Originally published: 30/09/2021 07:42

Last version published: 27/12/2023 09:25

Publication number: ELQ-77059-6

View all versions & Certificate

Last version published: 27/12/2023 09:25

Publication number: ELQ-77059-6

View all versions & Certificate

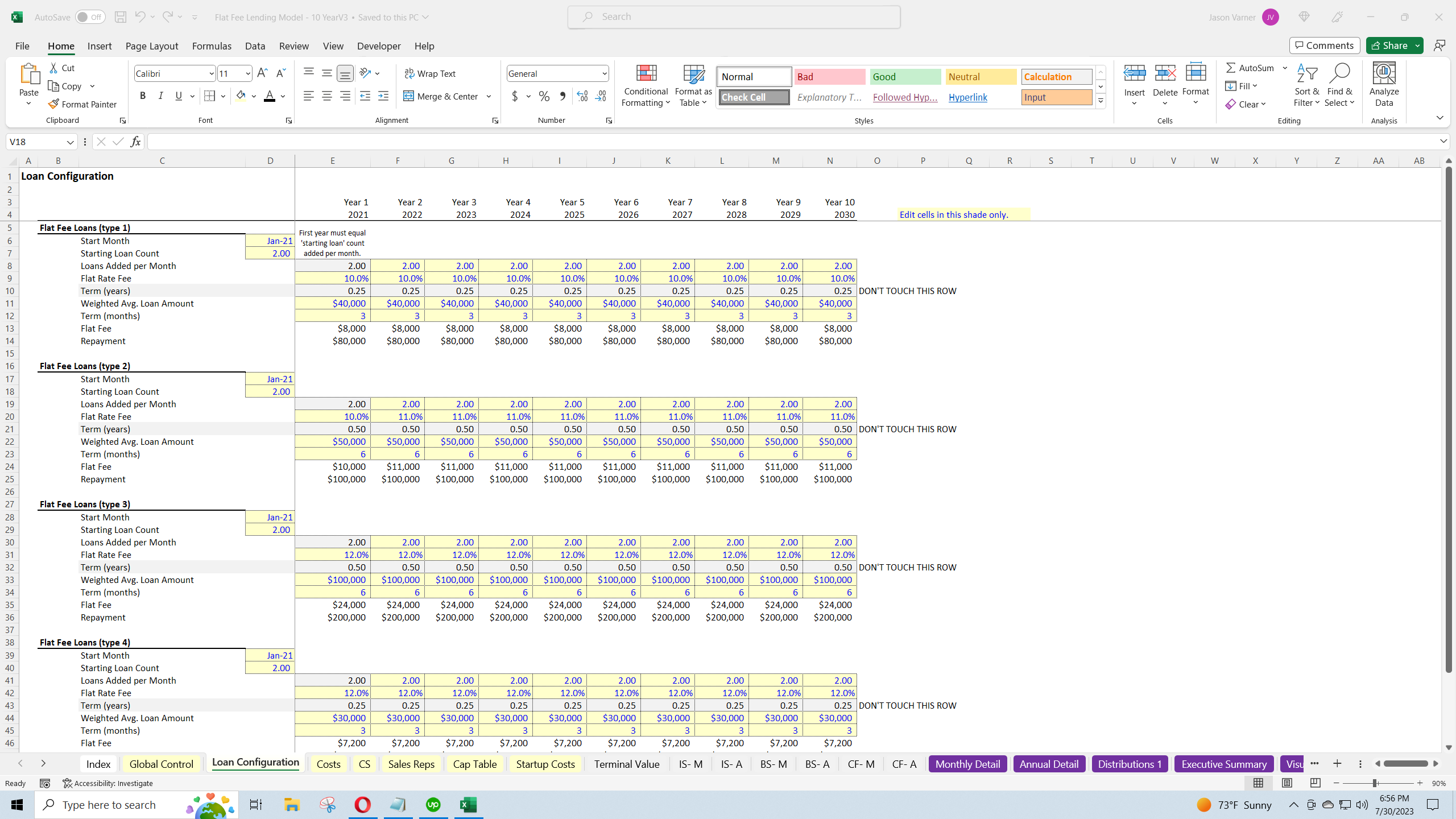

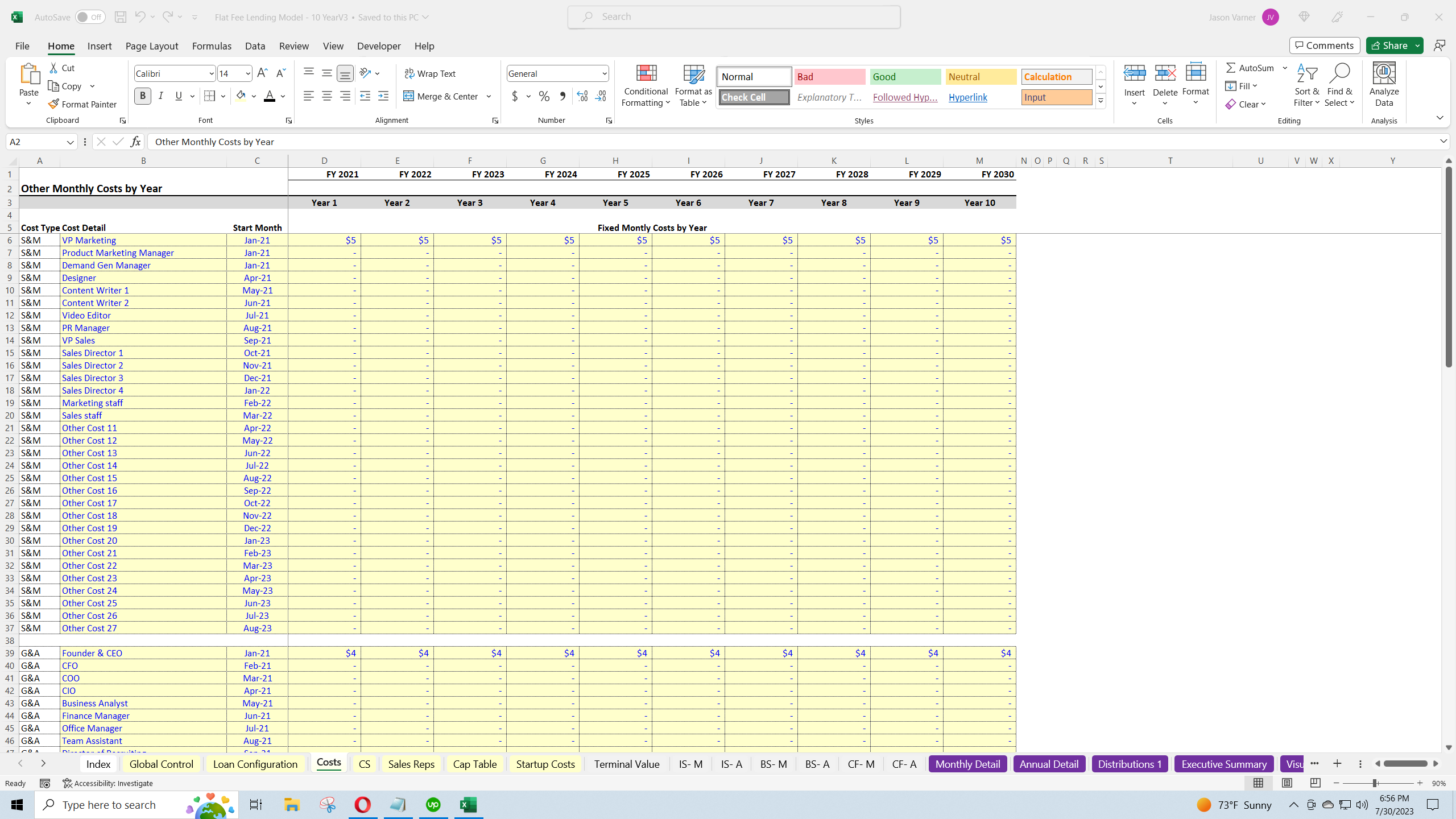

