Originally published: 25/06/2018 12:47

Last version published: 27/12/2023 09:25

Publication number: ELQ-77678-8

View all versions & Certificate

Last version published: 27/12/2023 09:25

Publication number: ELQ-77678-8

View all versions & Certificate

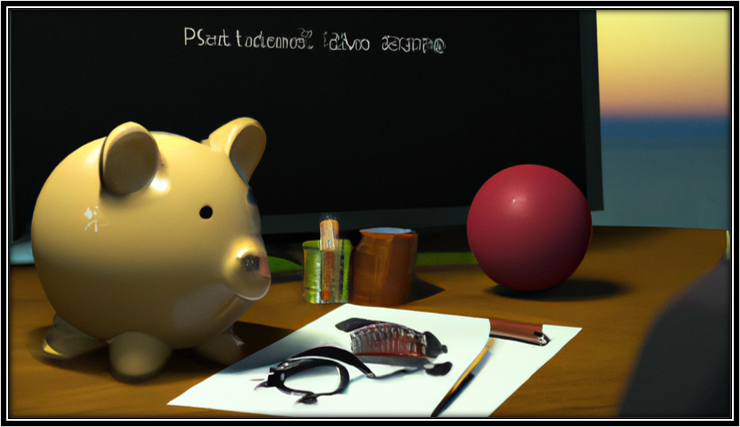

