Originally published: 21/03/2024 12:41

Last version published: 29/03/2024 09:05

Publication number: ELQ-73504-2

View all versions & Certificate

Last version published: 29/03/2024 09:05

Publication number: ELQ-73504-2

View all versions & Certificate

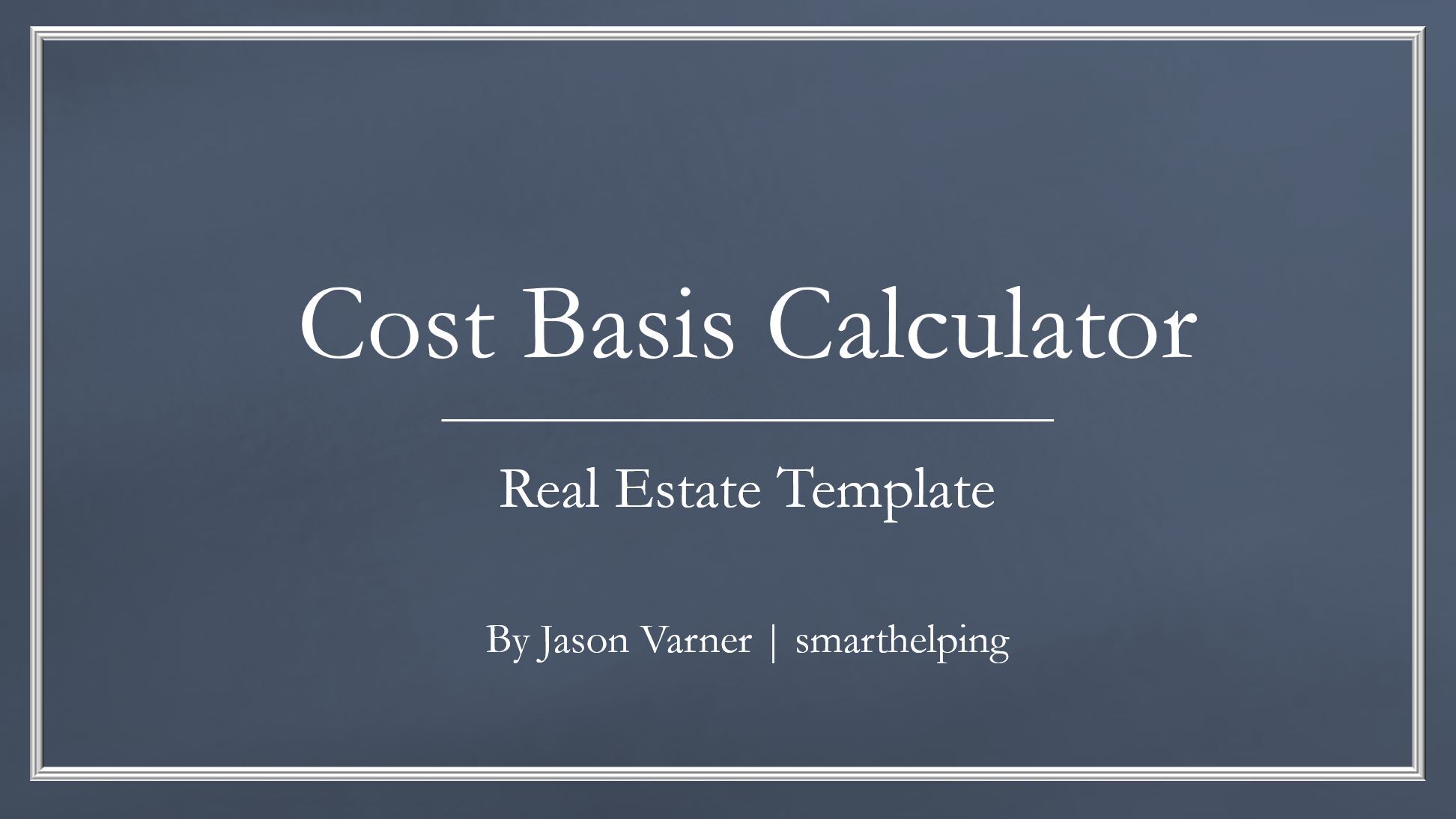