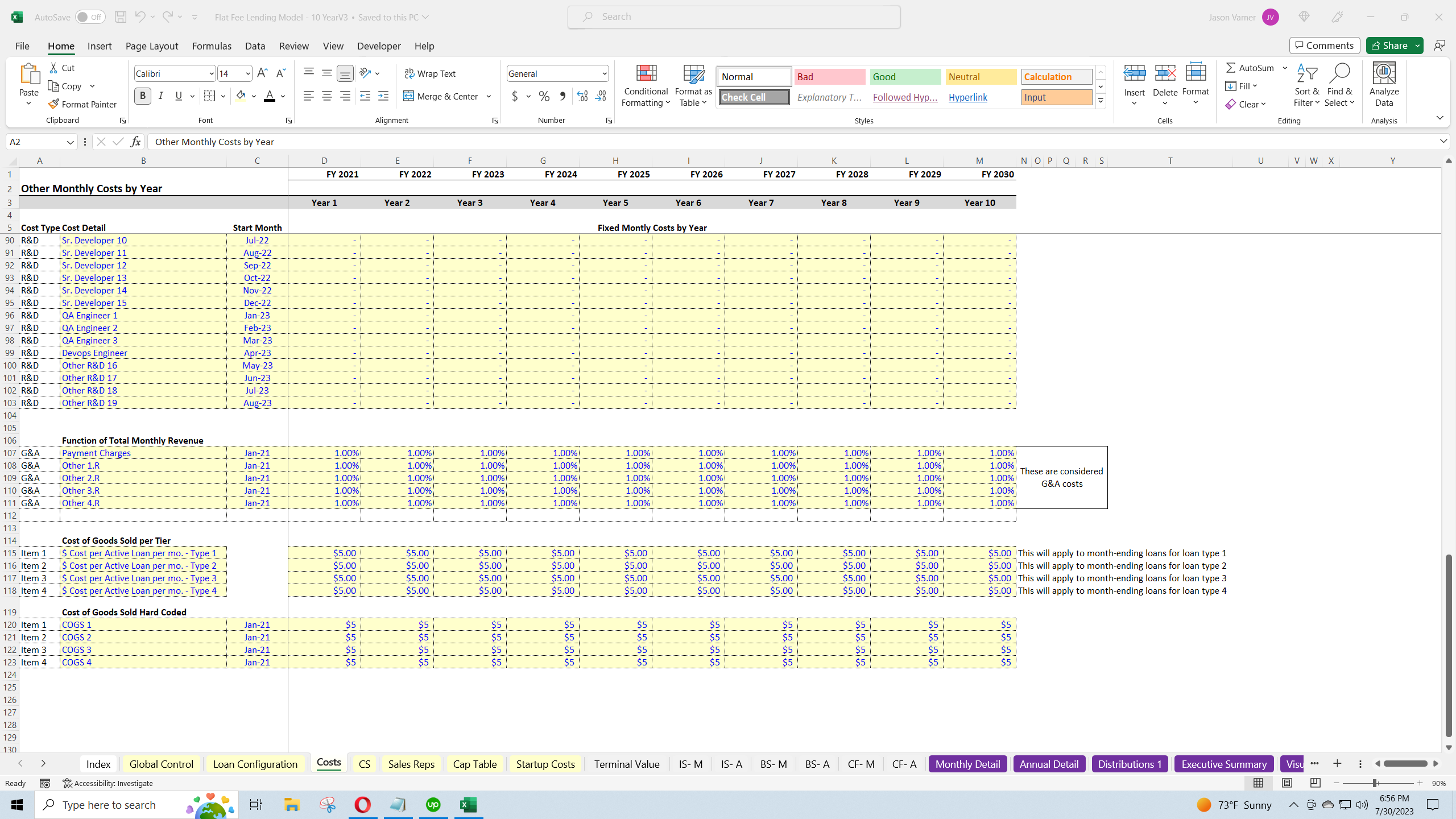

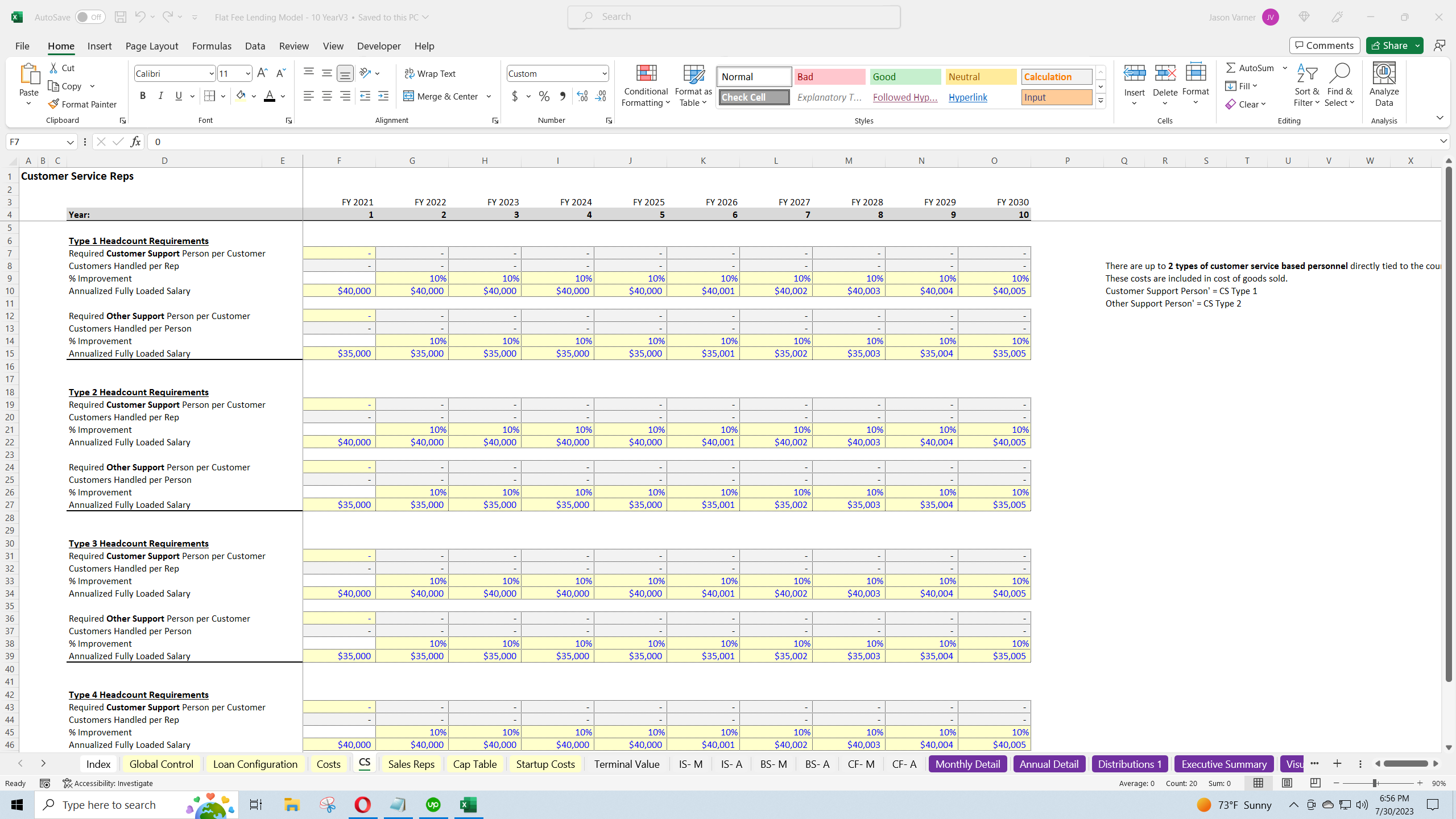

