Originally published: 06/02/2025 08:00

Last version published: 06/05/2026 18:53

Publication number: ELQ-68004-2

View all versions & Certificate

Last version published: 06/05/2026 18:53

Publication number: ELQ-68004-2

View all versions & Certificate

Senior Living Real Estate Underwriting Model

Model the acquisition of a senior care facility, operations, and exit. Includes joint venture waterfall, two SBA loan options, and a REFI / exit configuration.

Description

Below is a high-level overview of a real estate underwriting model designed to accommodate both an SBA loan for the operating business and a real estate–specific SBA loan, while also allowing for a potential refinance (REFI) at a future date and an eventual exit. In addition, it features a joint venture waterfall structure with GP fees.

1. Purpose and Structure

Download over 200 of my templates in the all models bundle.

Below is a high-level overview of a real estate underwriting model designed to accommodate both an SBA loan for the operating business and a real estate–specific SBA loan, while also allowing for a potential refinance (REFI) at a future date and an eventual exit. In addition, it features a joint venture waterfall structure with GP fees.

1. Purpose and Structure

- Purpose

- Underwrite and analyze the financial feasibility of acquiring or developing real estate that also houses or supports an underlying operating business.

- Incorporate both an SBA loan for the business (often referred to as an SBA 7(a)) and a separate real estate–specific SBA loan (often an SBA 504).

- Evaluate multiple exit strategies: hold, refinance, or sell.

