Originally published: 29/03/2022 08:42

Last version published: 28/11/2024 21:11

Publication number: ELQ-49370-3

View all versions & Certificate

Last version published: 28/11/2024 21:11

Publication number: ELQ-49370-3

View all versions & Certificate

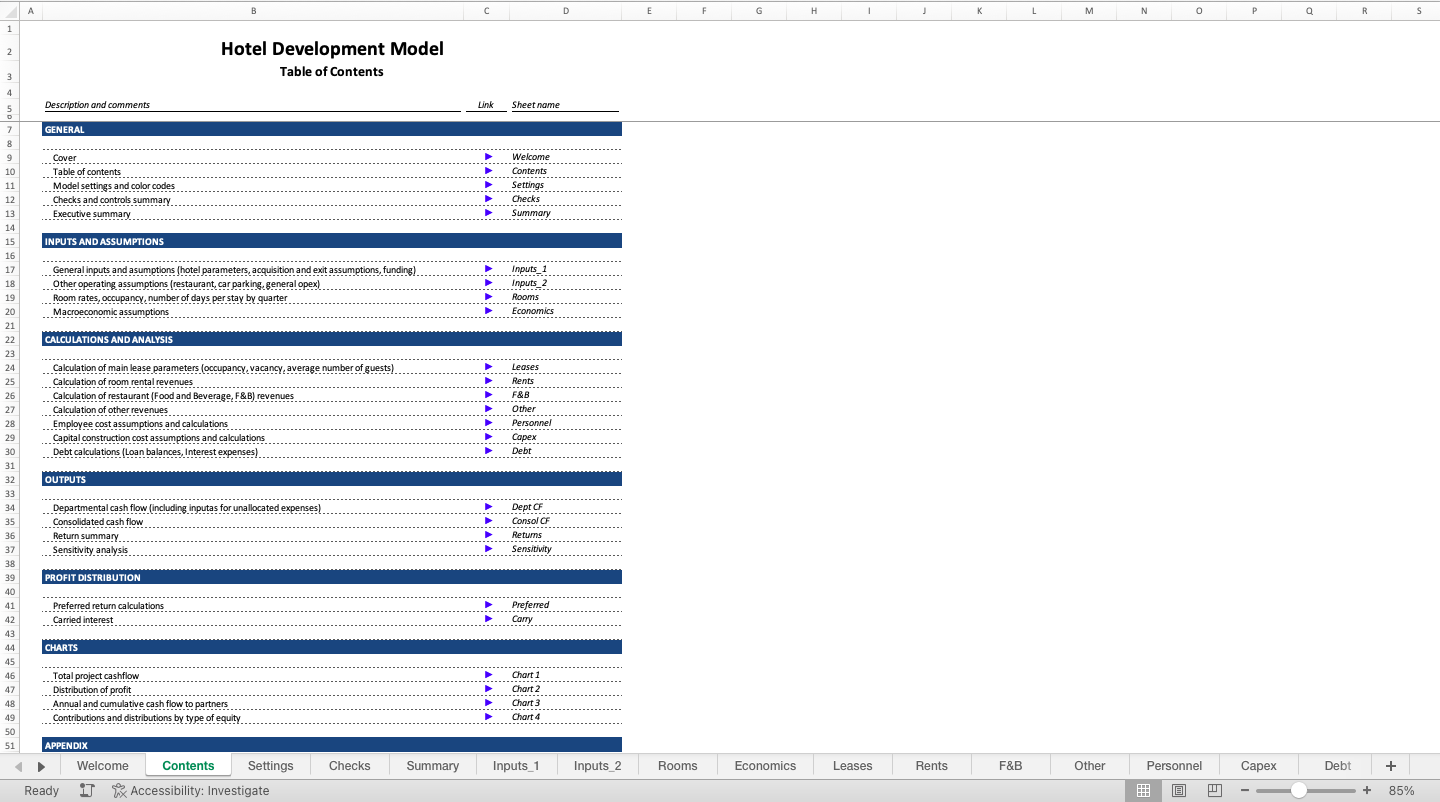

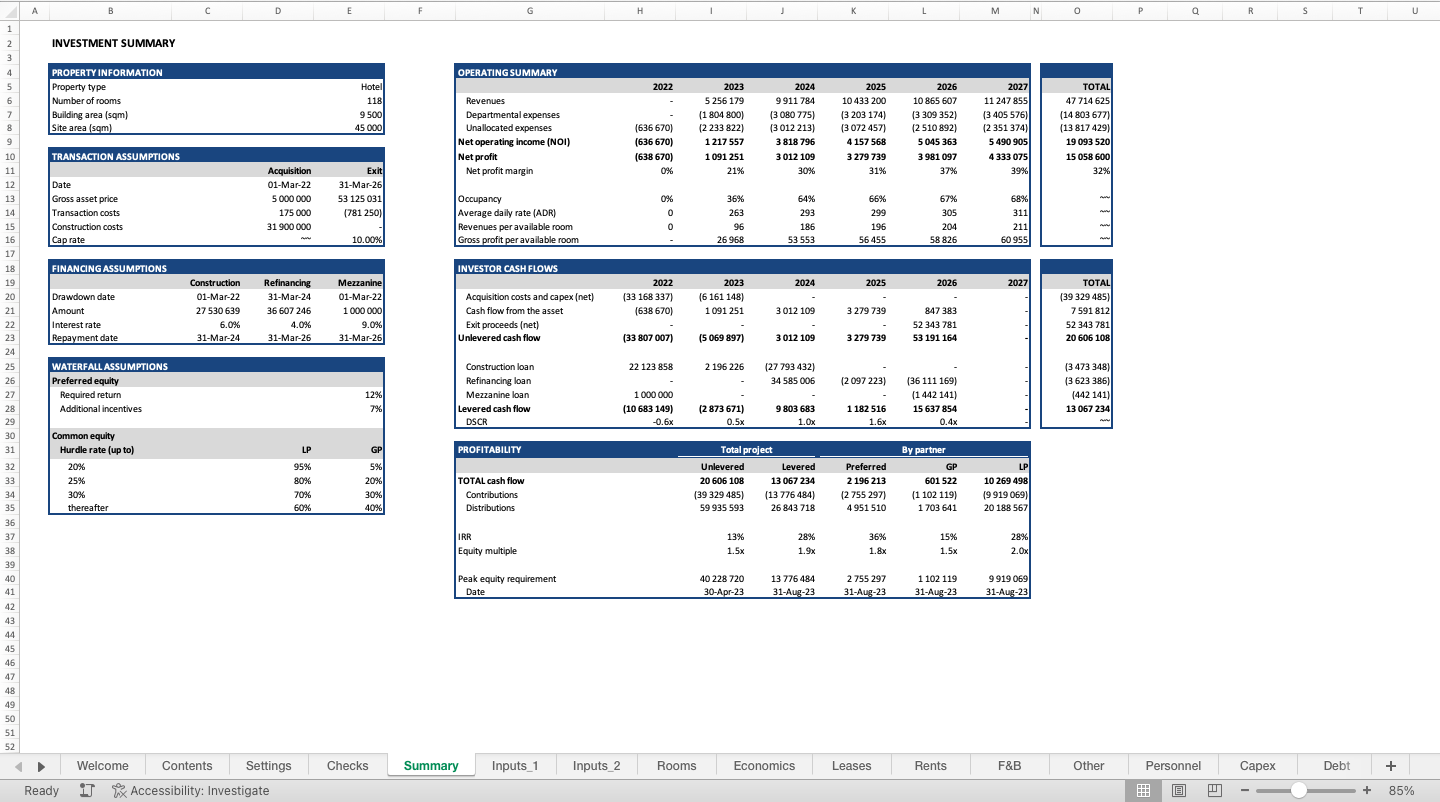

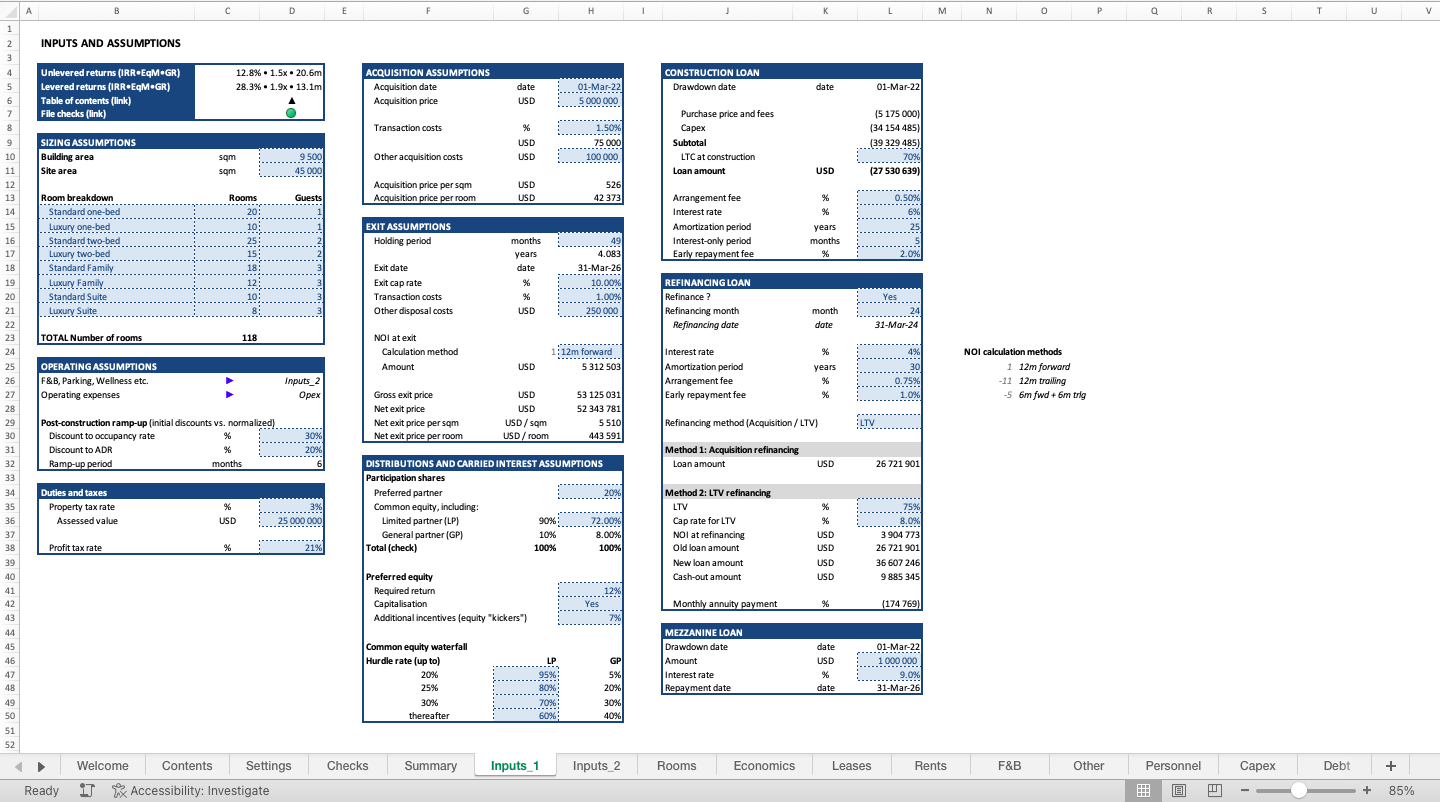

