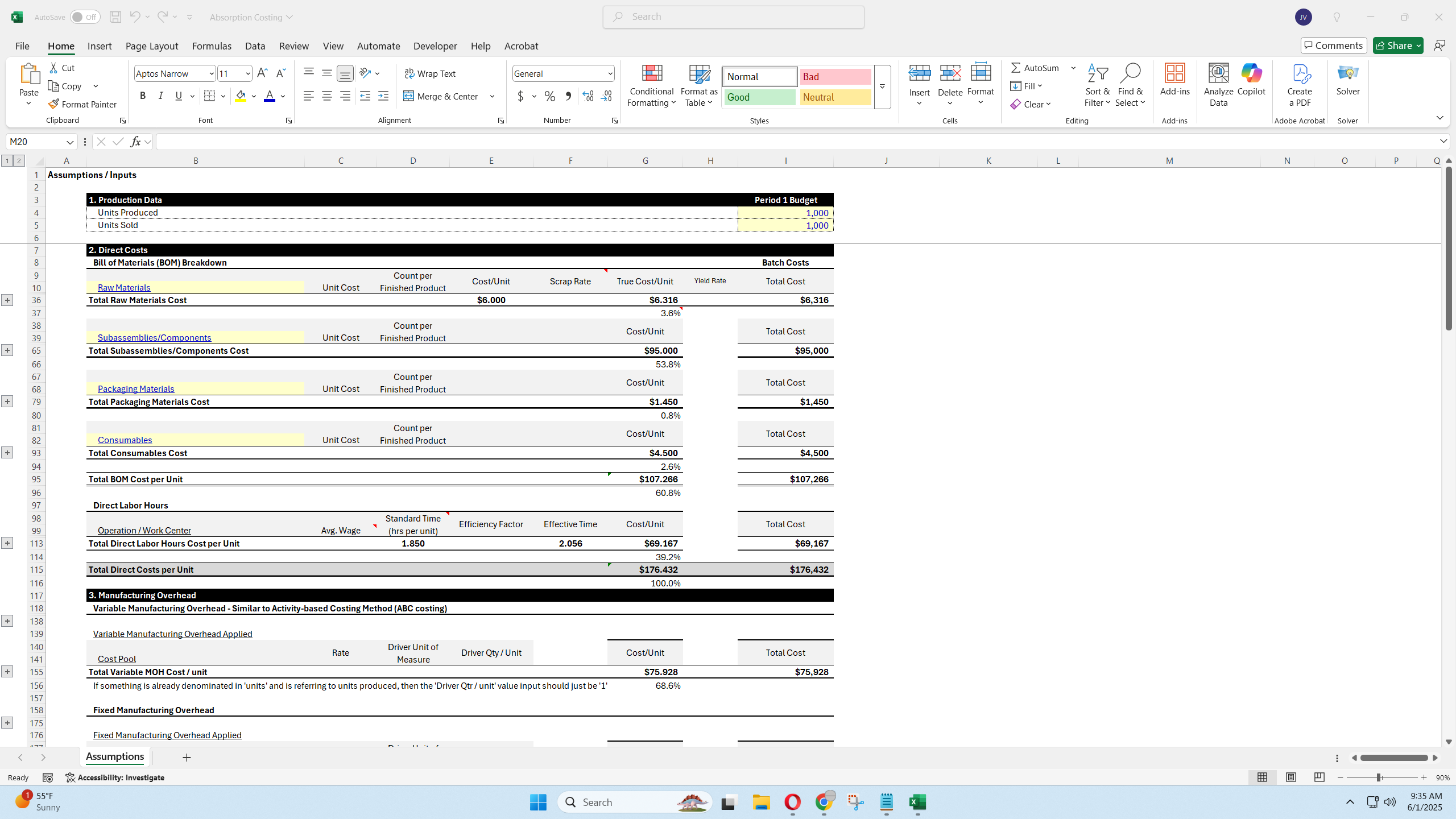

Populate the input blocks with your real-world data: material quantities and prices, standard labor hours, expected production volume, and detailed overhead budgets. Input cells are clearly color-coded, so users can add or subtract lines (for new materials, additional machine centers, etc.) without damaging formulas.