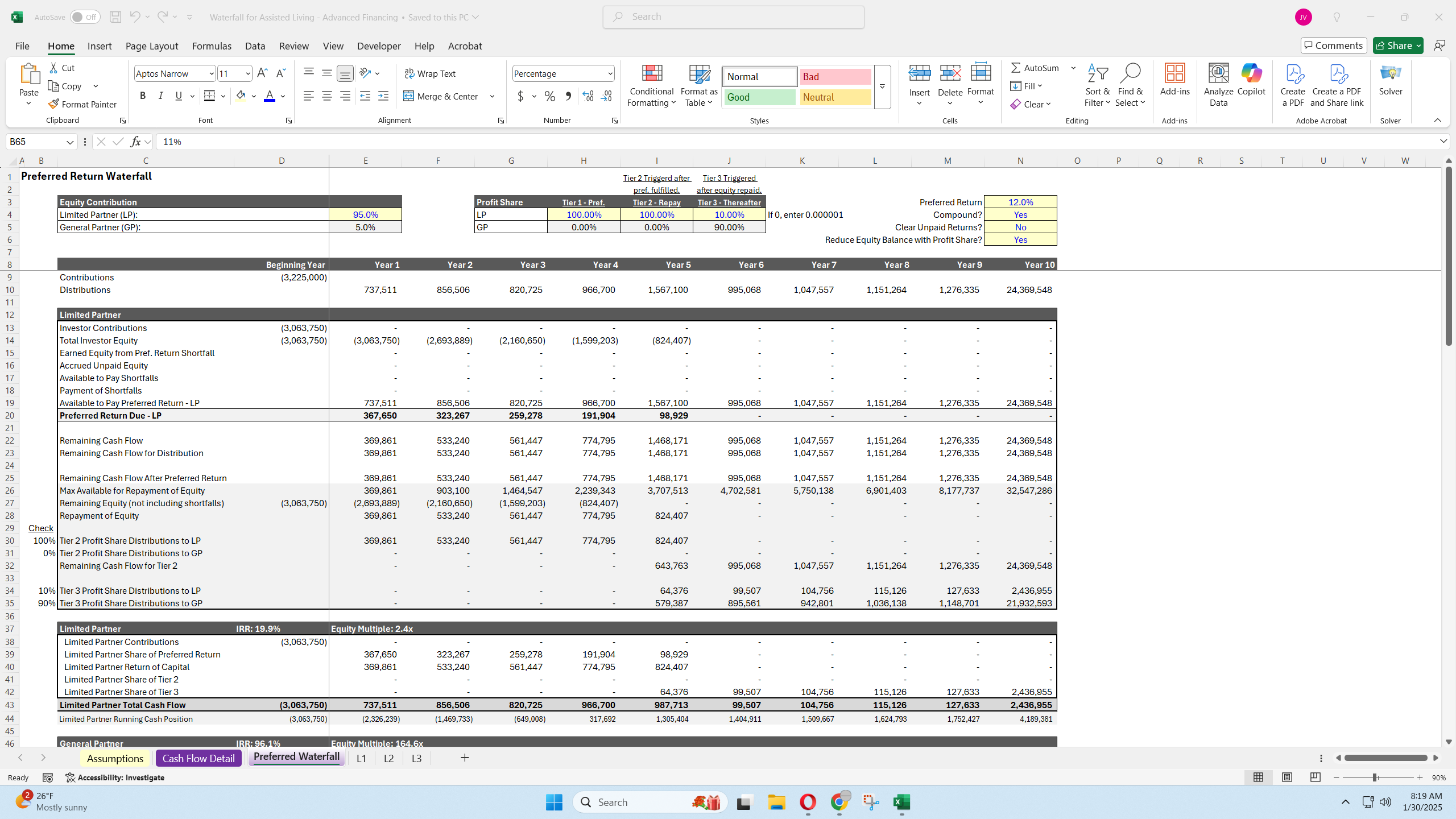

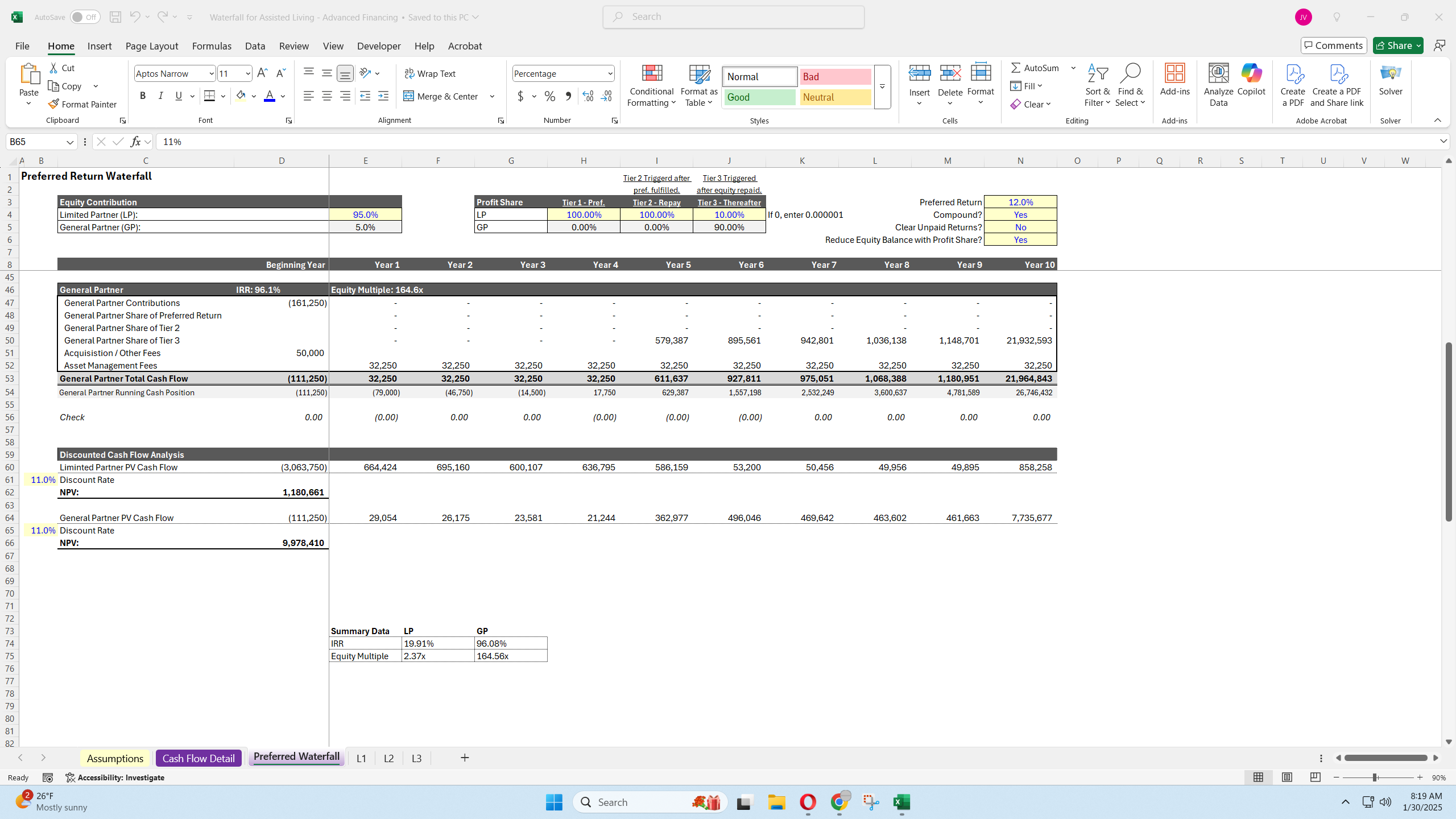

- Model distributions to investors using a joint venture waterfall