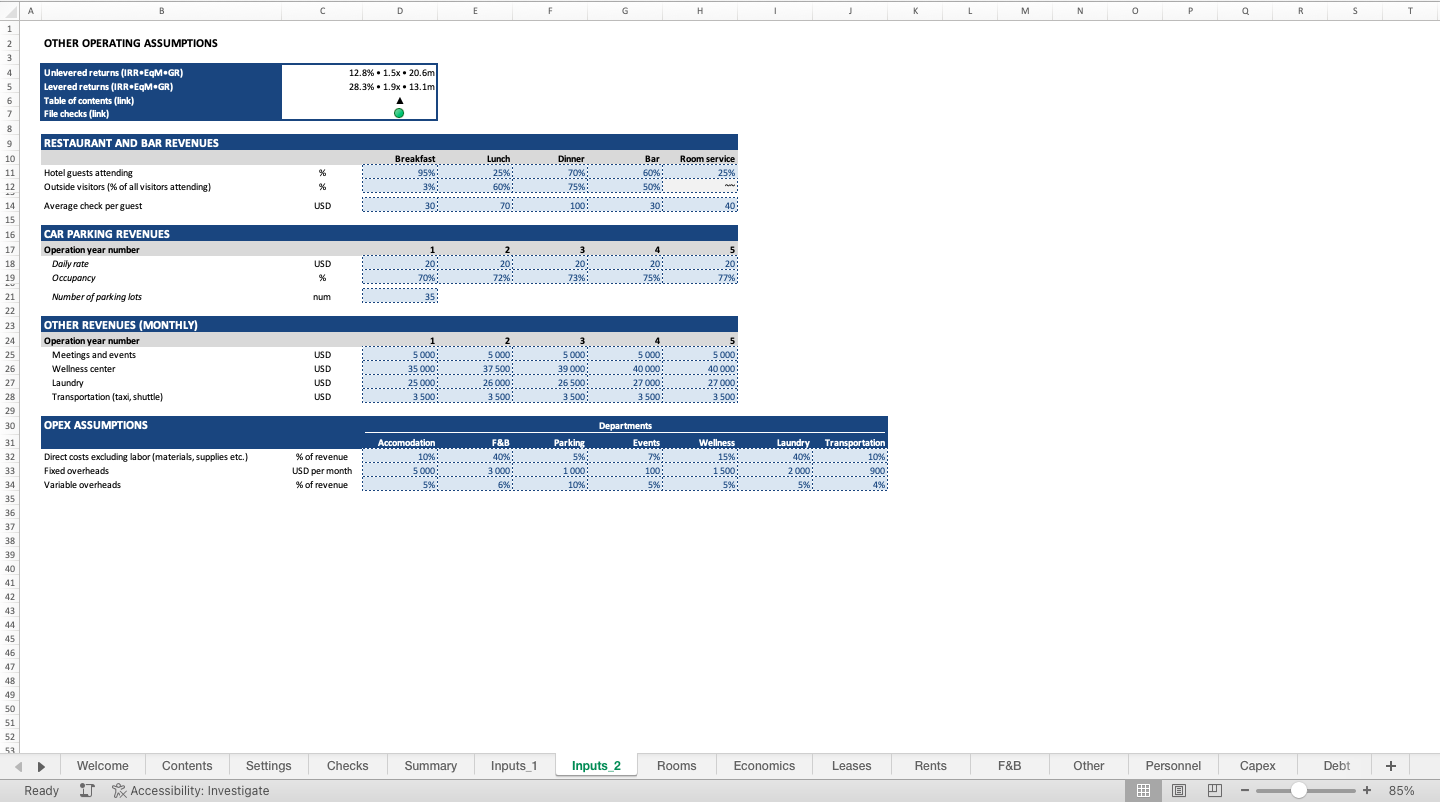

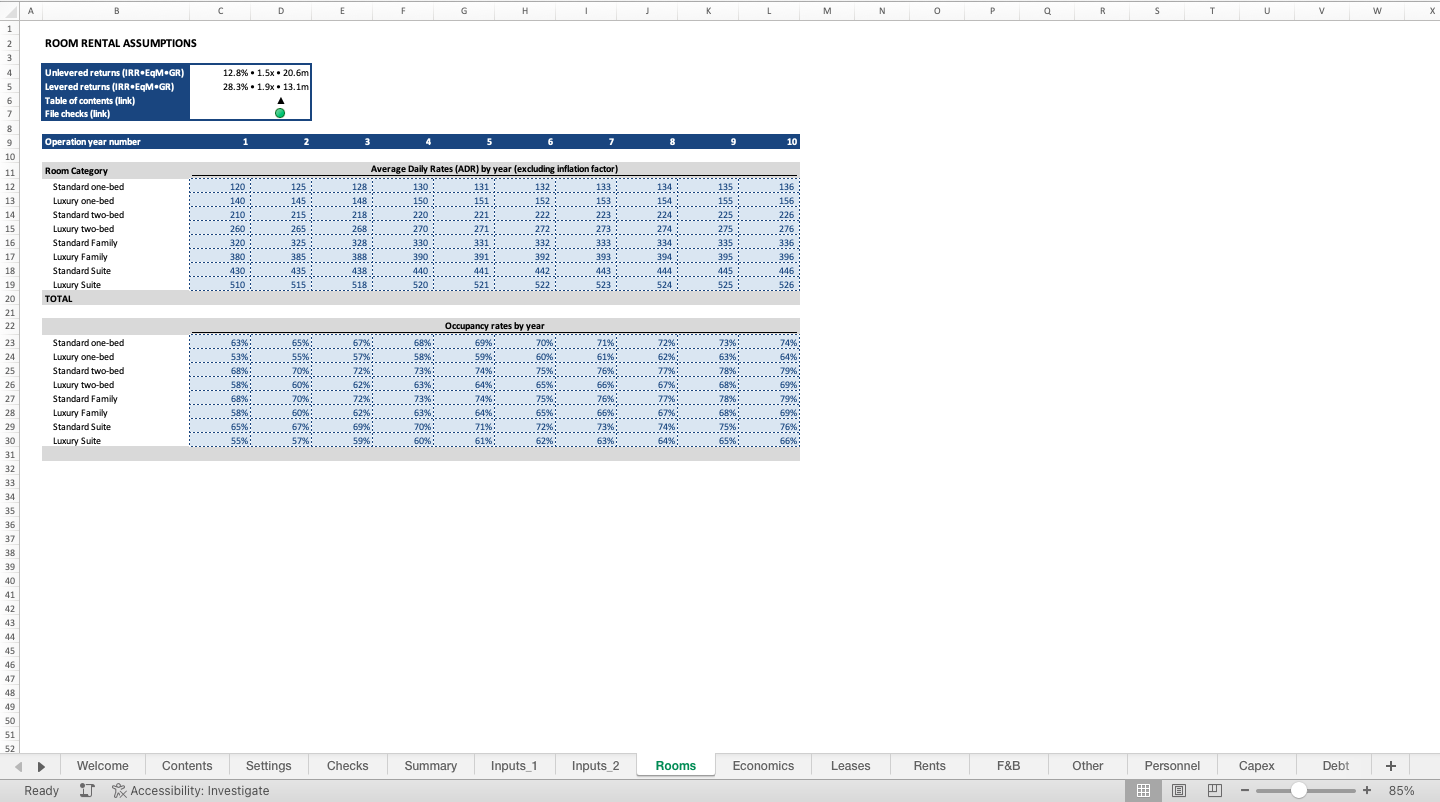

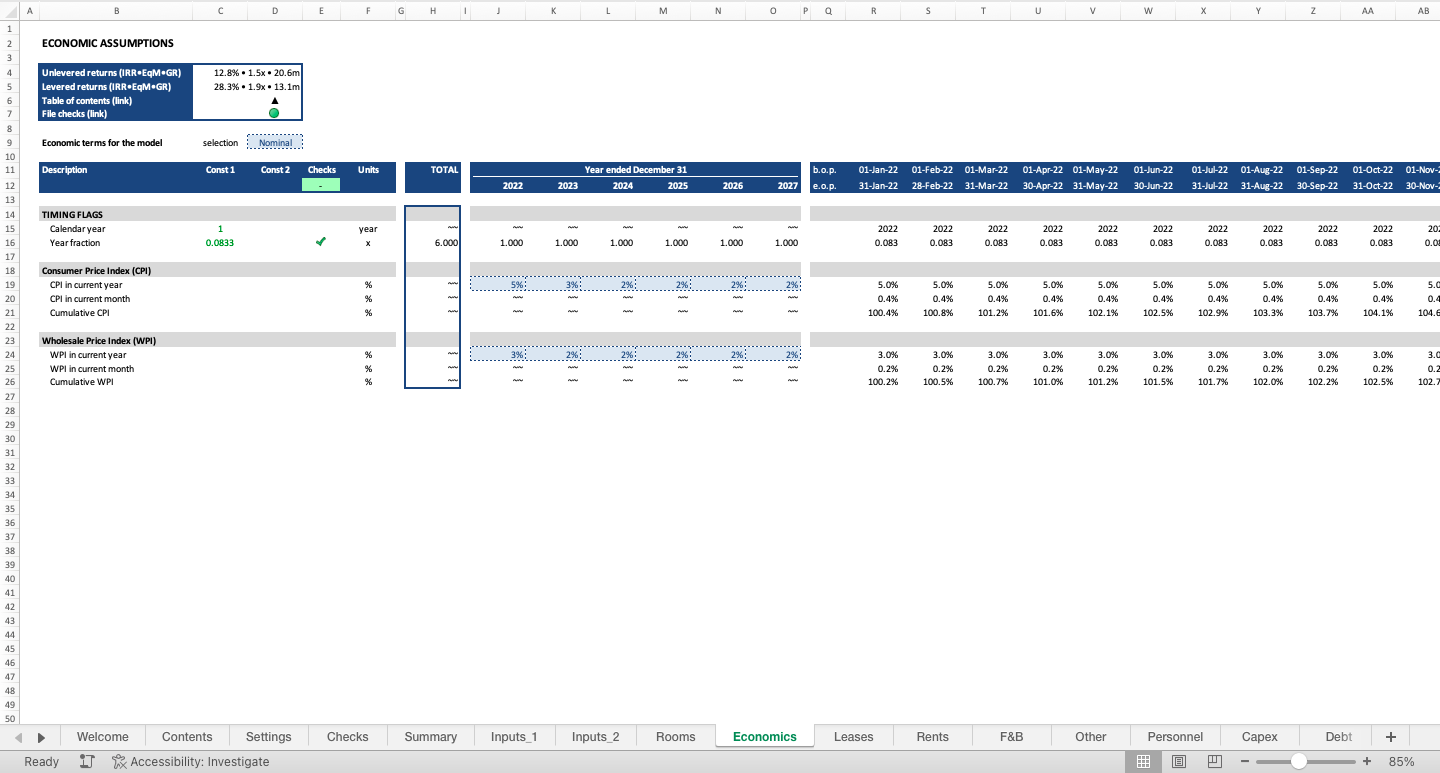

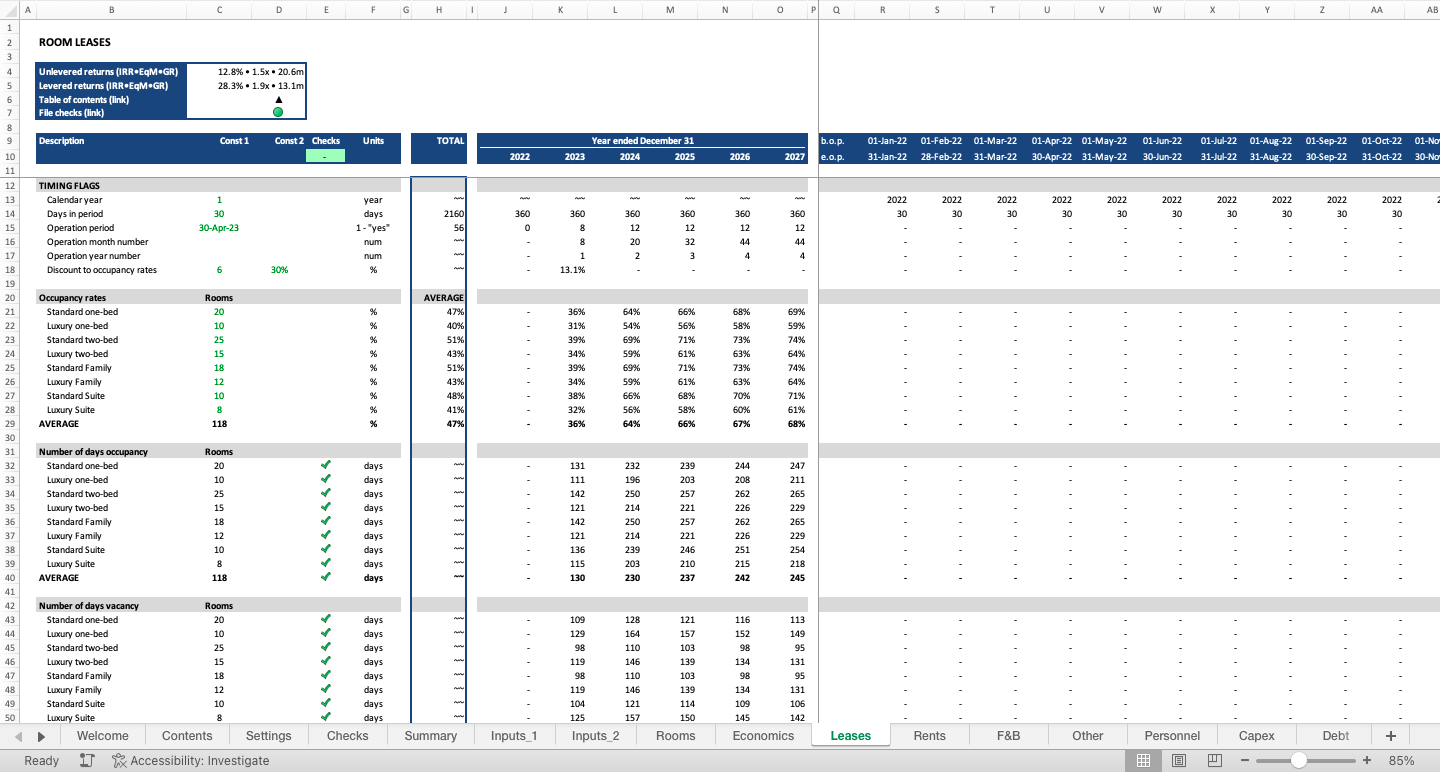