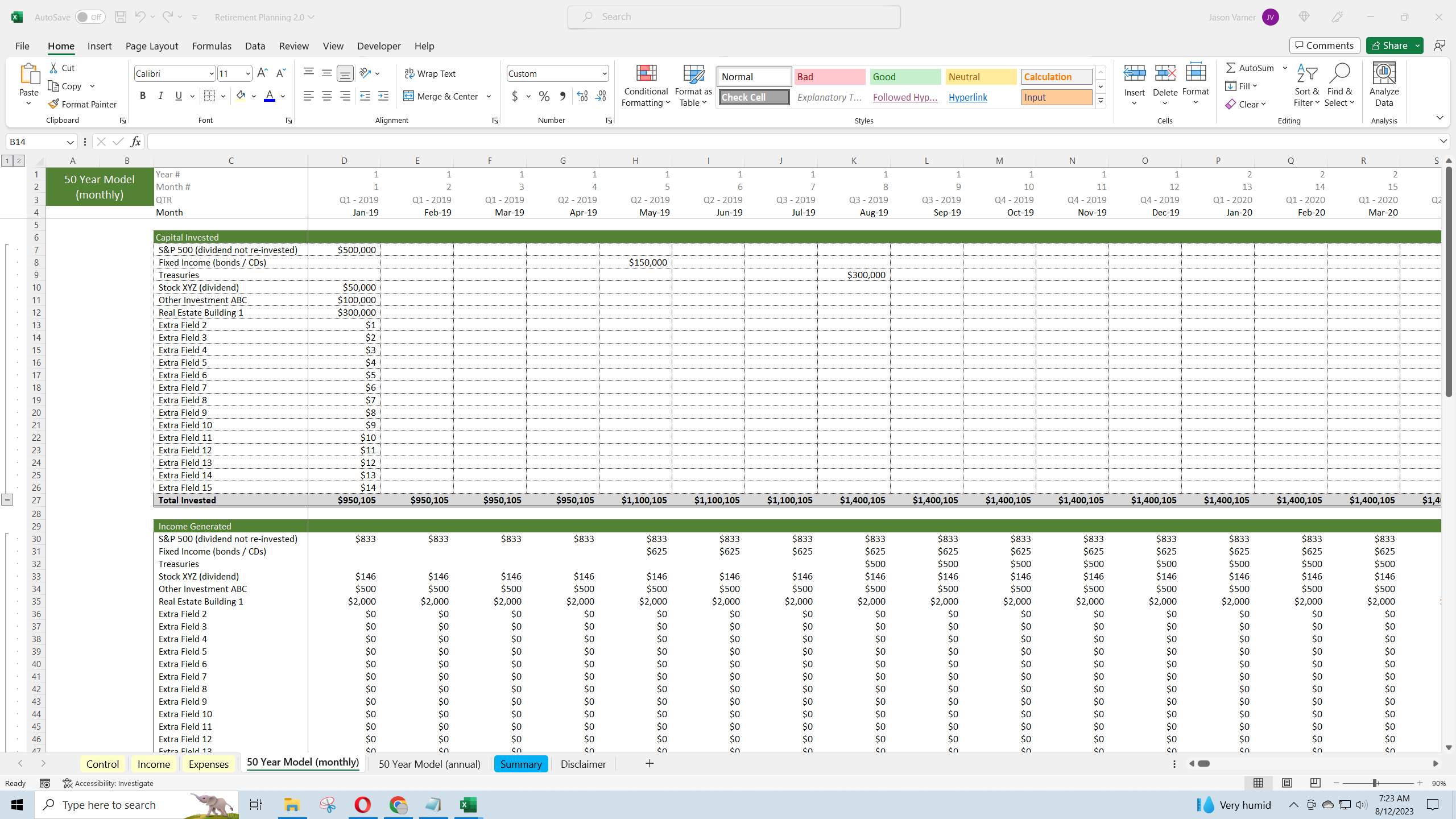

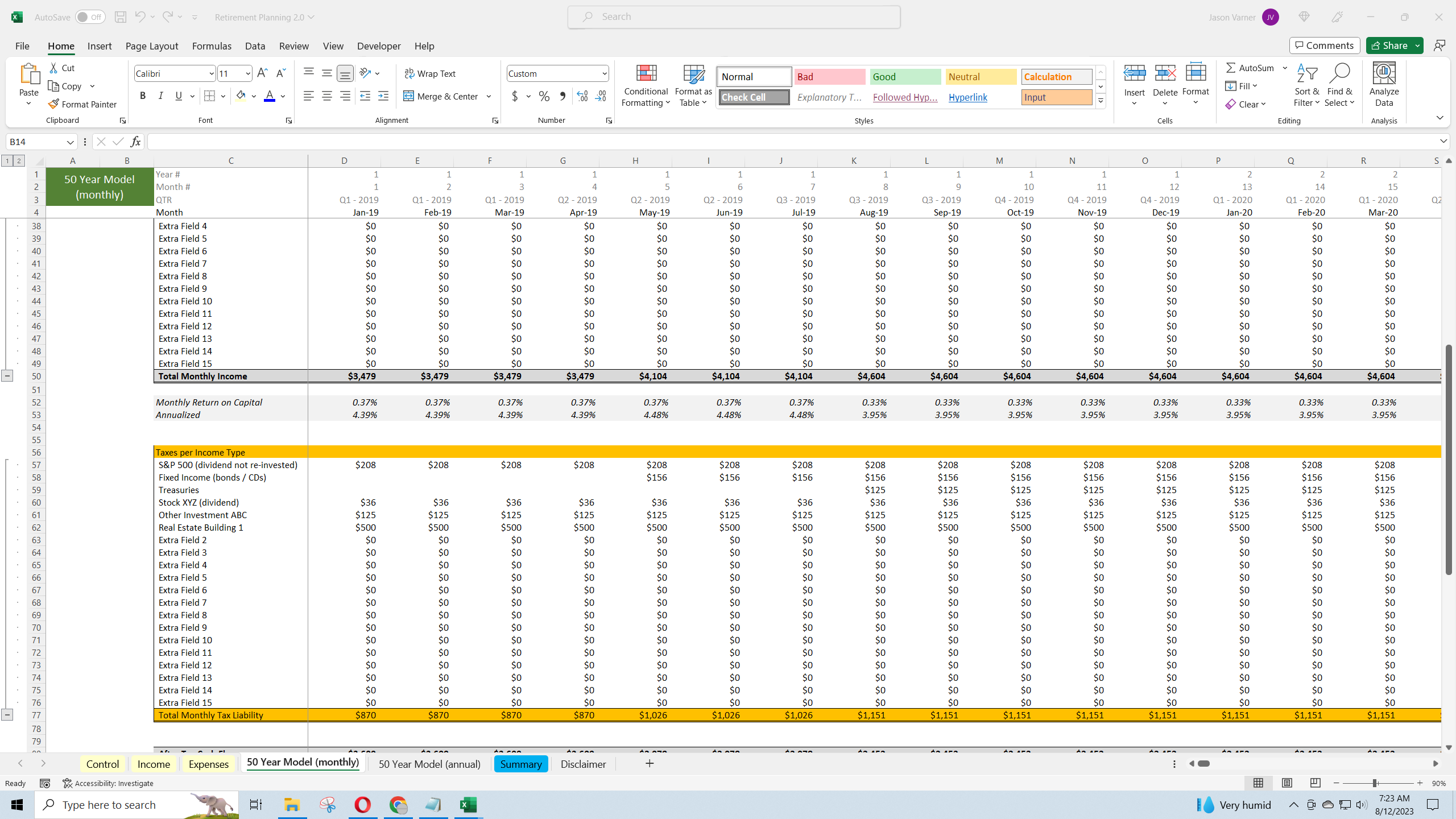

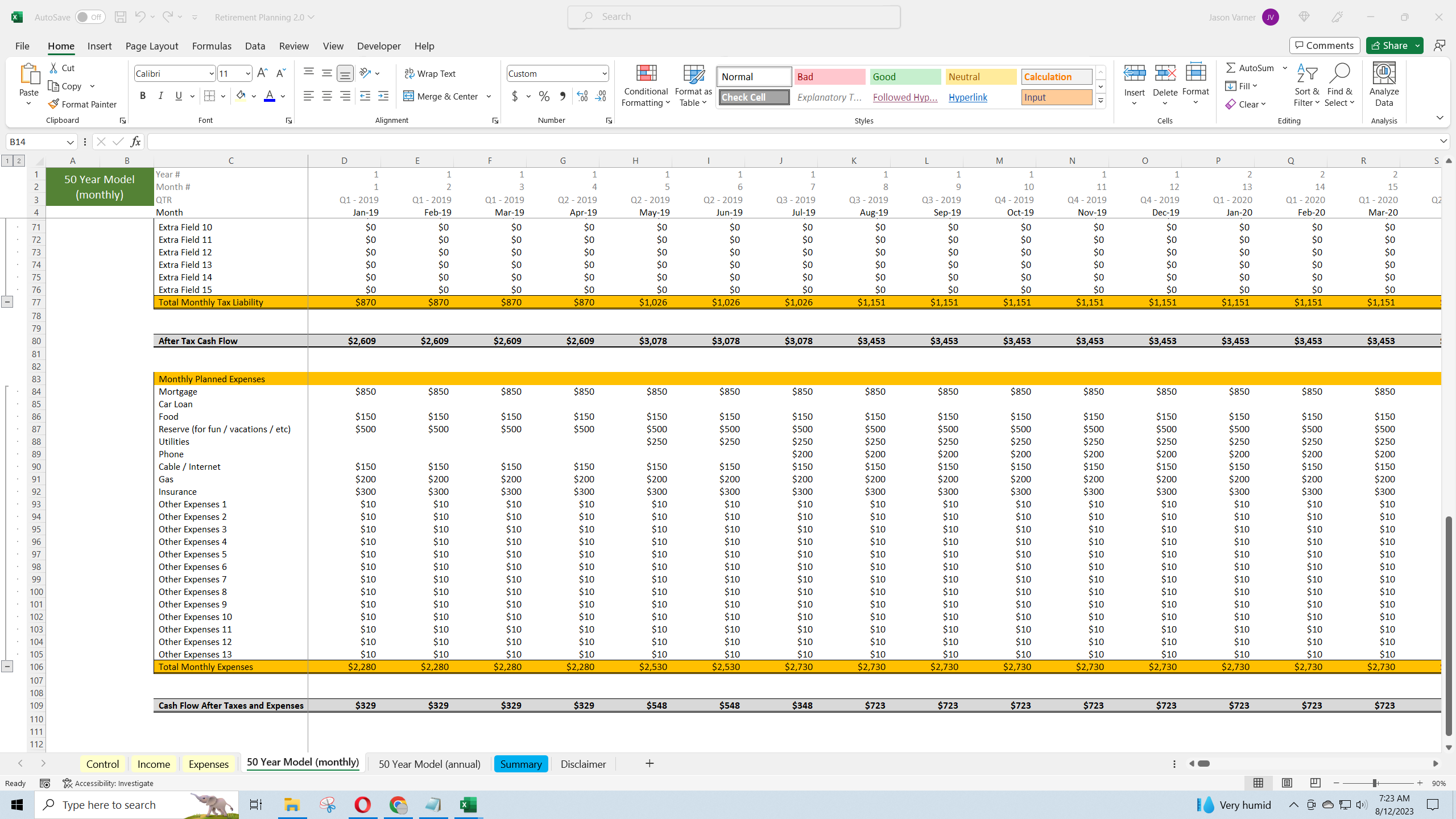

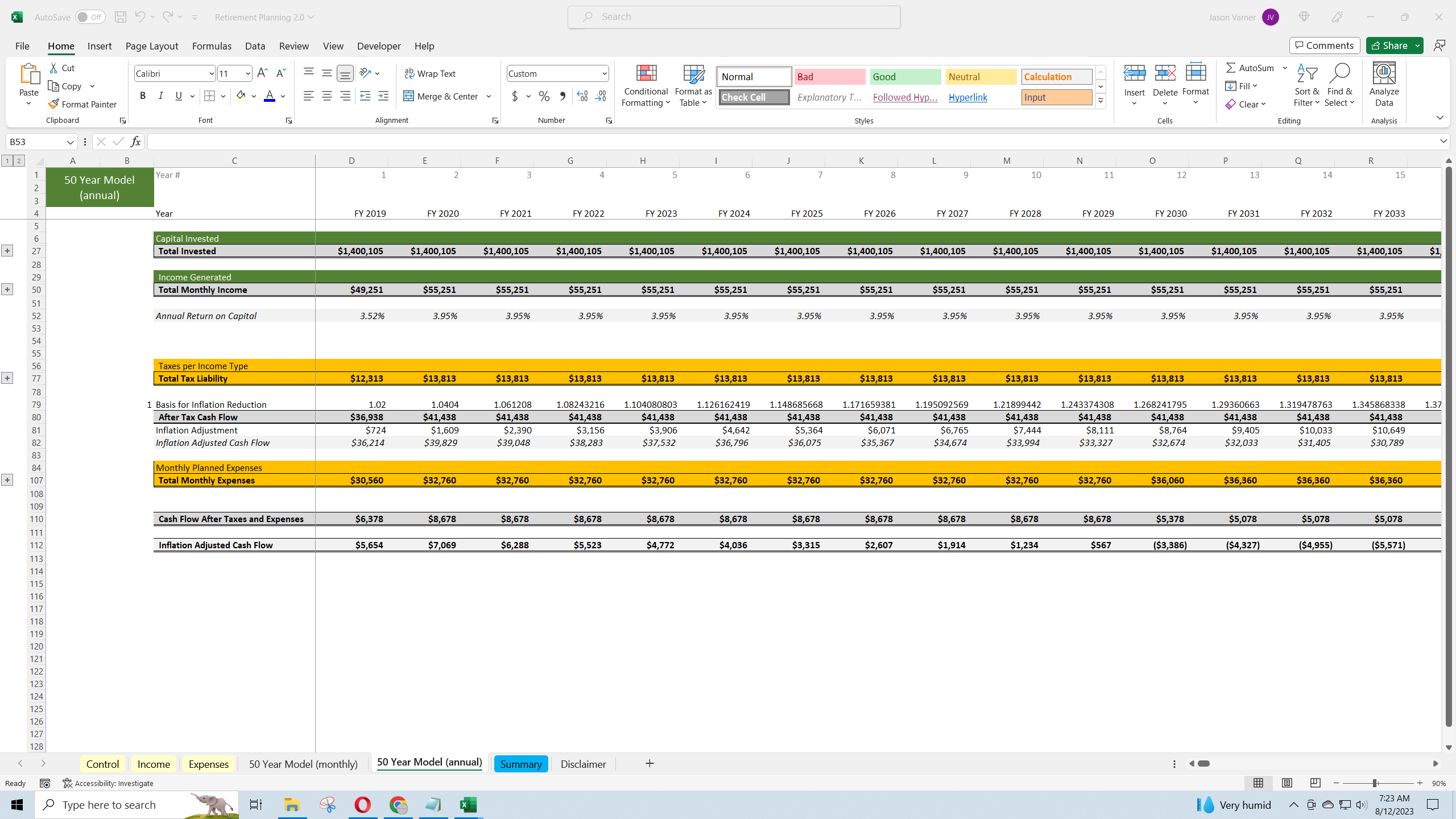