with GP fees and promotes.

- Overall Structure

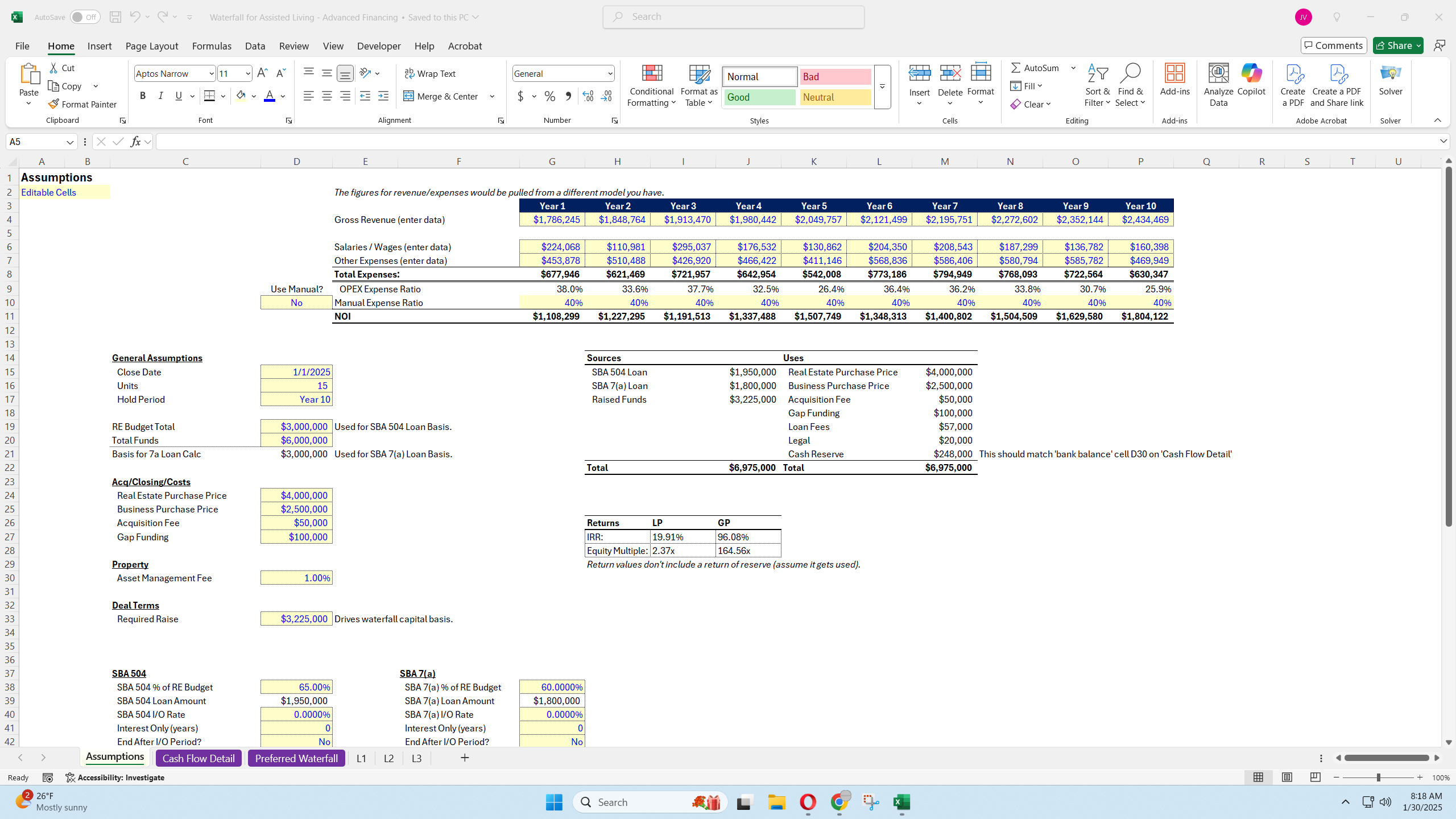

The model typically comprises multiple tabs or sections for:- Assumptions & Inputs

- Operating Business & Real Estate Revenues/Expenses

- Debt & Financing (SBA loans, conventional financing, etc.)