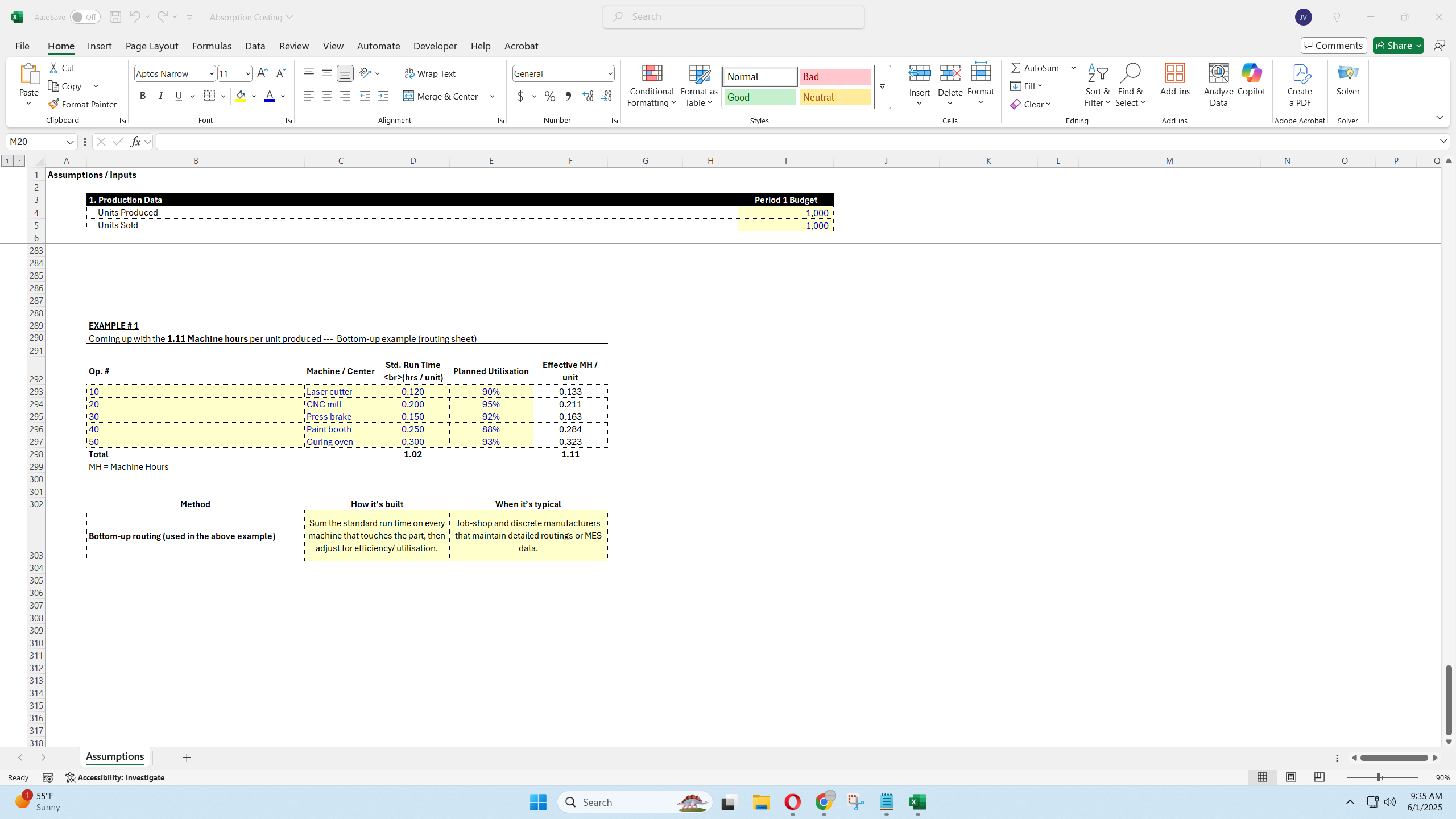

Validate the overhead cost drivers. For each variable overhead pool, choose the most behaviorally relevant driver—often the one that best explains cost variability in a regression or correlation test. Enter fixed overhead as period totals; the template automatically spreads these across units produced.