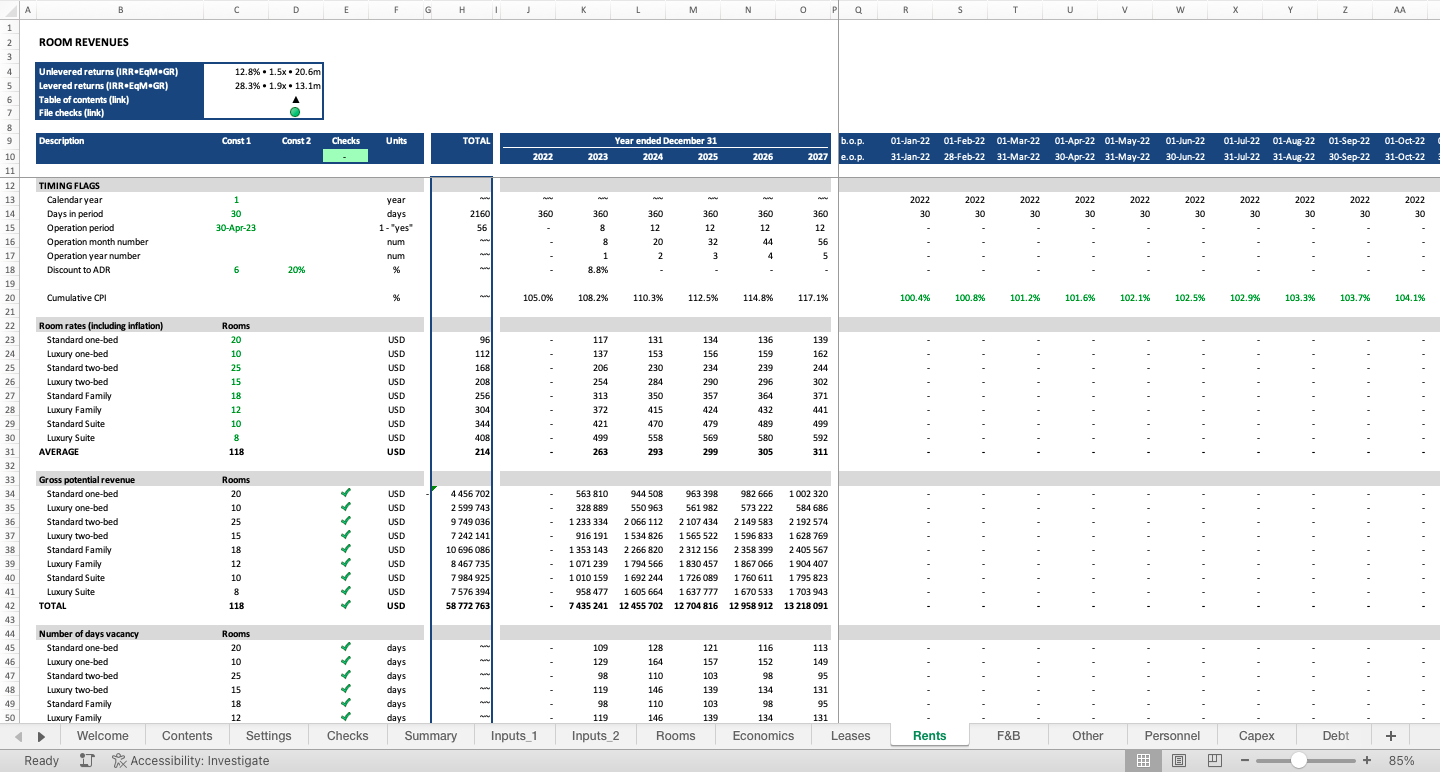

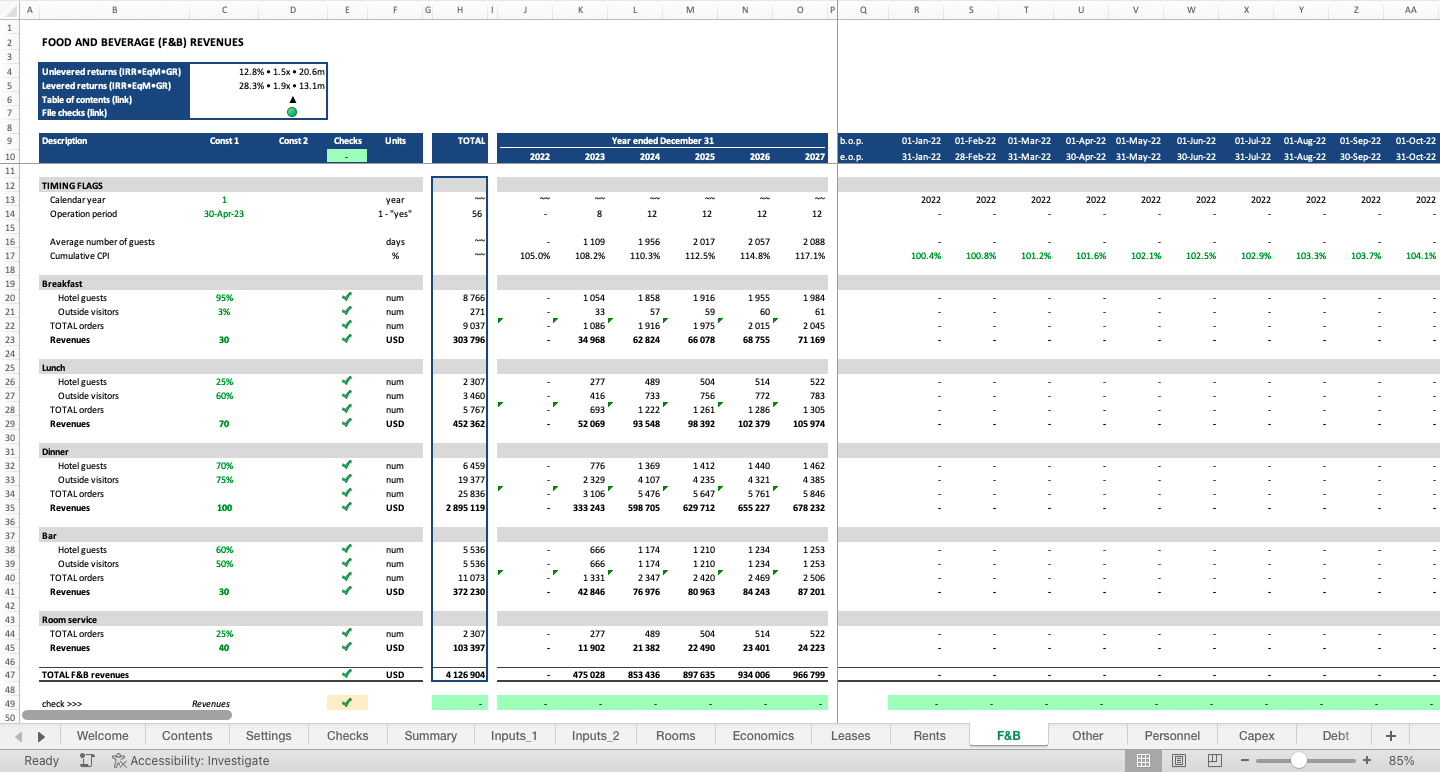

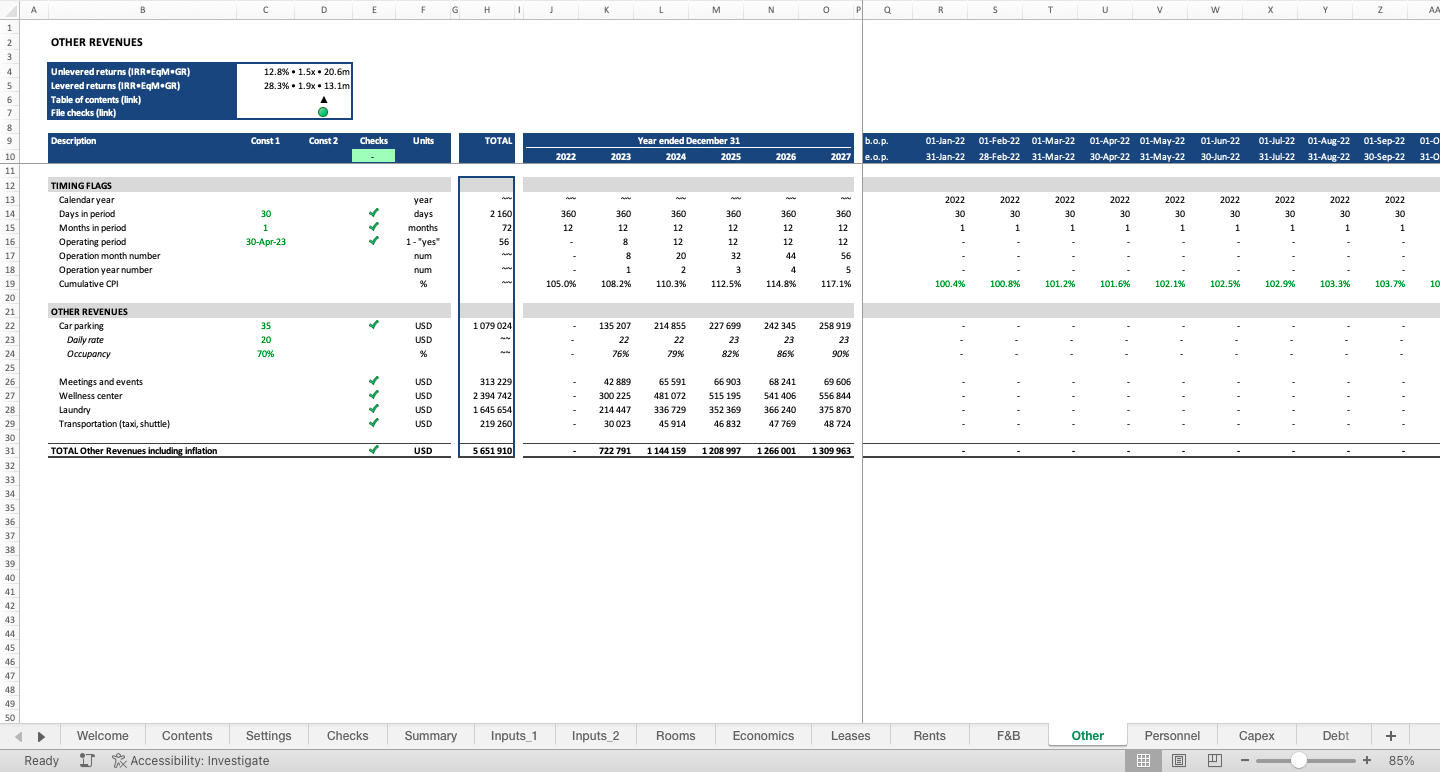

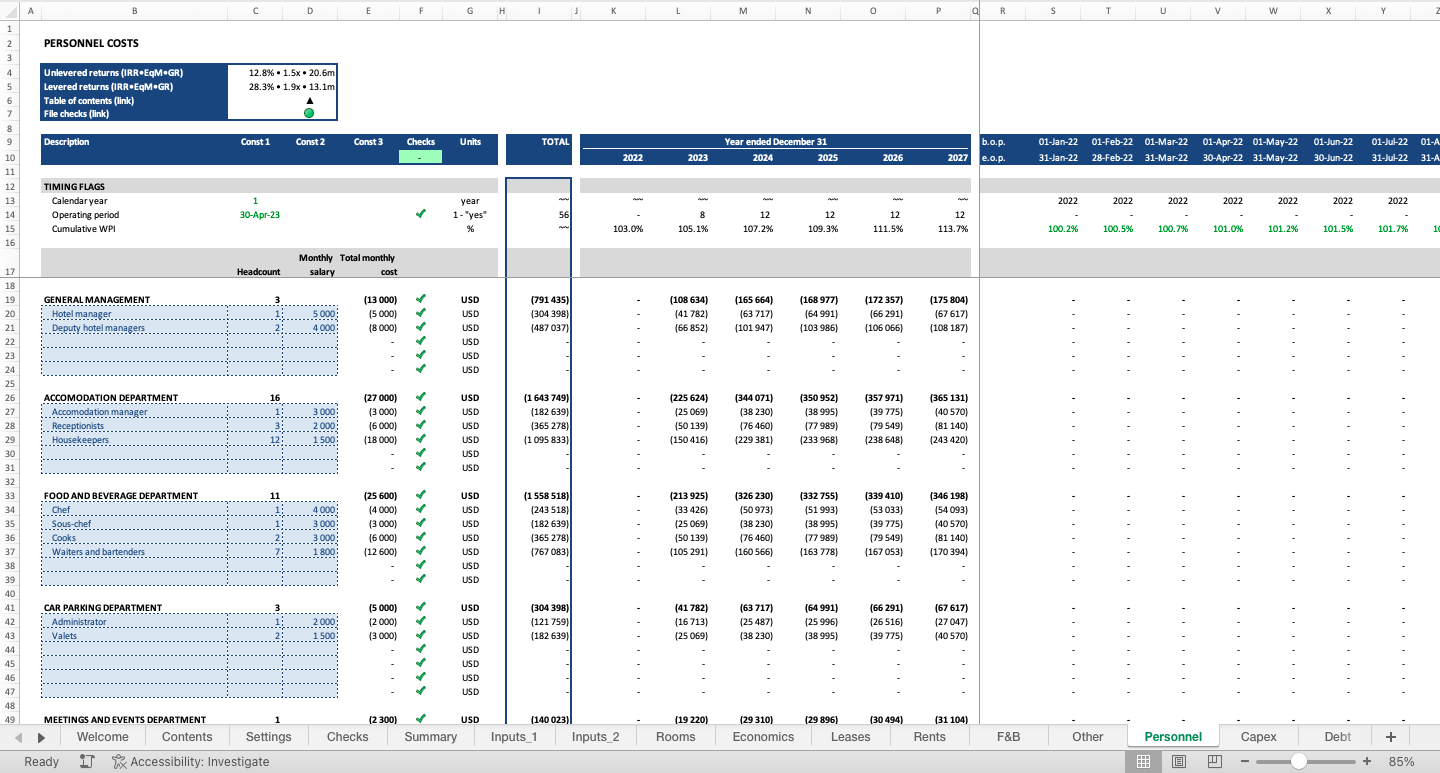

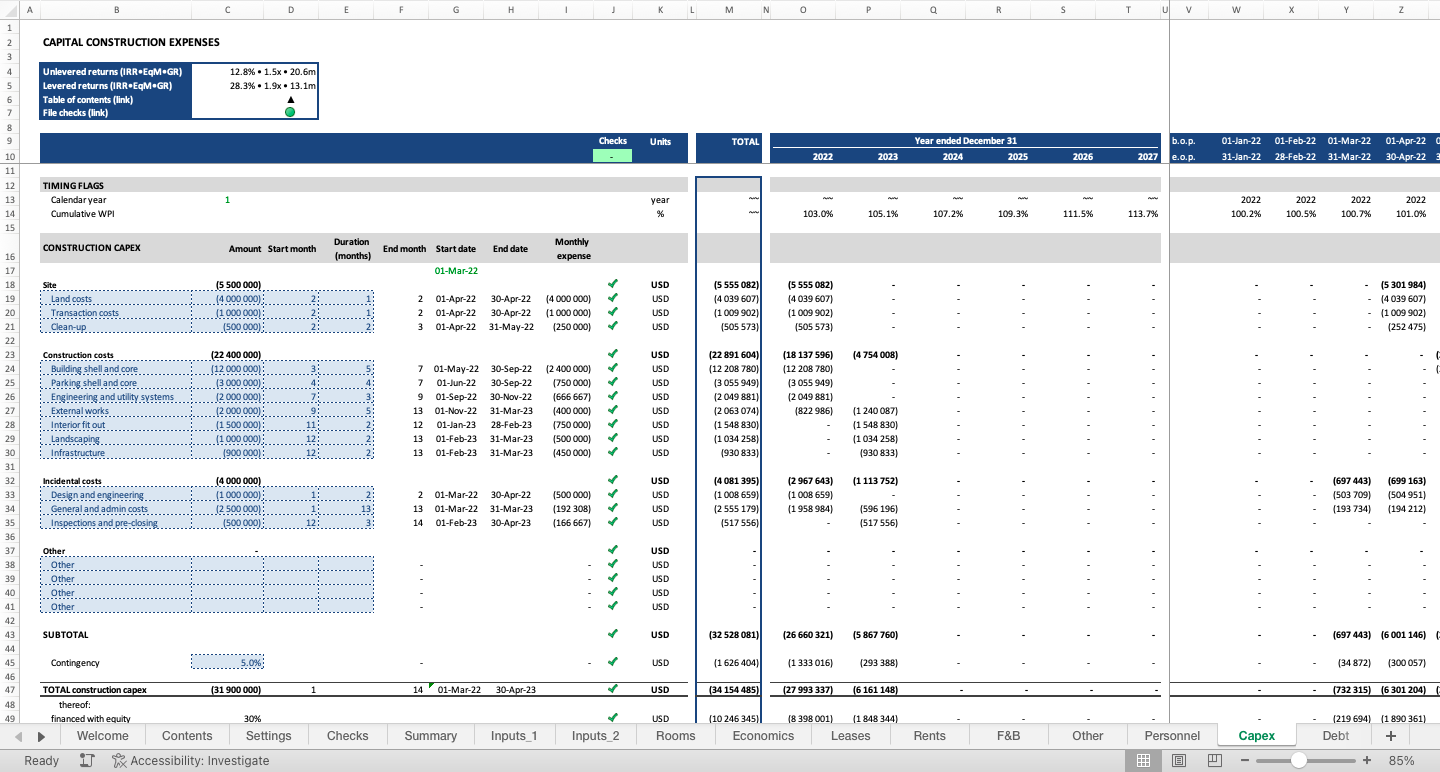