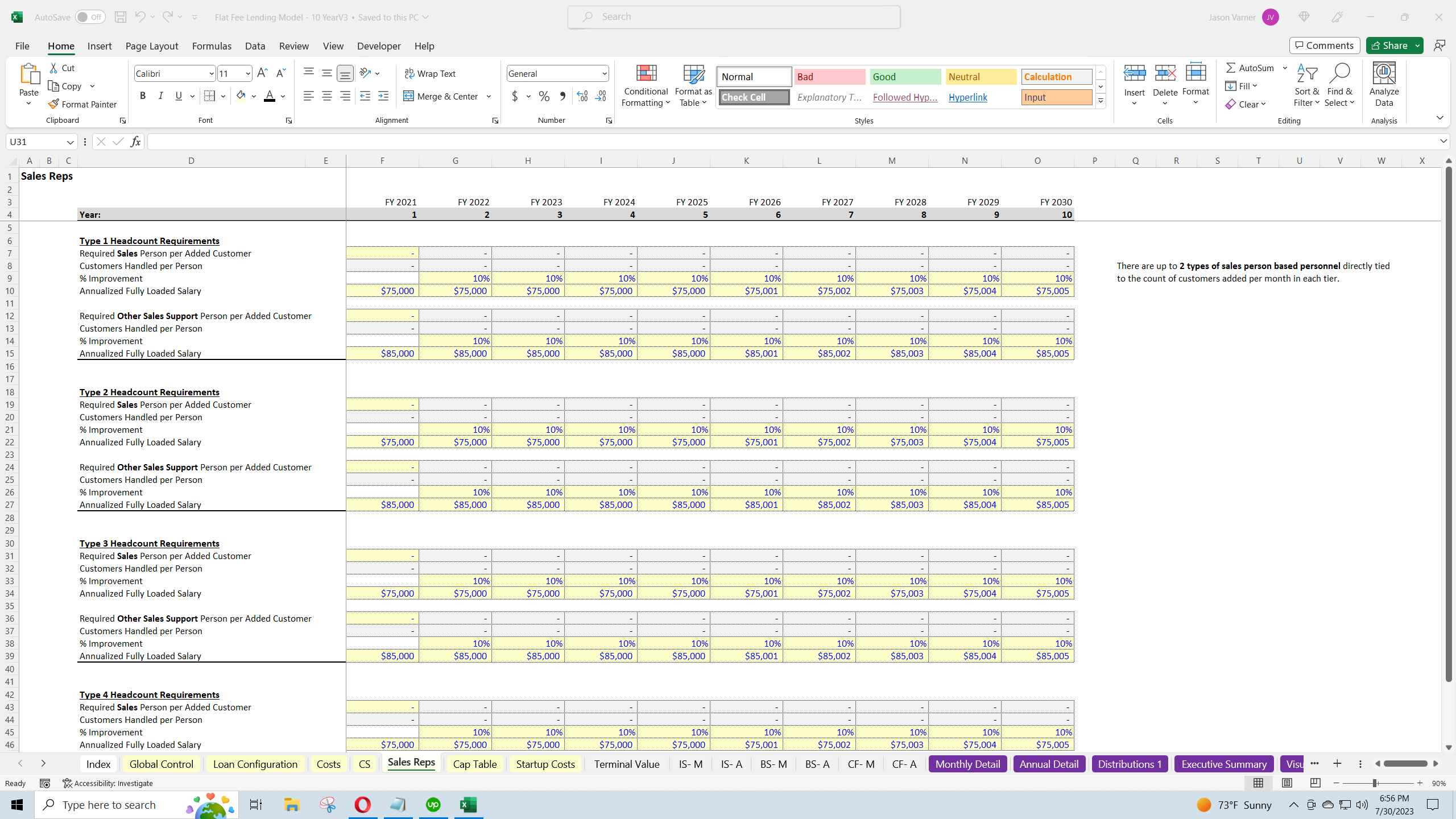

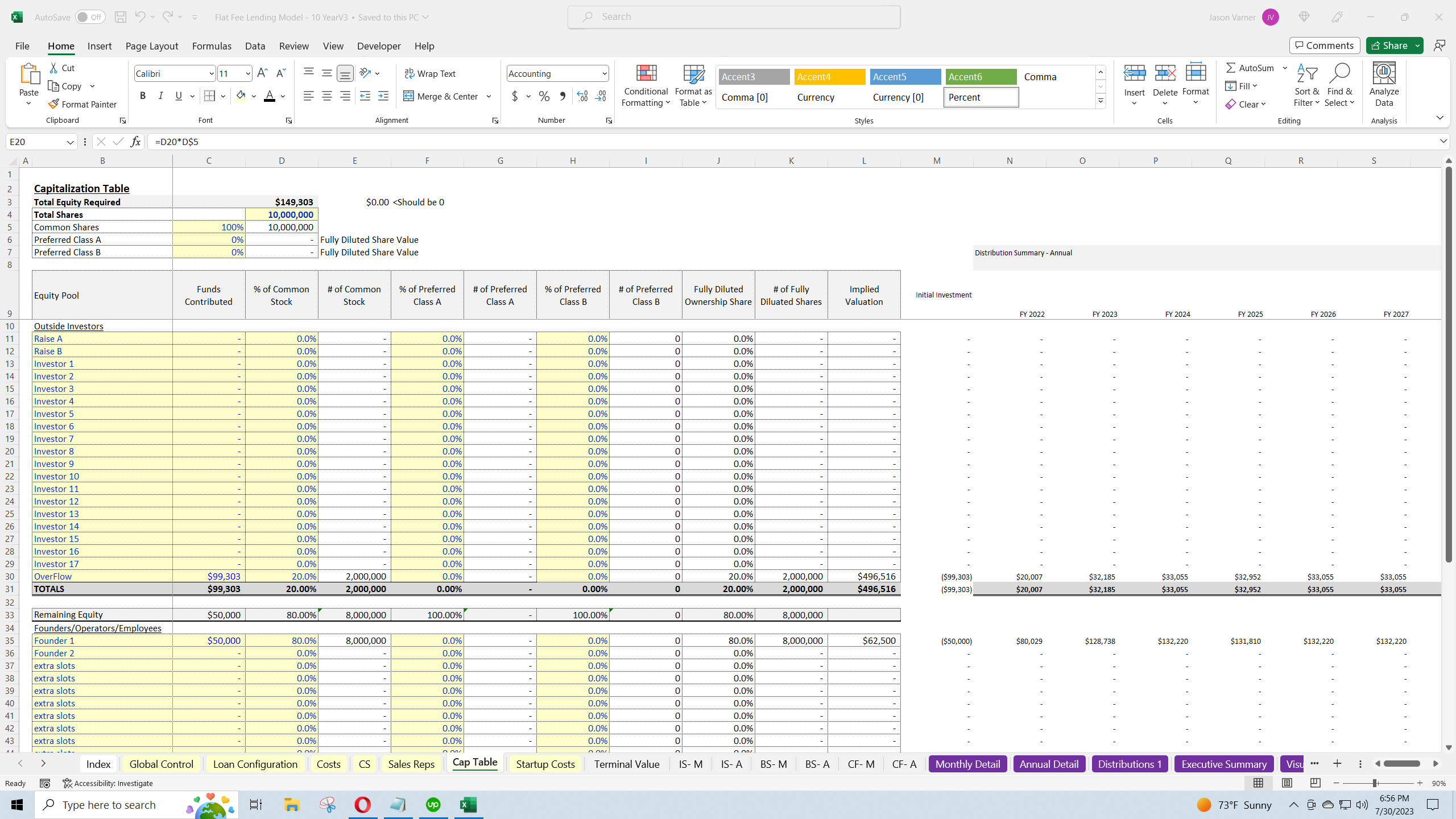

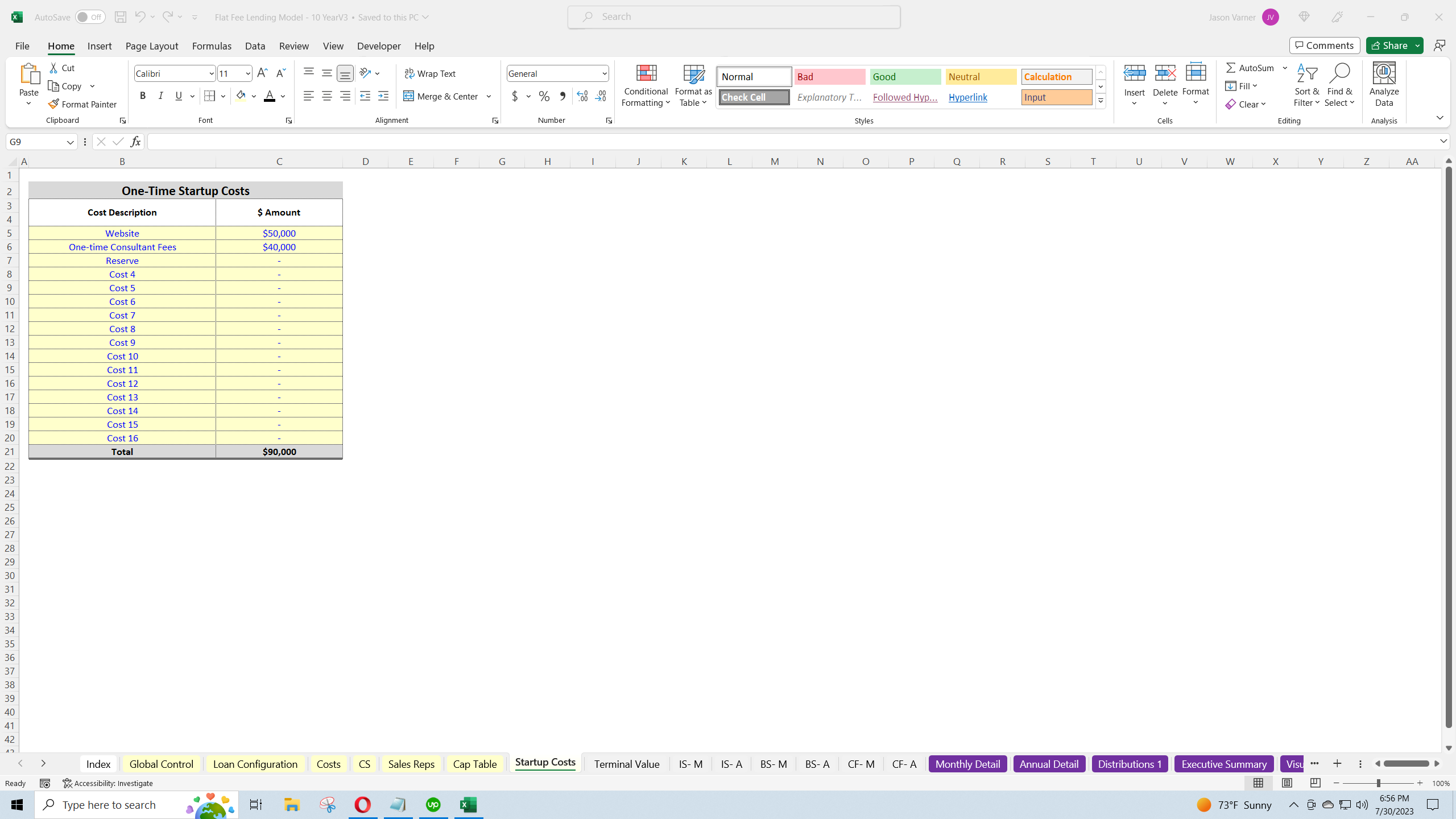