- Refinance & Exit Scenarios

- Cash Flow Waterfall (Equity distributions and GP fees)

- Summary Returns & Sensitivity Analysis

- Property-Level Inputs

- Revenue Projections: Lease income, rent escalations, or business revenue.

- Expense Assumptions: Operating expenses, property taxes, insurance, maintenance.

- Other Operating Metrics: Vacancy factors, reimbursements, tenant improvements, capital expenditures, etc.

- Business-Level Inputs

- Operating Business Revenue: Projected sales or revenue for the underlying business, if relevant to the SBA 7(a) loan.

- COGS / Operating Expenses: Direct costs, SG&A, etc.

- EBITDA / Net Cash Flow: Used to size the business portion of the SBA loan.

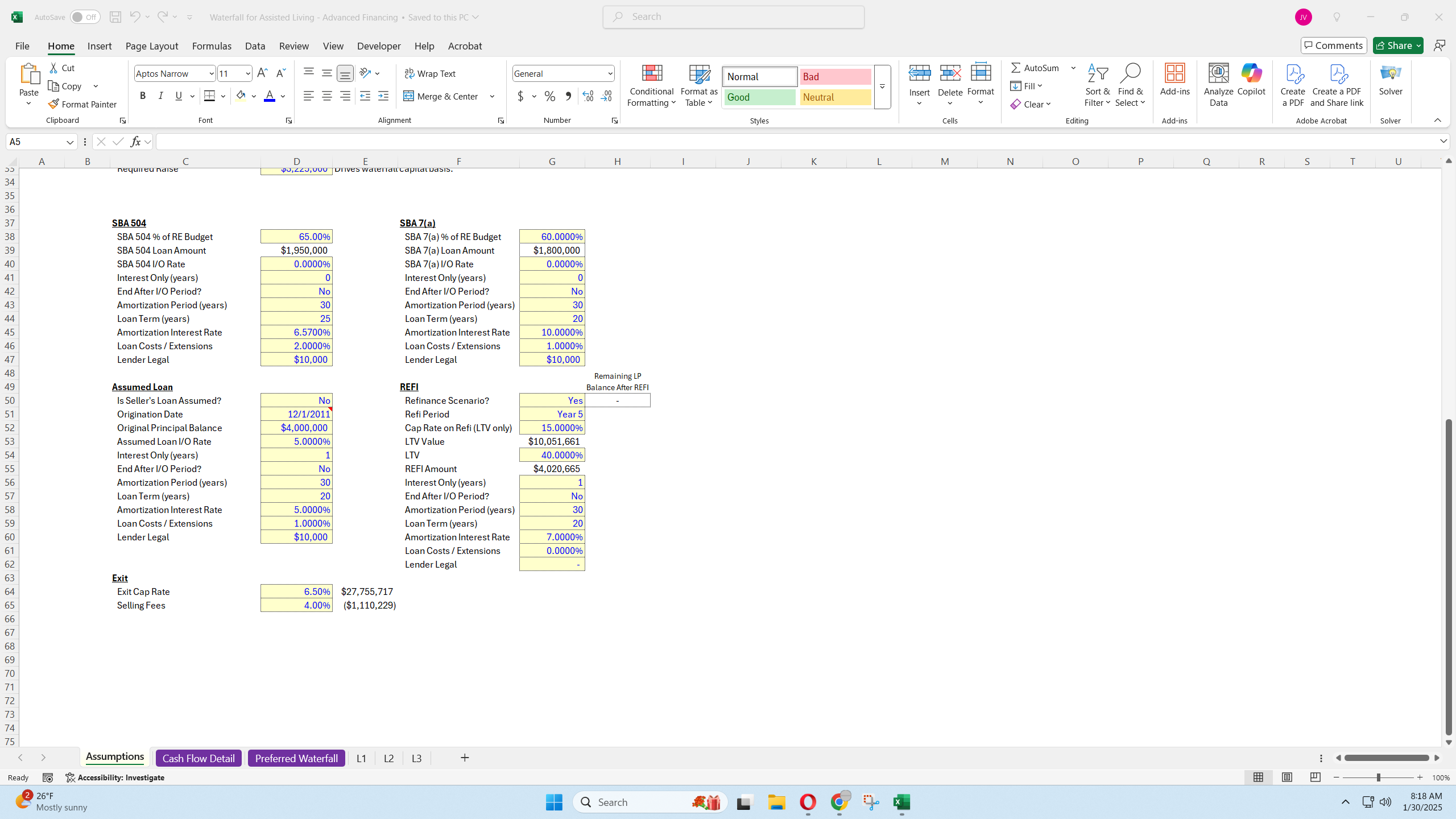

- Loan & Financing Assumptions

- SBA 7(a): Loan amount, interest rate, amortization term, fees, and coverage requirements.

- SBA 504 or Real Estate–Specific SBA Loan: Typically has two components (a bank portion and an SBA debenture). Inputs include interest rates, terms, and loan fees.

- Equity Injection: Minimum owner/operator equity required by SBA guidelines.

- Potential Conventional Debt: If the deal uses supplemental or mezzanine debt in addition to the SBA loans.

- Refinance & Exit Parameters

- Refi Timing: Assumed year of refinance (e.g., Year 5).

- Refi Terms: Loan-to-value (LTV) ratio, interest rate, amortization, and costs.

- Exit Cap Rate or Valuation Approach: Used to estimate sale proceeds if property is sold (e.g., dividing stabilized NOI by an exit cap rate).

- Sale Costs: Brokerage commissions, legal fees, etc.