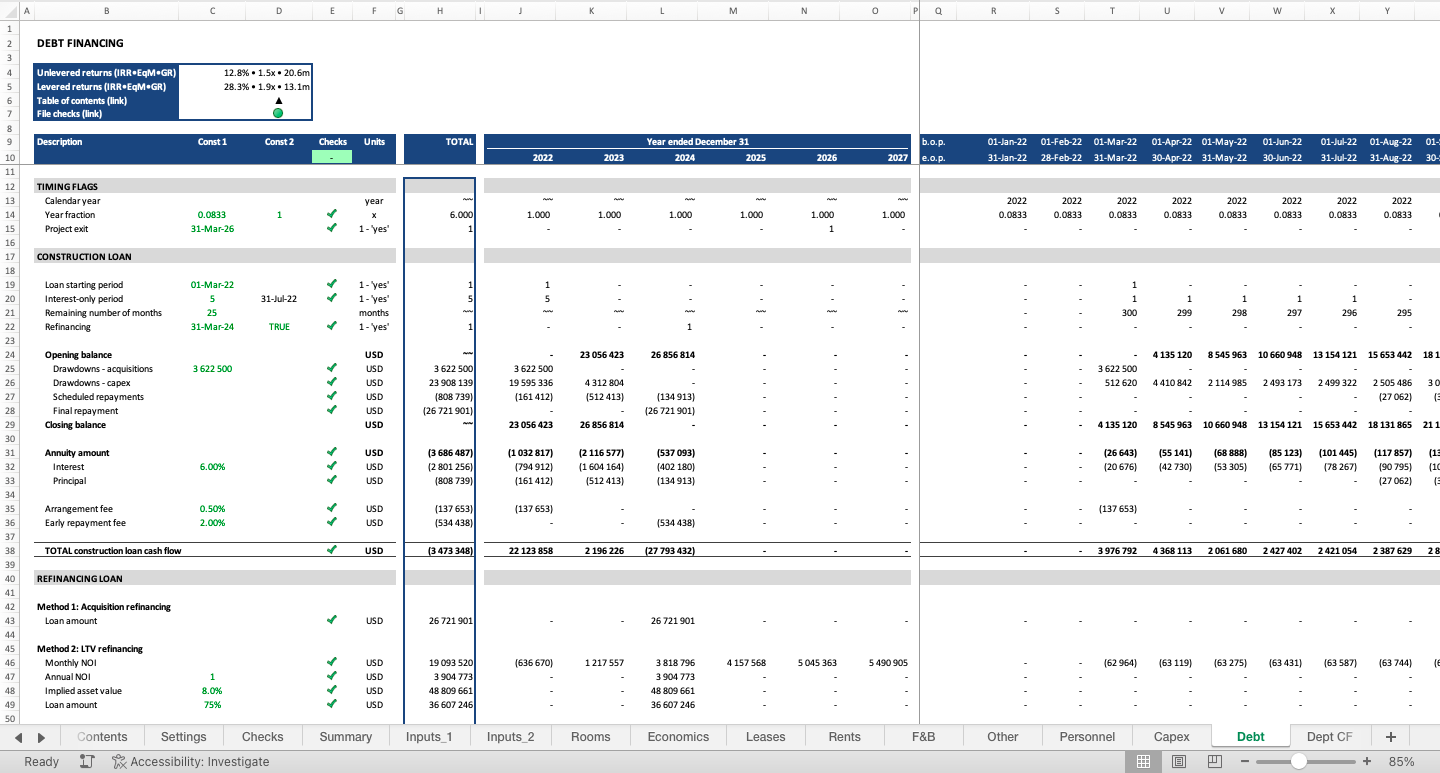

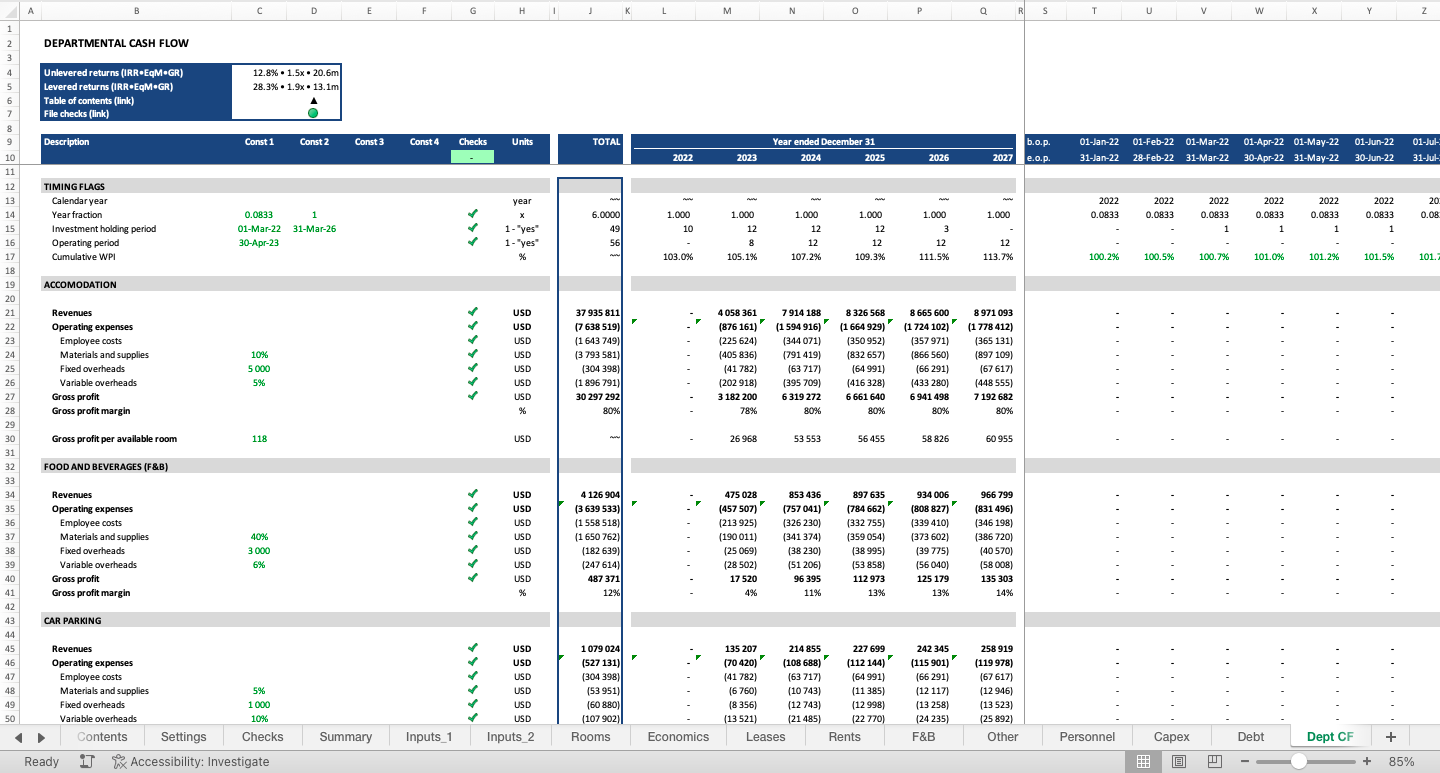

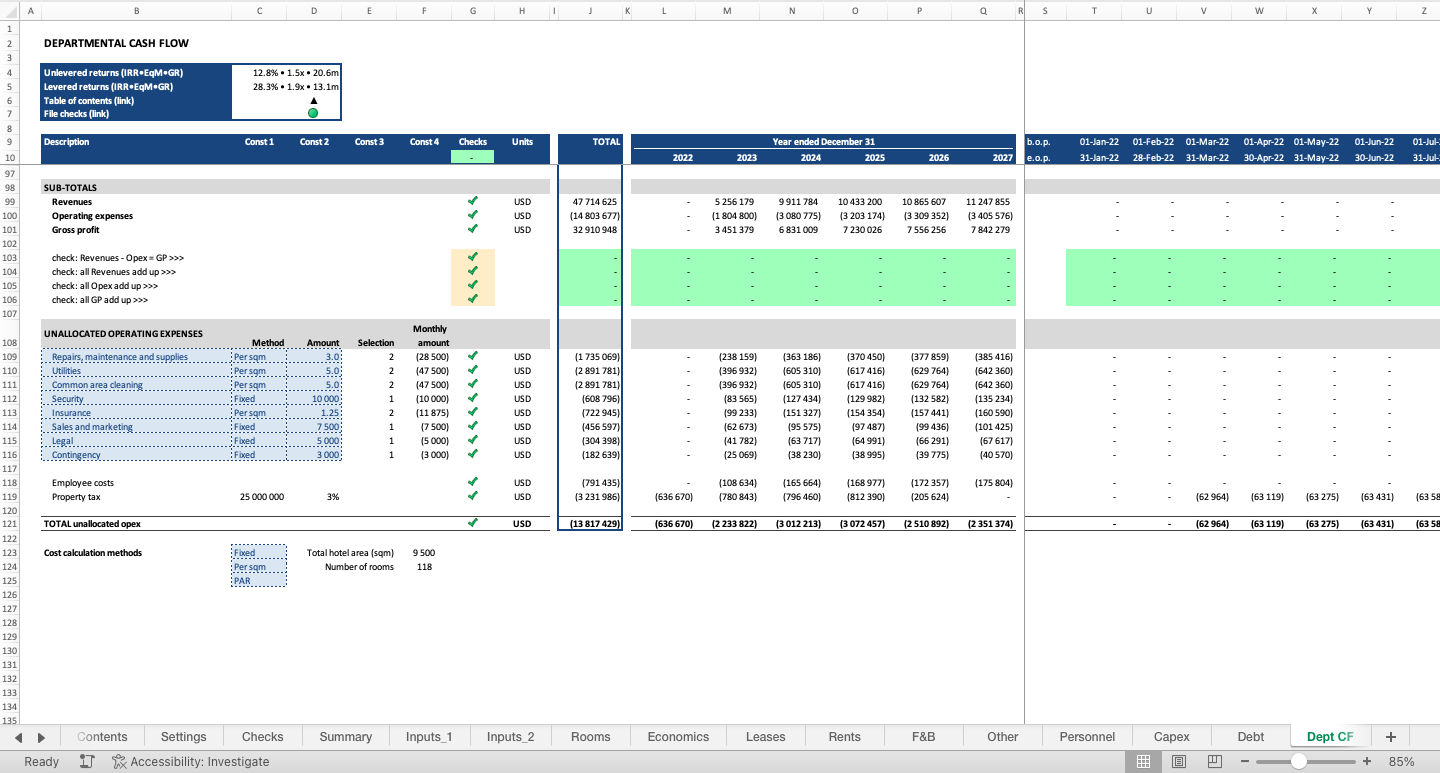

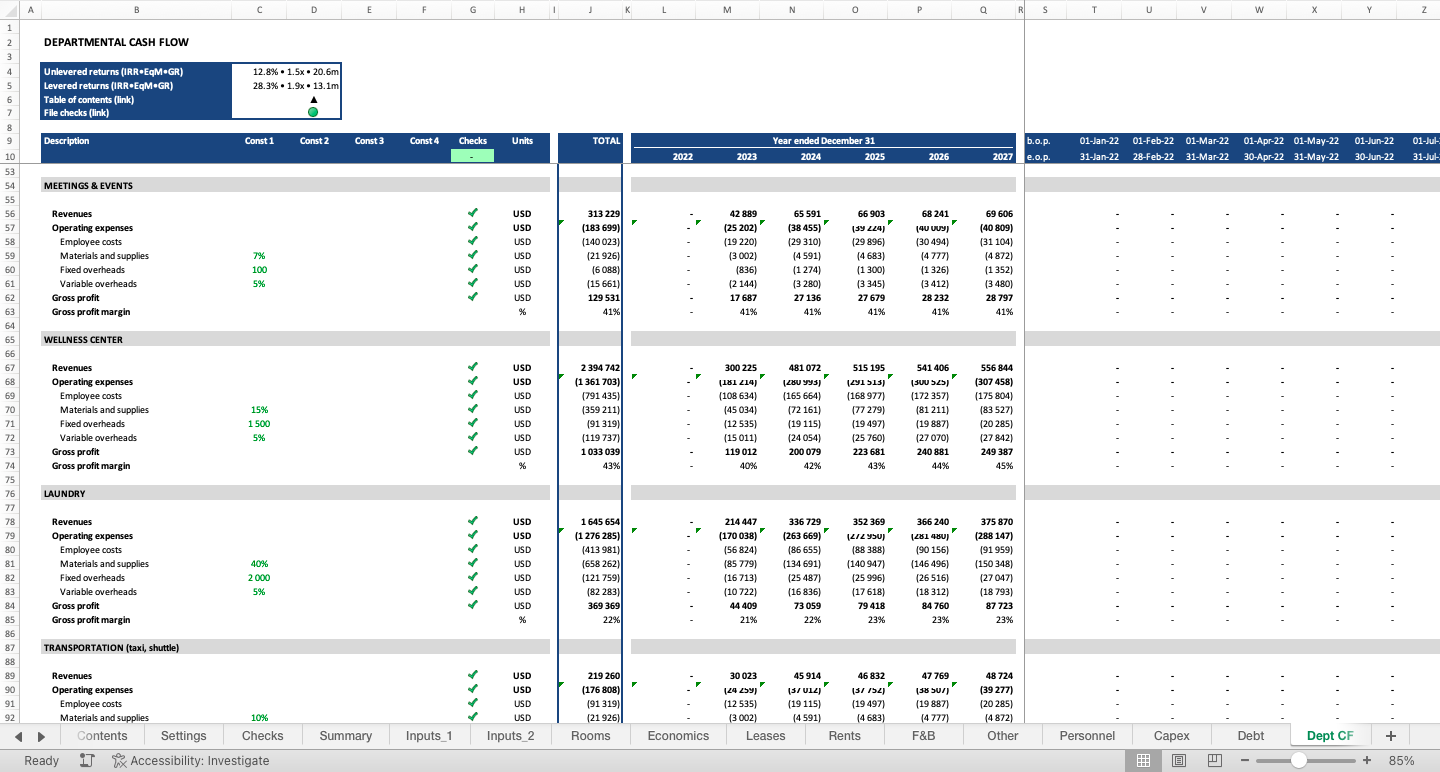