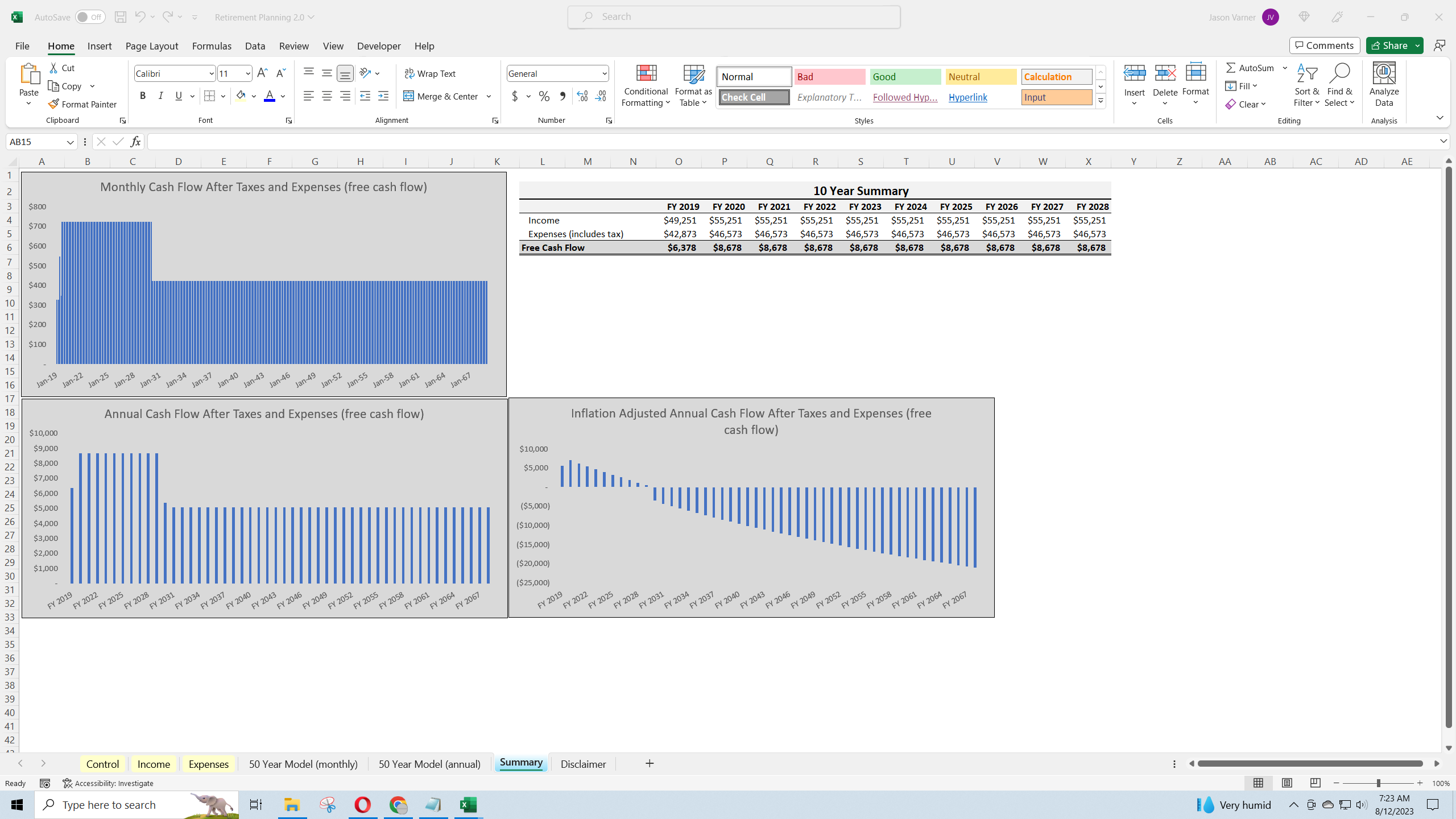

Retirement Planner Excel Model - Cash Flow Forecasting with Inflation Adjustment