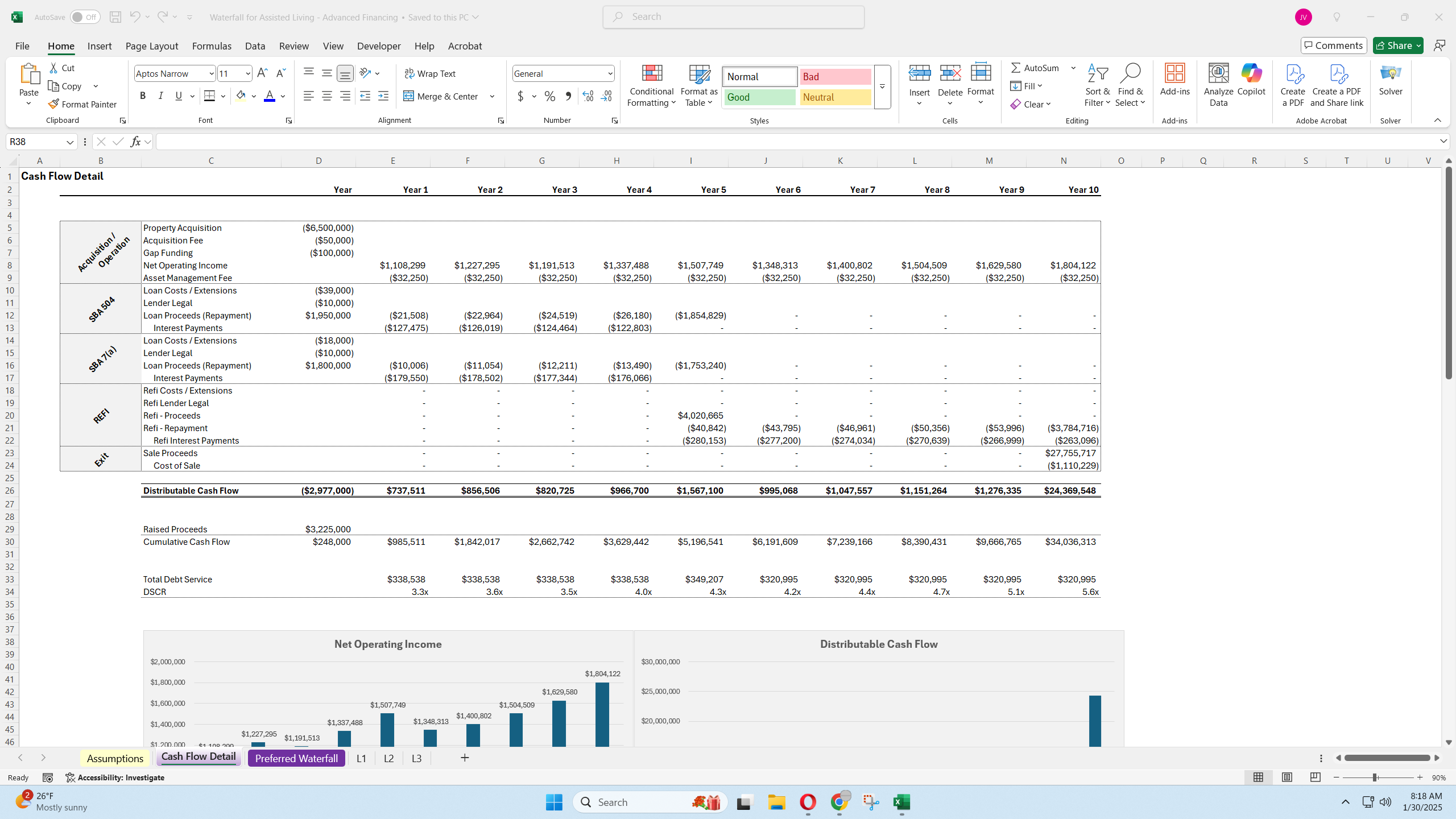

- Gross Revenue

- Include all potential property income (rent, reimbursements) and business income (if relevant to underwriting).

- Model annual growth rates or escalators.

- Operating Expenses

- Break out into categories (utilities, repairs, management fees, etc.).

- Apply an annual inflation factor or escalation percentage.

- Net Operating Income (NOI)

- Subtotal of revenue minus property operating expenses.

- Serves as a key figure for debt sizing, valuation, and refinance analysis.

- SBA 7(a) Loan (Business)

- Sized based on business cash flow (EBITDA or net income) and SBA requirements.

- Typically has longer amortization than conventional business loans, but is slightly more expensive in fees.

- May include covenants or coverage ratios that must be met.

- SBA 504 Loan (Real Estate)

- Usually split into two pieces: a bank loan (50% of project cost) and an SBA debenture (up to 40% of project cost), with at least 10% equity injection.

- The real estate portion’s NOI (plus any separate business occupancy coverage) must support this debt.

- Combining the Loans

- Ensure total combined debt service coverage meets both bank and SBA guidelines.

- If the real estate is owner-occupied (with the underlying business), the combined coverage from business and property cash flow may be considered.

- Timing & Assumptions

- Typically model a refi at or after a stabilization period (e.g., Year 5).

- Set an exit LTV, interest rate, and new loan terms (amortization, points, fees).

- Payoff of Existing Debt

- The new loan proceeds pay off any remaining principal balances on the SBA loans.

- The model calculates potential penalty costs or prepayment fees.

- Equity Recapture

- If the new loan is sized above the outstanding balance, some equity may be returned to investors or used for capital improvements.

- Impact on Cash Flows

- Post-refi, the model updates debt service costs based on the new interest rate and loan amount.

- This changes subsequent distributable cash flow and investor returns.

- Sale Timing

- Often aligned with or after refinance if the project’s goal is short- to mid-term hold.

- The model calculates the sale in a designated year (e.g., Year 5 or Year 10).

- Valuation

- Use projected NOI and an exit cap rate to determine gross sale proceeds.

- Deduct any closing costs, commissions, or loan payoff.

- Return to Investors

- Net proceeds (after transaction costs and debt payoff) flow into the distributions waterfall to calculate final returns.

- Waterfall Structure

- Preferred Return: Investors receive a preferred return on their contributed capital.

- Splits / Promote: After achieving certain preferred return, profits are split between LPs and the GP, often with increasing shares going to the GP as performance improves.

- GP Fees

- Asset Management Fee: Charged on revenue or equity.

- Acquisition Fee: One-time fee upon closing (percentage of the purchase price).

- Distributions Over Time

- Annual periods only.

- Upon refinance or sale, any large lump-sum proceeds are distributed through the waterfall model according to capital account balances, preferred returns, and promotes.