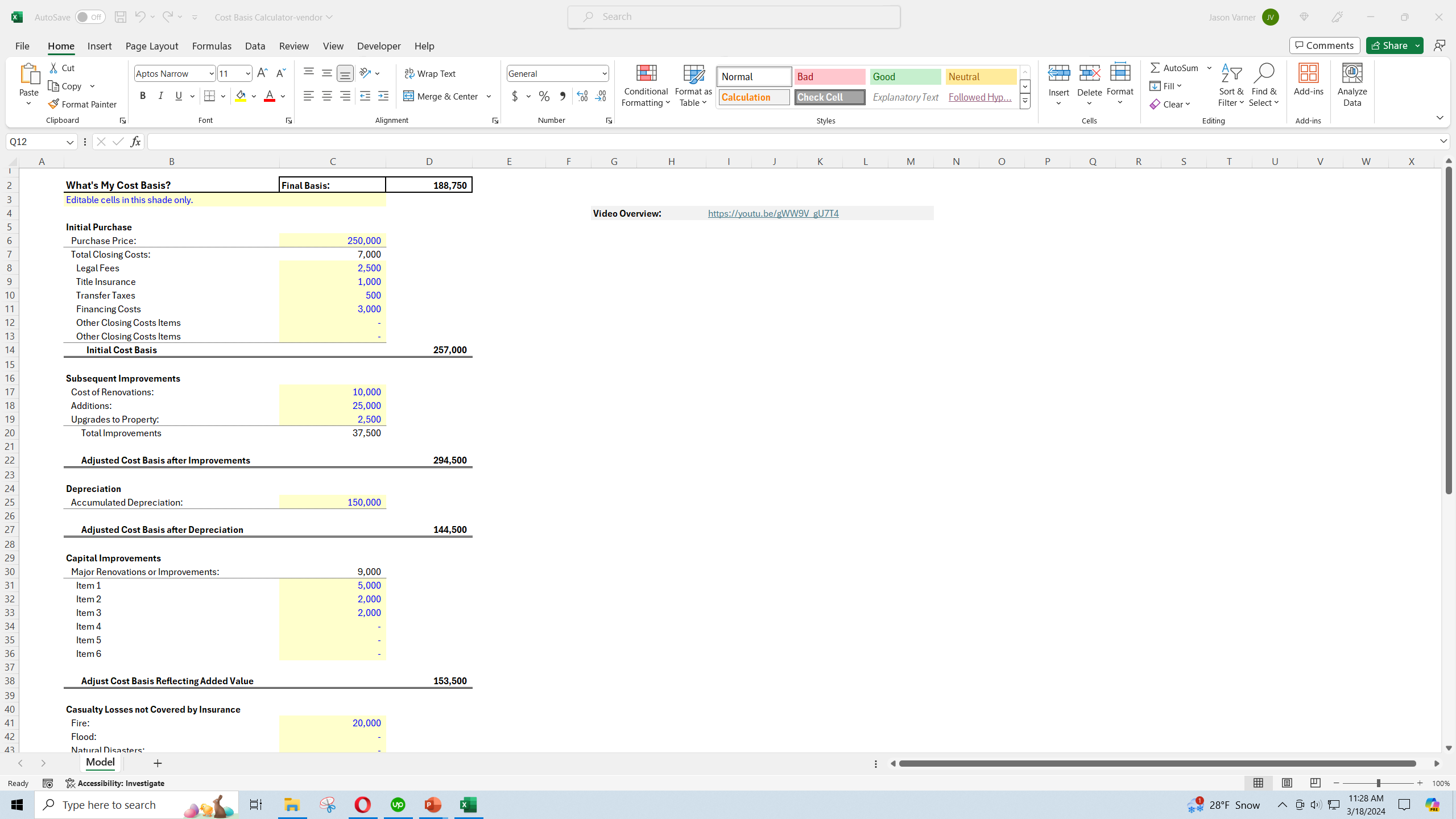

Adjusted Cost Basis Helper

This is a nice tool to organize the components for the final cost basis of a piece of property, equipment, or building.

Further information

Calculate the adjusted cost basis of a fixed asset.

General assets.