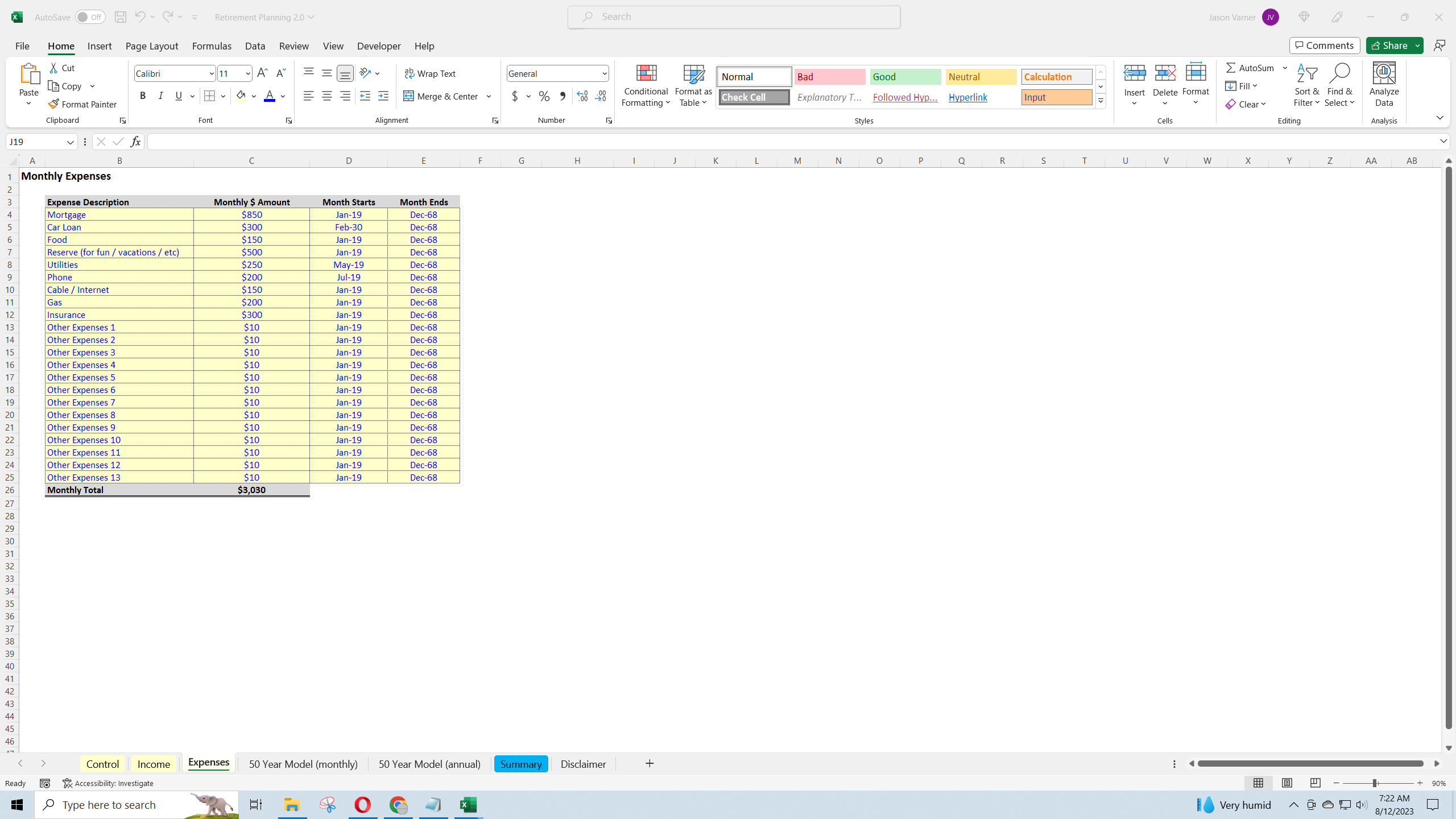

Create an income generating schedule as well as budget your expenses for retirement.

Further information

Plan out the future cash flows of your retirement.

When using only income generating assets.

When not using income generating assets and not planning for retirement.