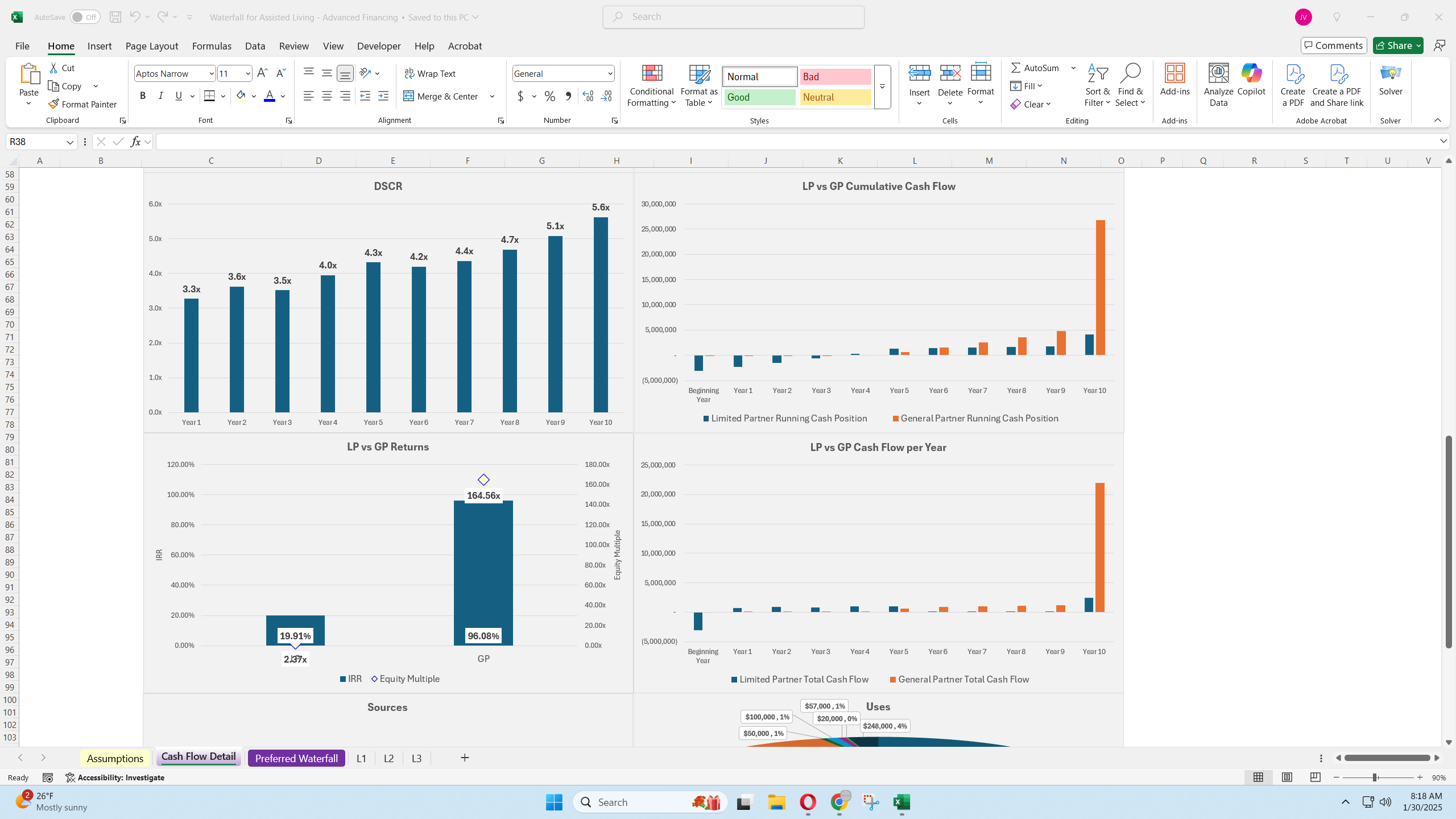

- Key Return Metrics

- IRR: Internal Rate of Return for both LP and GP.

- Equity Multiple: Total returns to equity over the investment horizon.

- Cash-on-Cash Return: Annual distributable cash flow / equity invested.

- Sensitivity Analysis

- Stress test changes in rent growth, exit cap rates, interest rates, and expenses.

- Evaluate impact on coverage ratios and returns.