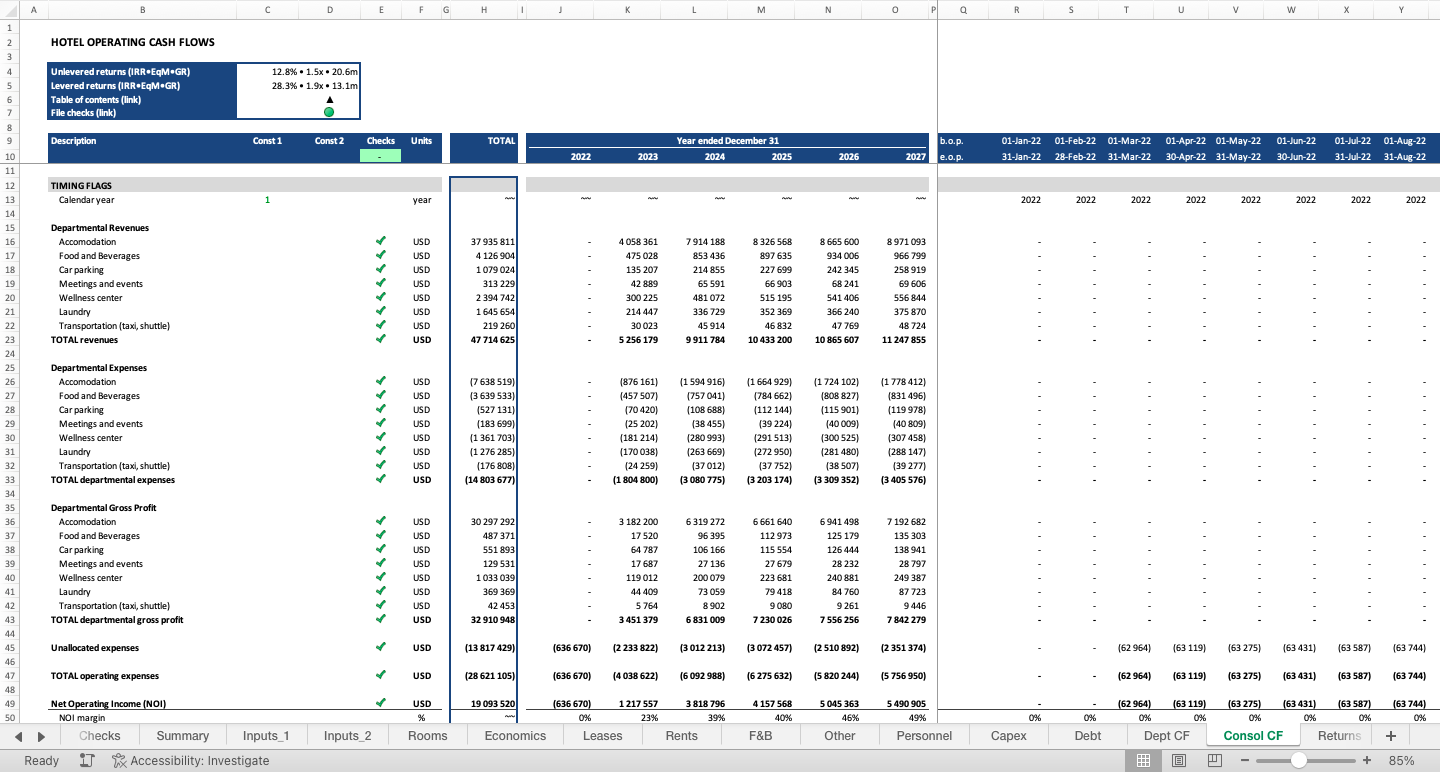

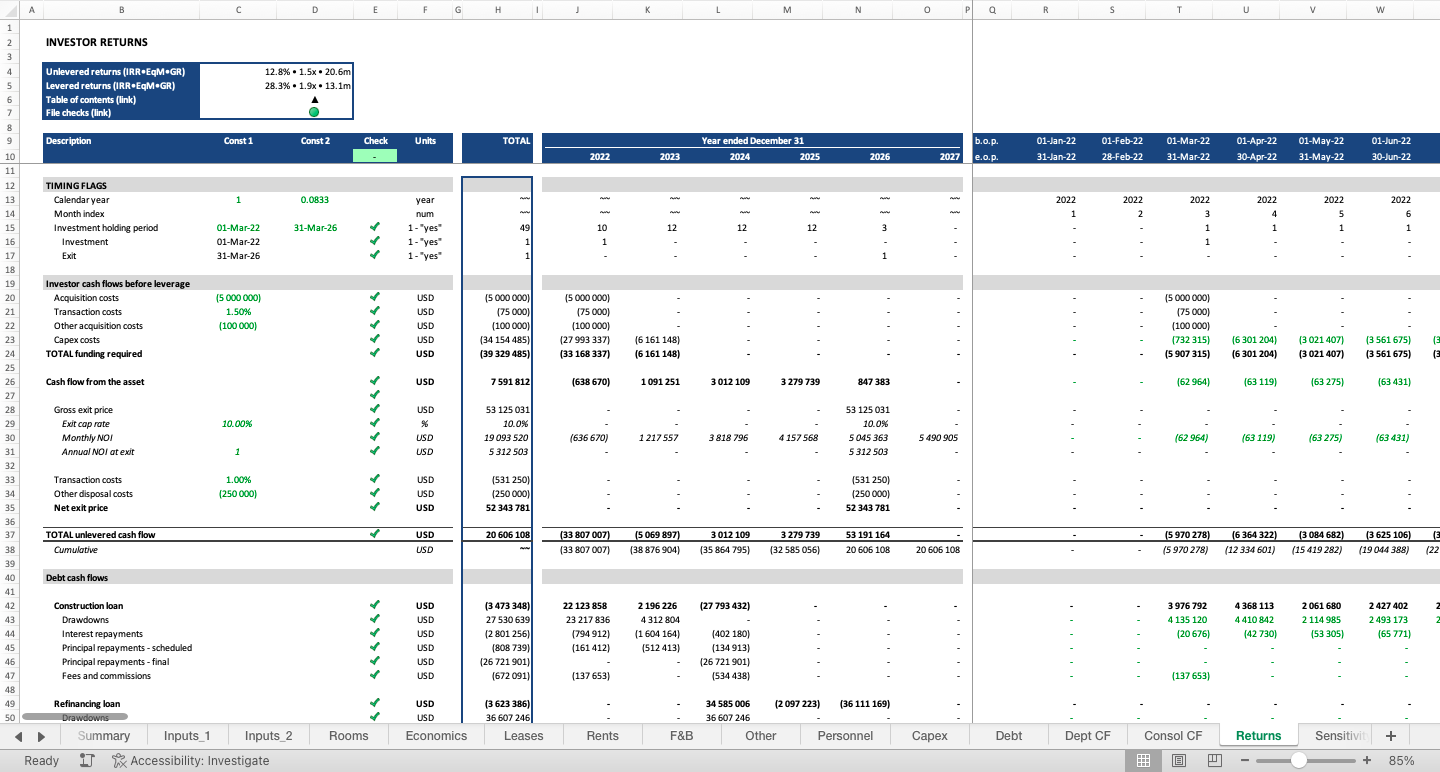

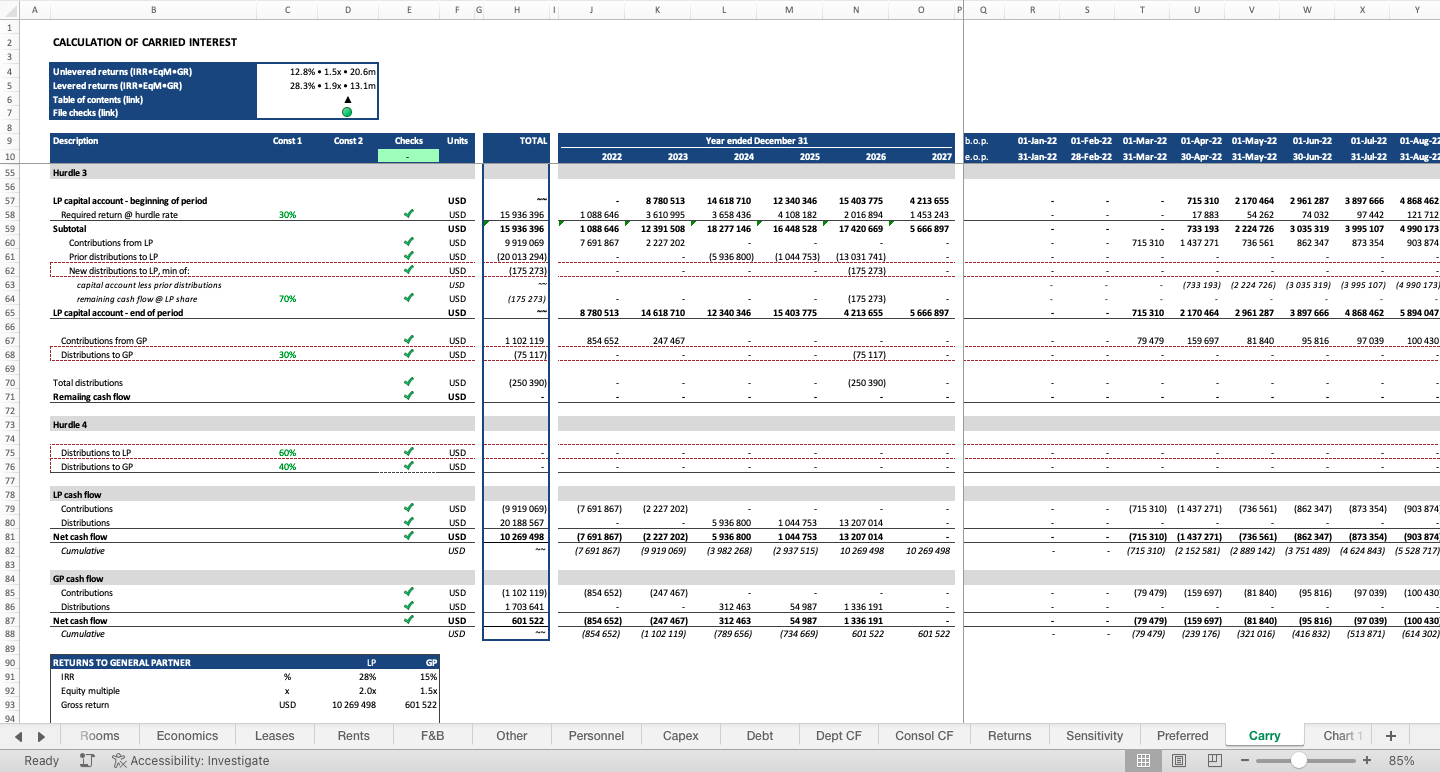

Hotel Development Financial Model

A professional model for hotel construction

Further information

Financial analysis for a hotel construction project

Use it if you are considering investing into a hotel development project

Every business case is unique and so the model might require fine-tuning. Contact me if you need help adjusting the model to your particular project or if you need a model developed completely from scratch.