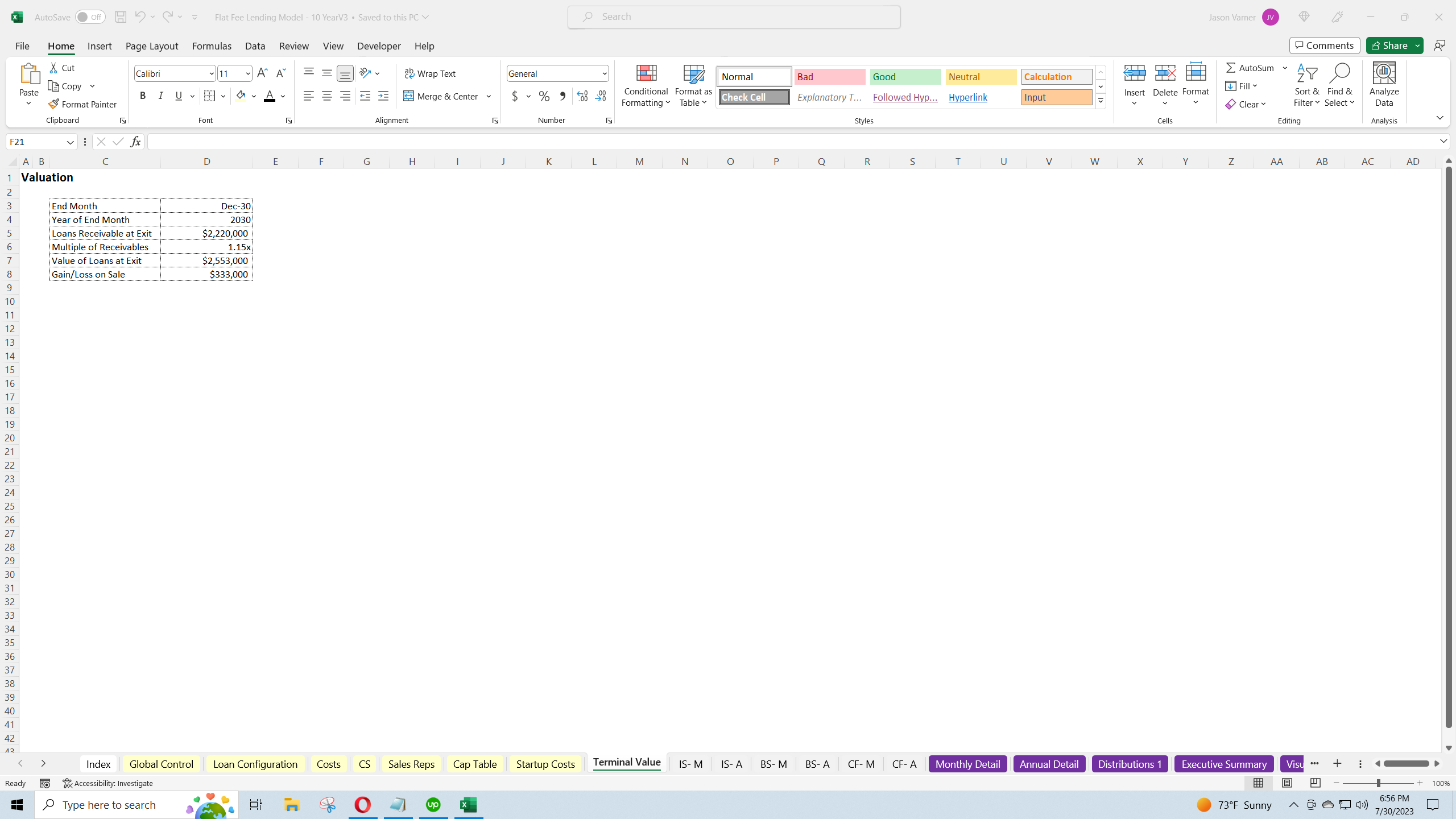

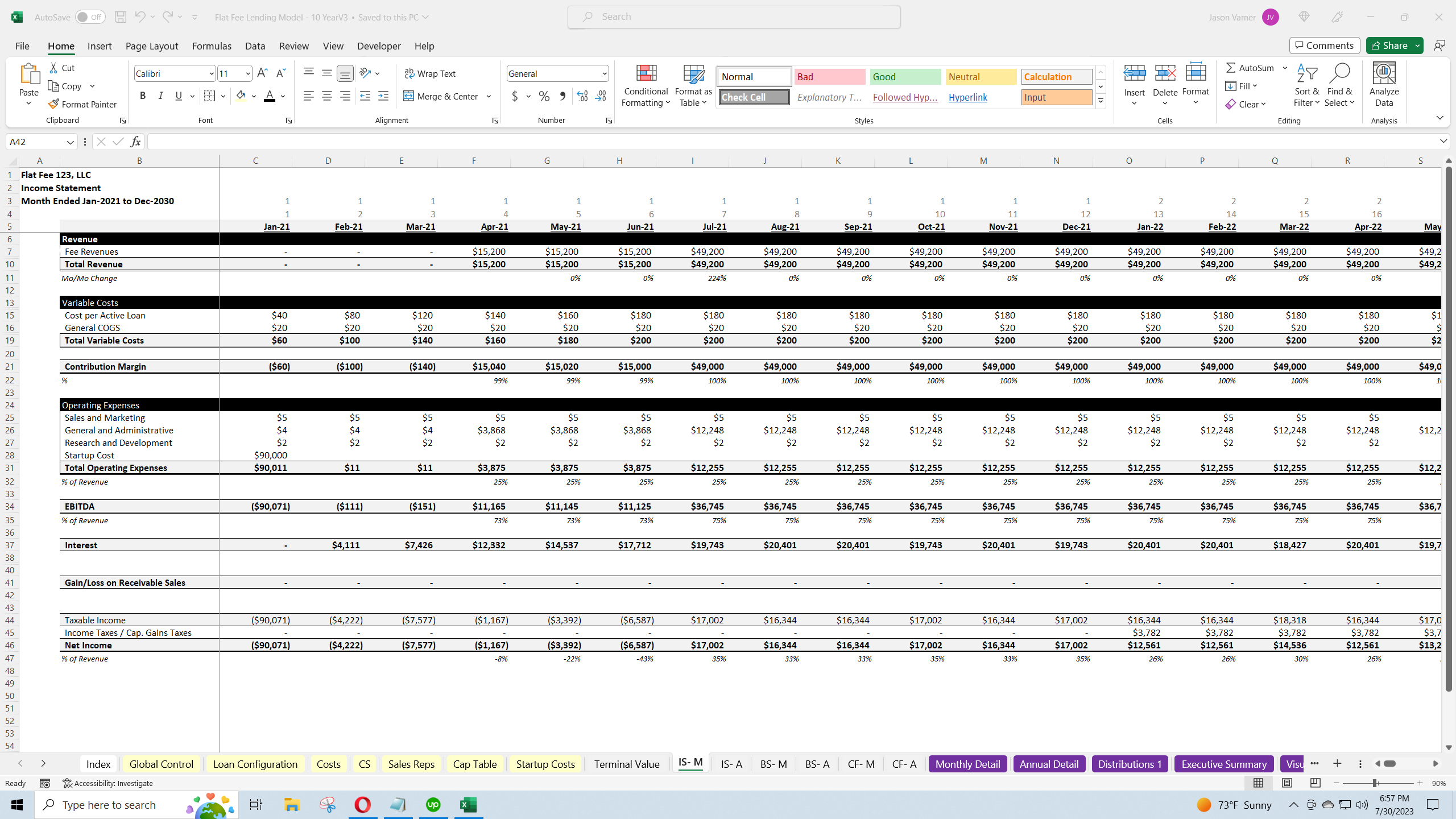

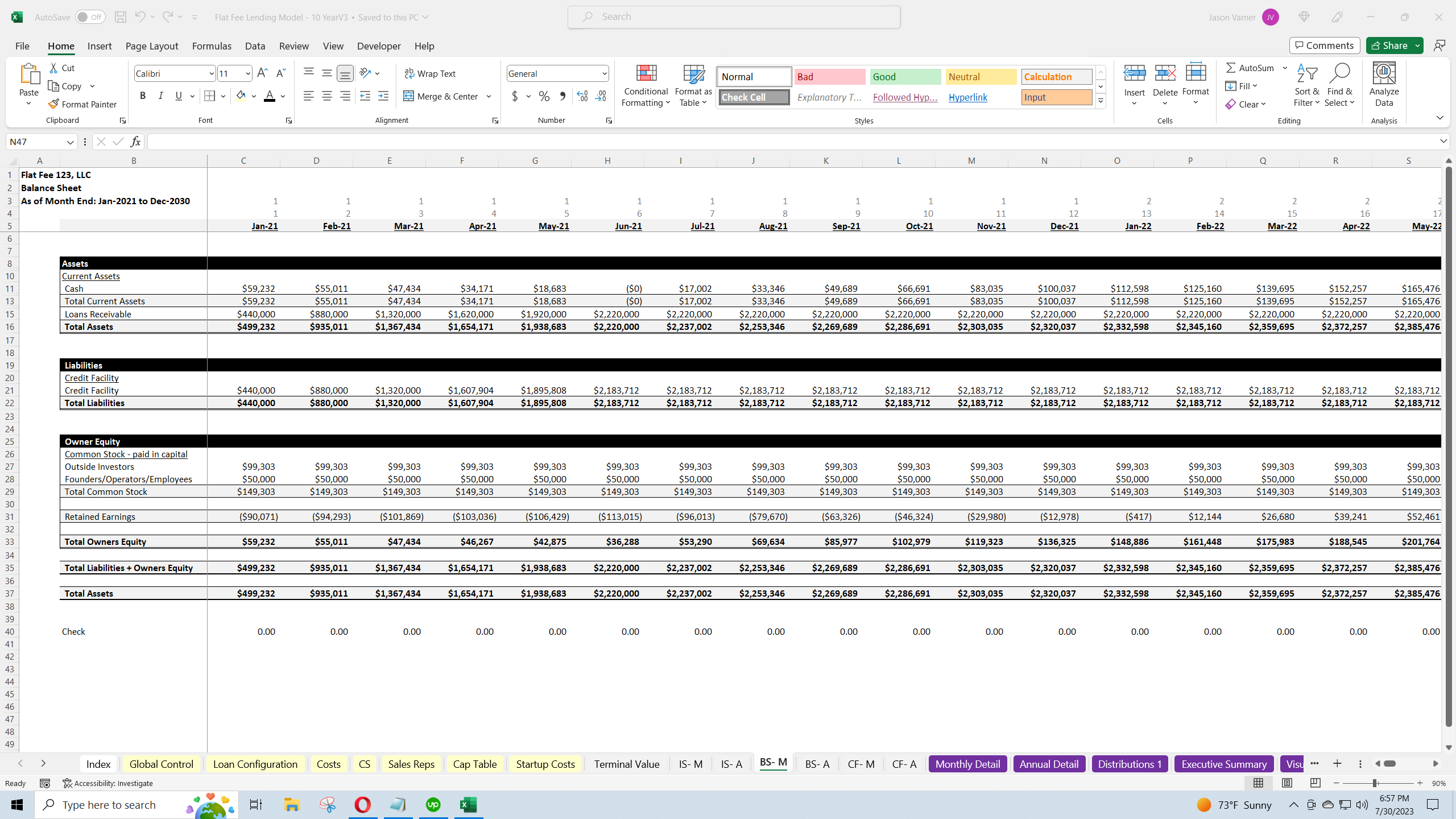

