Originally published: 22/03/2019 09:06

Publication number: ELQ-78808-1

View all versions & Certificate

Publication number: ELQ-78808-1

View all versions & Certificate

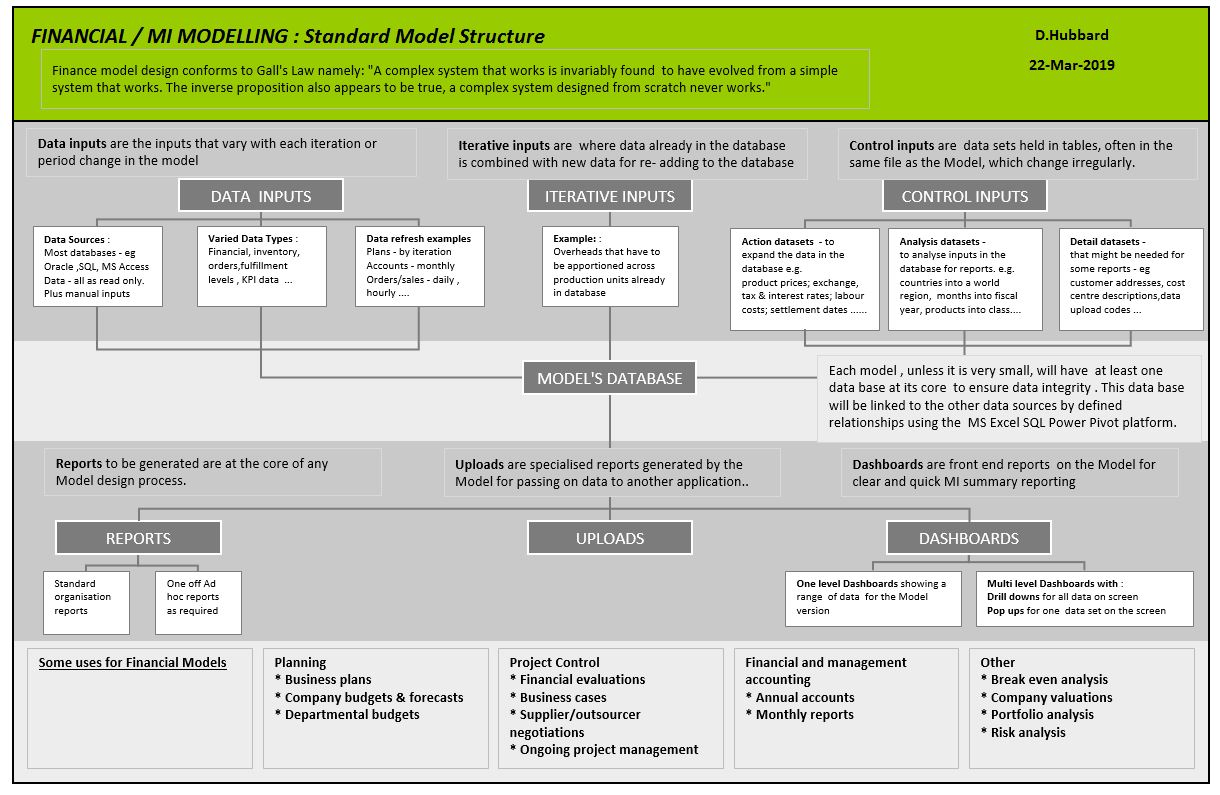

To Model or not to Model

A REFERENCE SHEET on why and how Finance Models are constructed