Originally published: 08/06/2020 07:12

Last version published: 18/09/2023 08:52

Publication number: ELQ-19581-2

View all versions & Certificate

Last version published: 18/09/2023 08:52

Publication number: ELQ-19581-2

View all versions & Certificate

Interim Budgeting (Reforecasting)

Tools to depict the mid-year status, estimate if the outlook looks reasonable and assess the accuracy of past forecasts

Further information

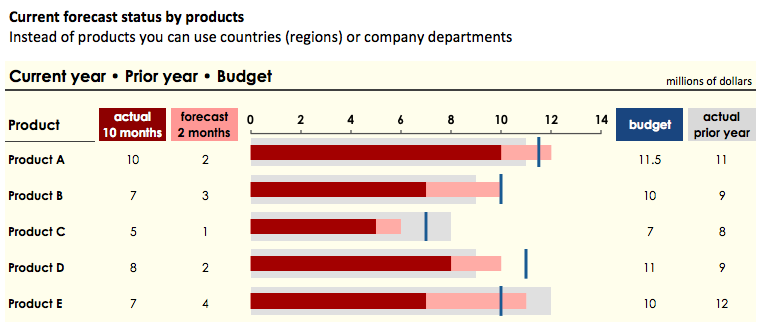

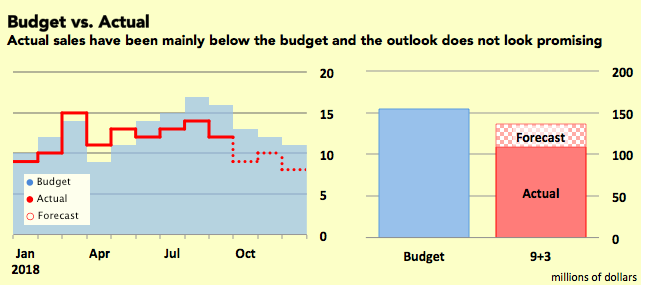

To provide additional analytics and visualisation for the on-going budgeting process

Interim budgets

n/a