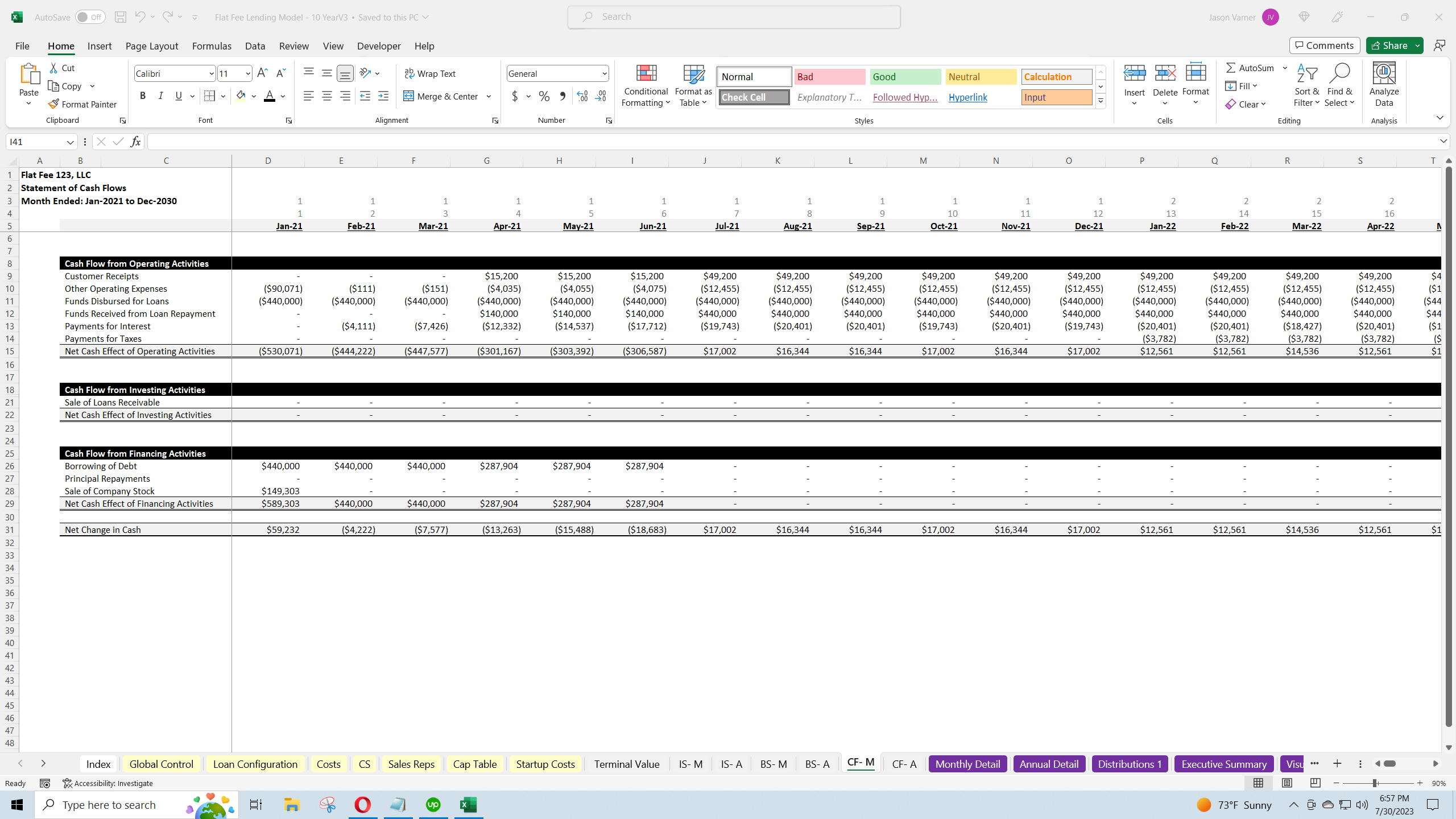

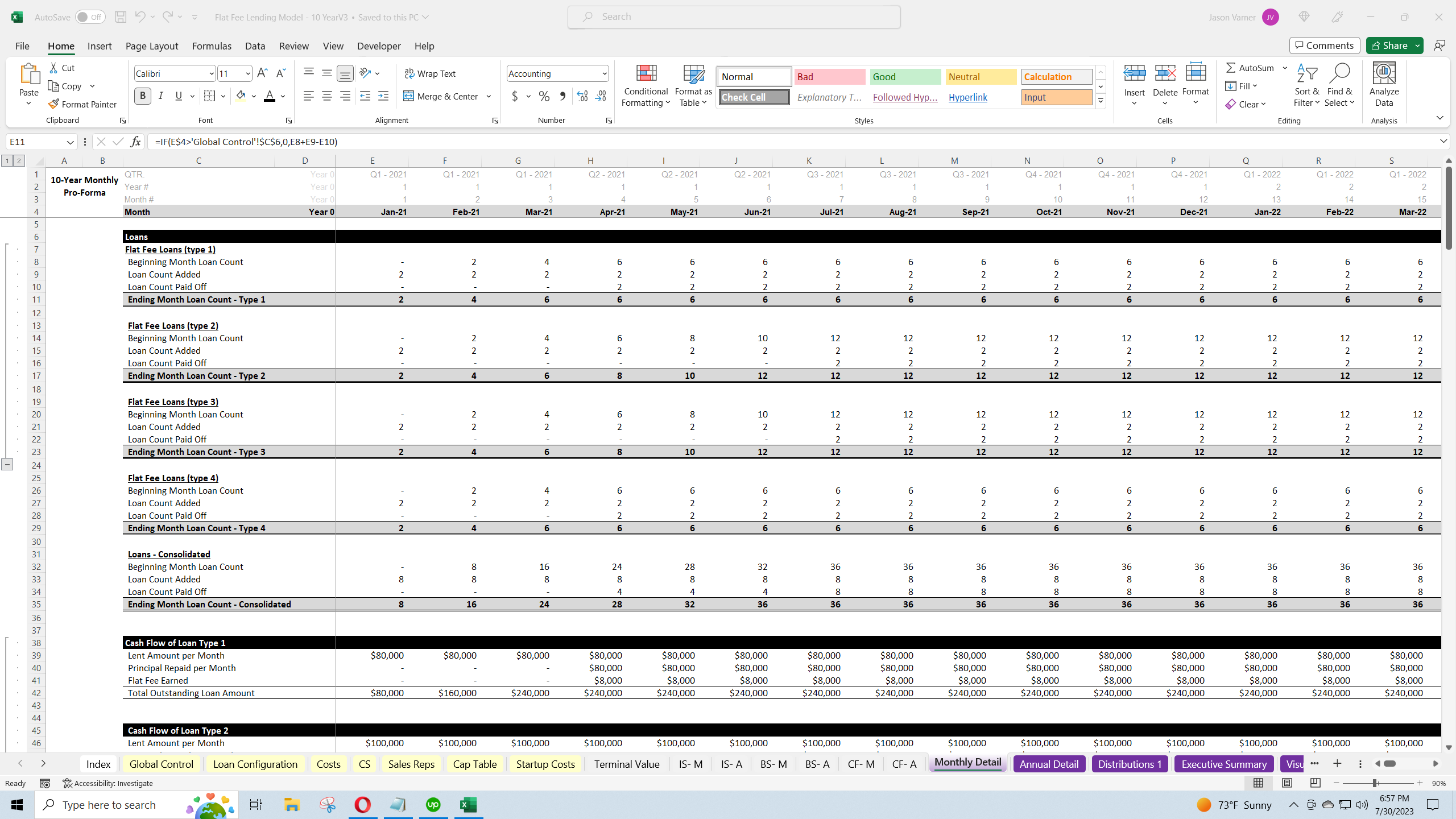