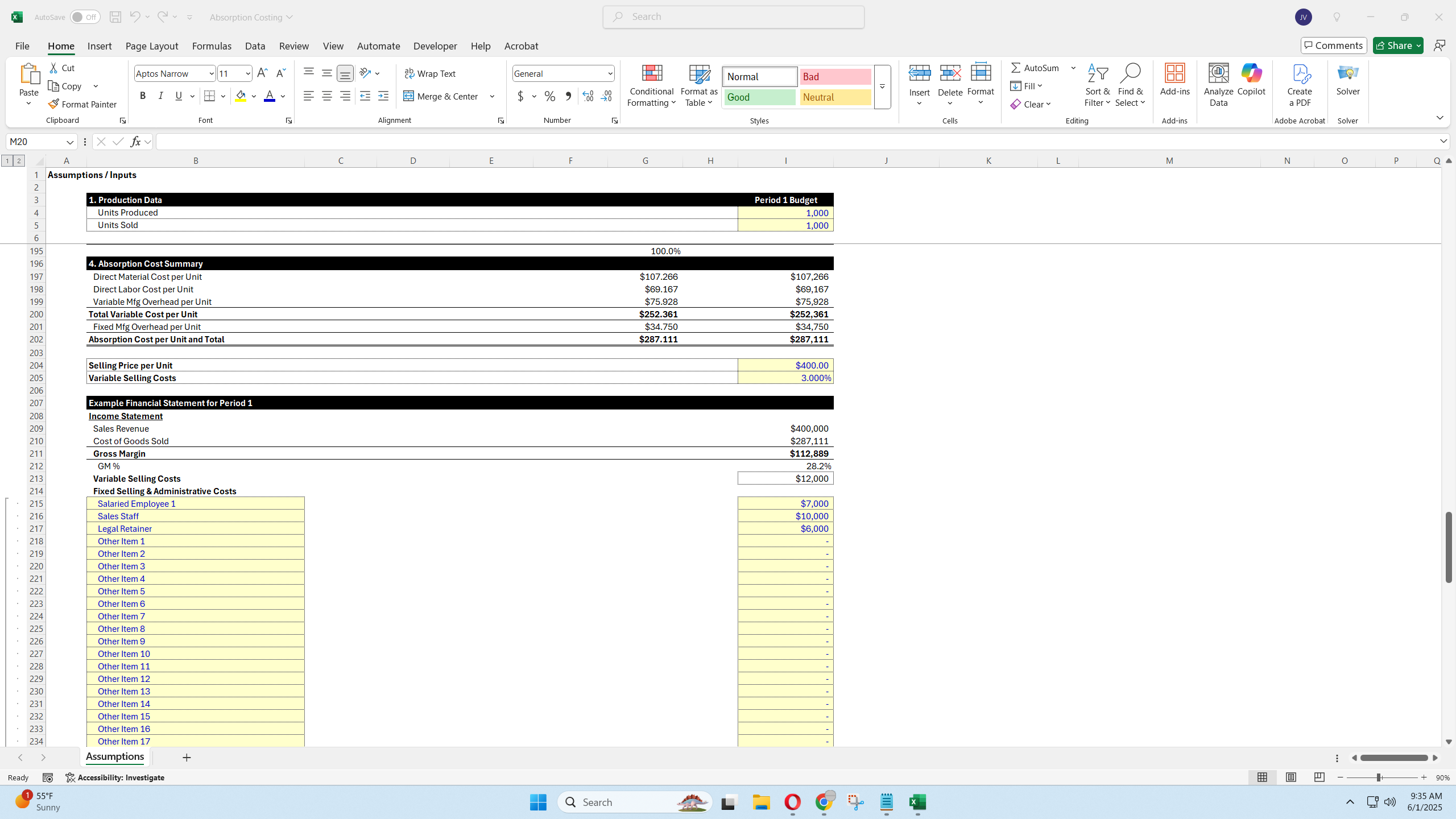

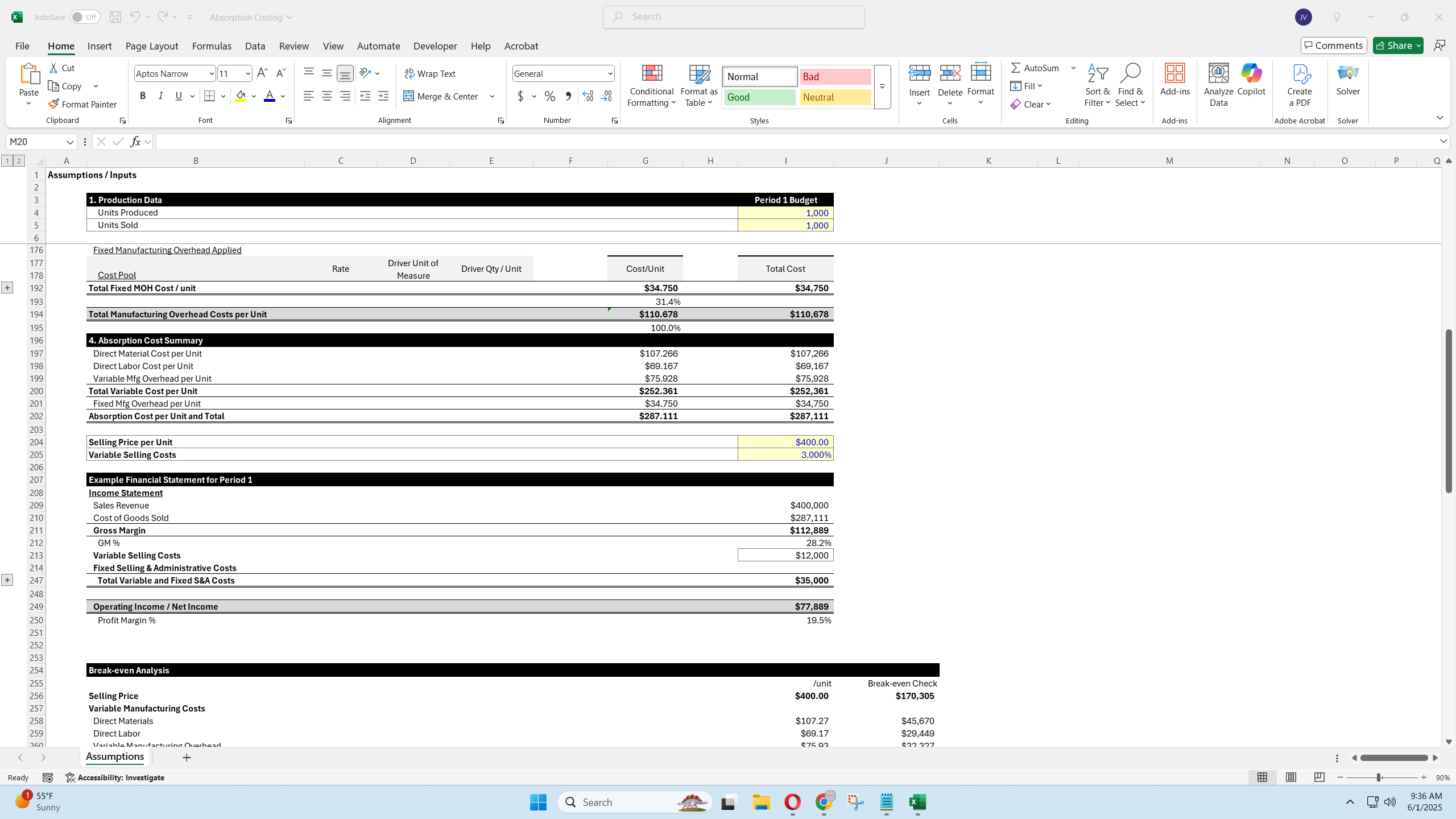

Interpret the automated outputs. The model instantly generates (a) absorption cost per unit, (b) GAAP-ready COGS and ending inventory figures, (c) break-even units, break-even revenue, and break-even price, and (d) a profit matrix that flexes price and volume. Use these for budgeting, pricing negotiations, “what-if” stress tests, or to supply auditors with traceable schedules.

Financial statement accuracy: Misallocating overhead can overstate inventory and understate expenses (or vice versa), leading to distorted gross margins and potential audit adjustments.

Strategic pricing and product-mix decisions: Knowing the full, properly absorbed cost floor prevents under-pricing and identifies when a product that appears profitable on a variable‐cost basis is actually eroding fixed-overhead coverage.

Capital investment evaluation: Absorption costing quantifies how fixed costs dilute with higher capacity utilization, which is a key variable in net present value (NPV) and internal rate of return (IRR) analyses when deciding whether to expand a plant or buy new equipment.

Performance measurement and incentives: Standard costing, variance analysis, and responsibility accounting all assume accurate absorption. If overhead is misapplied, managers’ bonuses may reward the wrong behaviors (e.g., maximizing production to absorb fixed costs rather than producing to demand).

In essence, this template operationalizes the theory you encounter in cost-accounting and managerial-finance courses: it bridges textbook concepts with the messy realities of manufacturing, giving both students and practitioners a reliable platform for decision-quality cost data.

Check out all the templates I've built and download the all-in-one bundle here.

This Best Practice includes

1 Excel model

Further information

Produce a full cost per unit analysis and run various pricing / volume / cost scenarios.

Built to analyze a single SKU type.