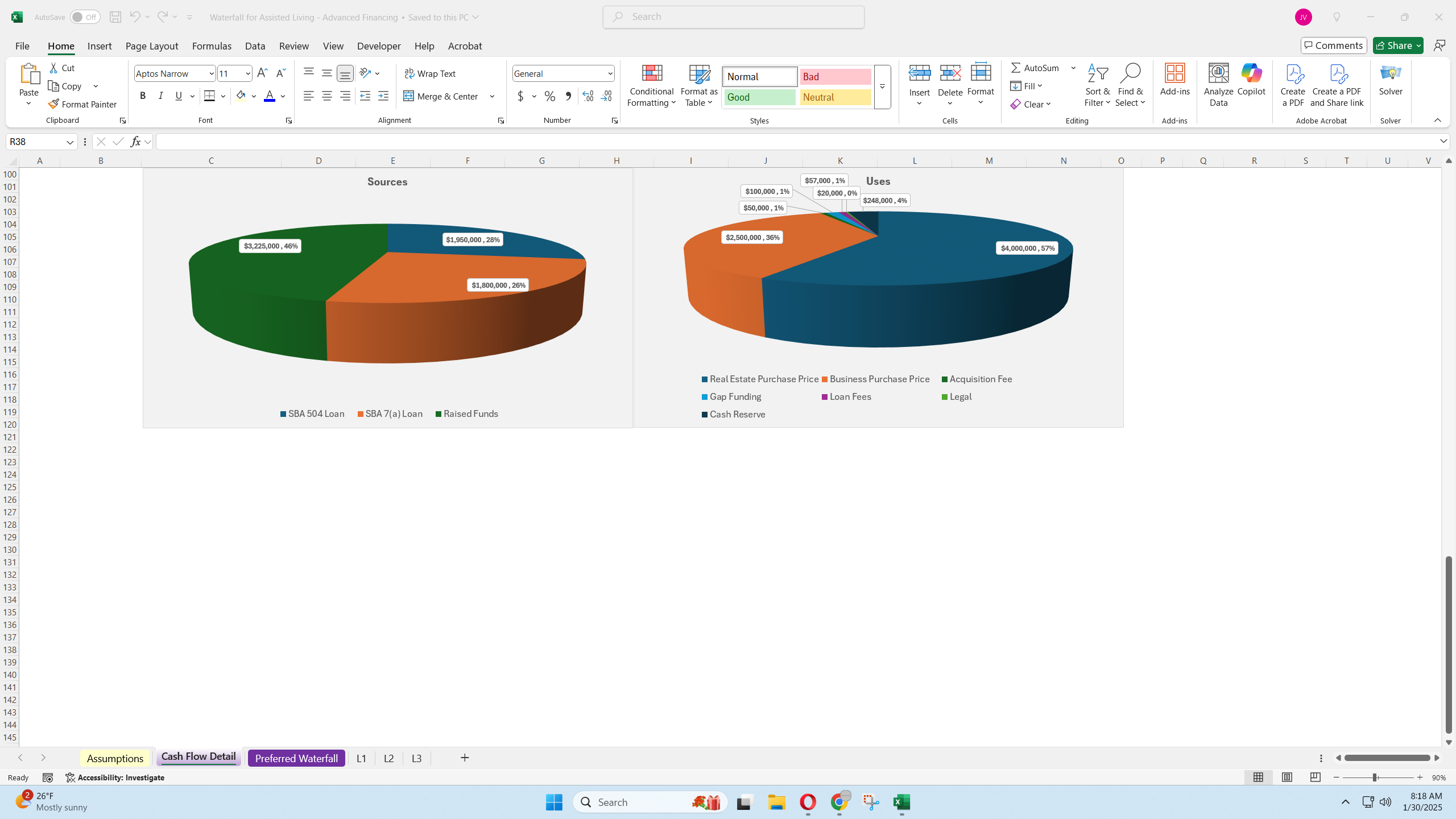

- Dashboards & Summaries

- Often the model presents a one-page summary with key metrics, a sources and uses table, five- or ten-year pro forma, and distribution waterfall outcomes.

Download over 200 of my templates in the all models bundle.

This Best Practice includes

1 Excel model and 1 Tutorial Video

Further information

Create cash flow and return forecasts for acquisition deals in real estate / senior care facilities.

Anything business acquisition with an underlying real estate asset.