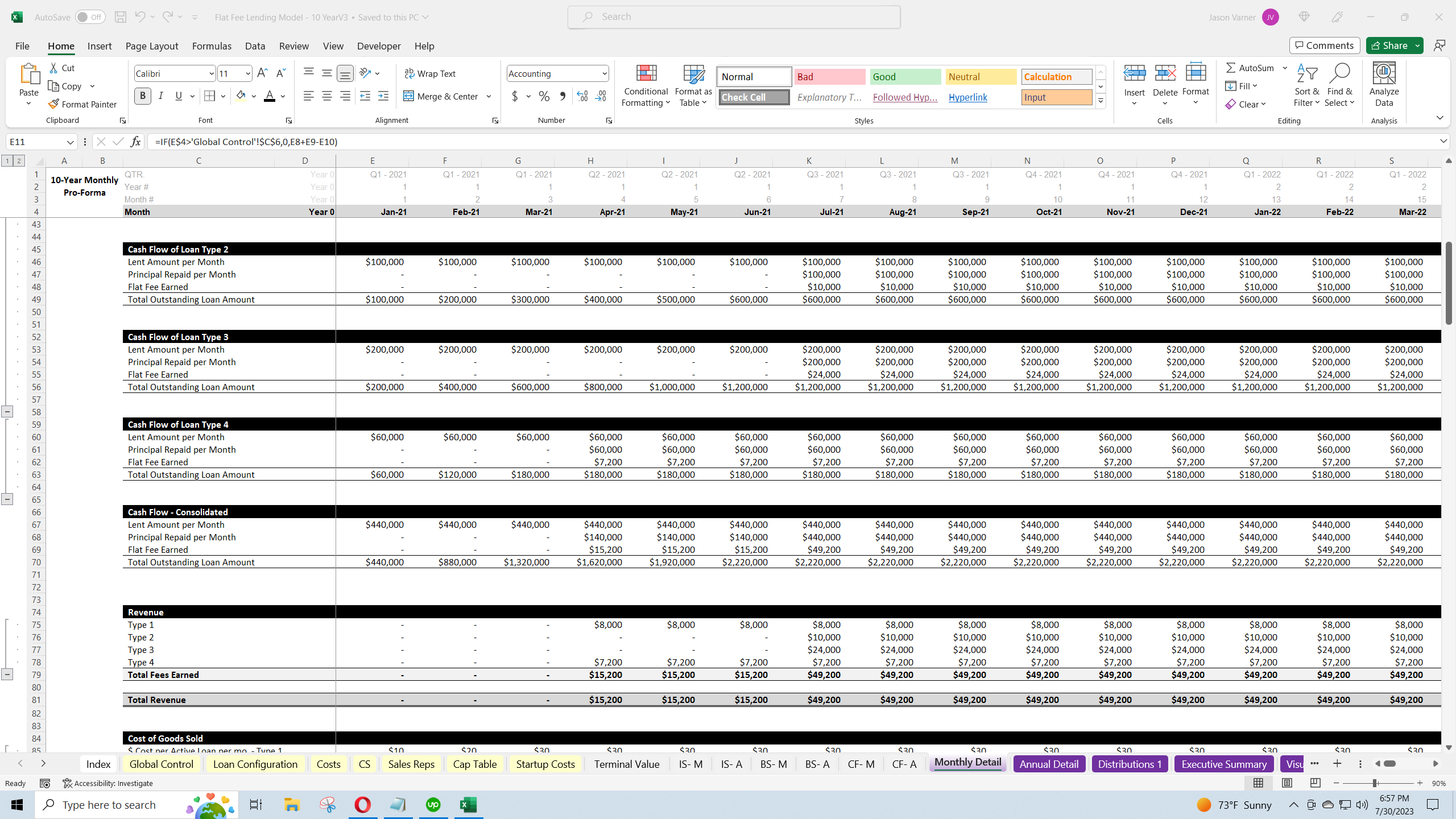

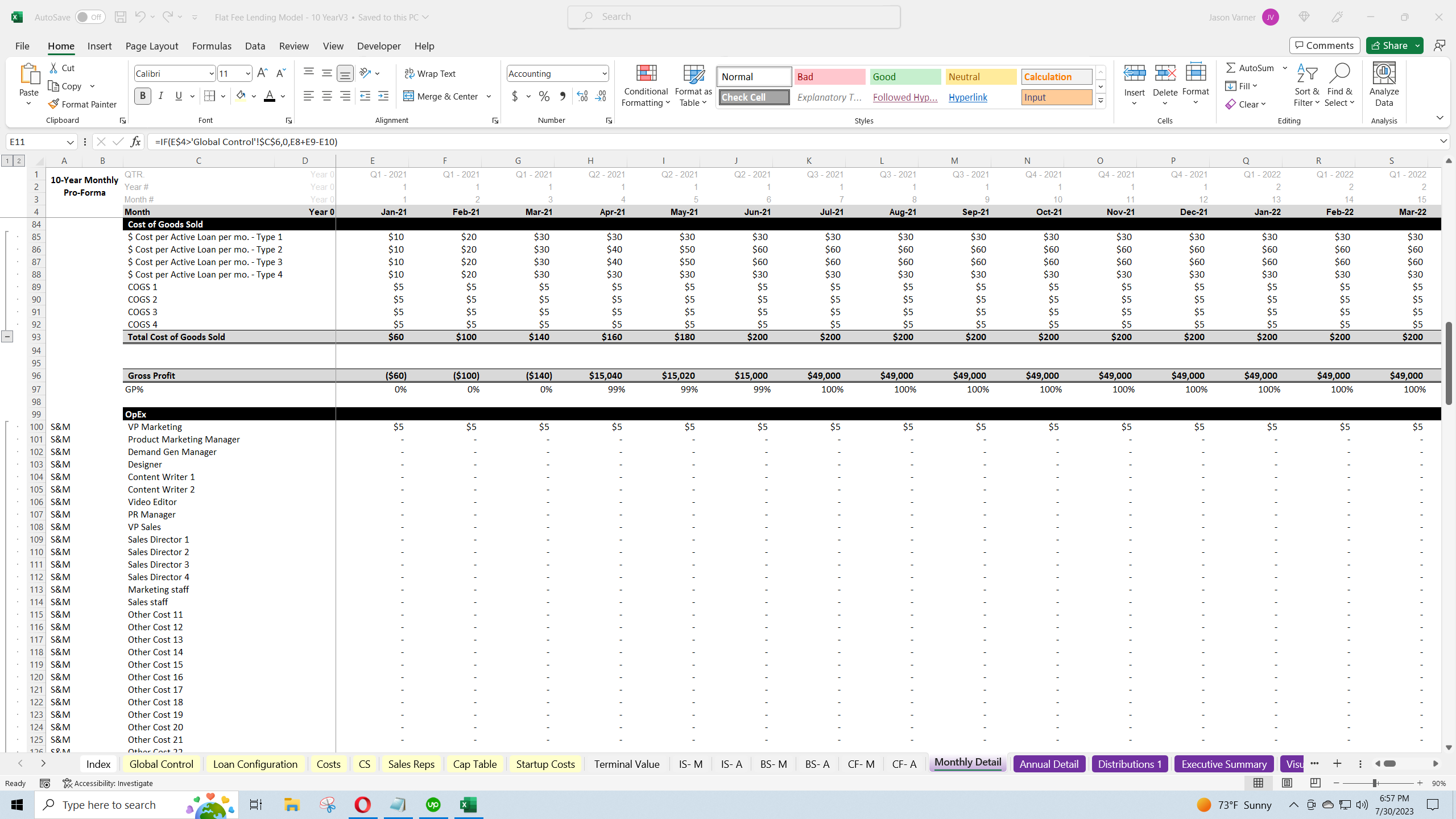

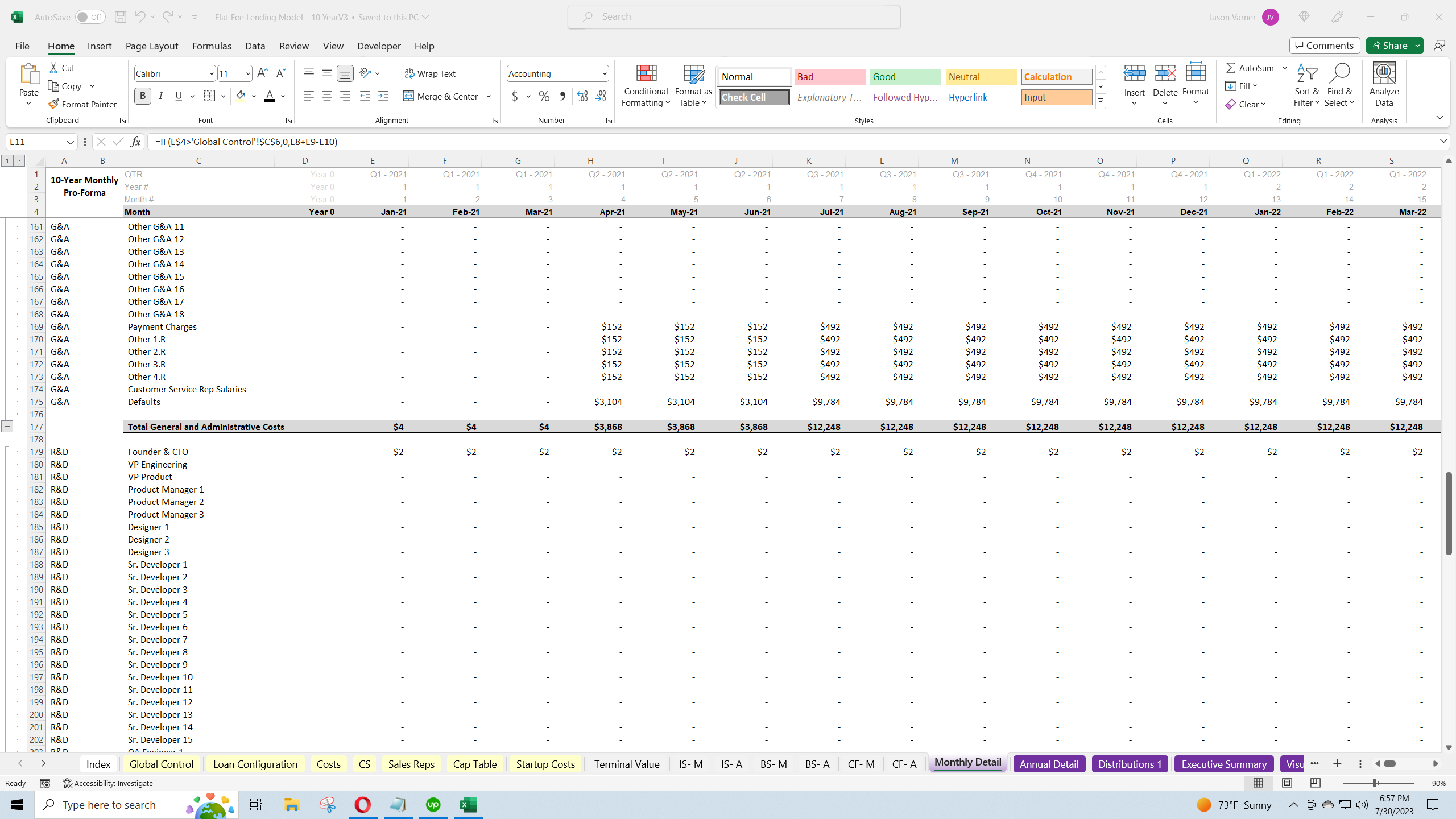

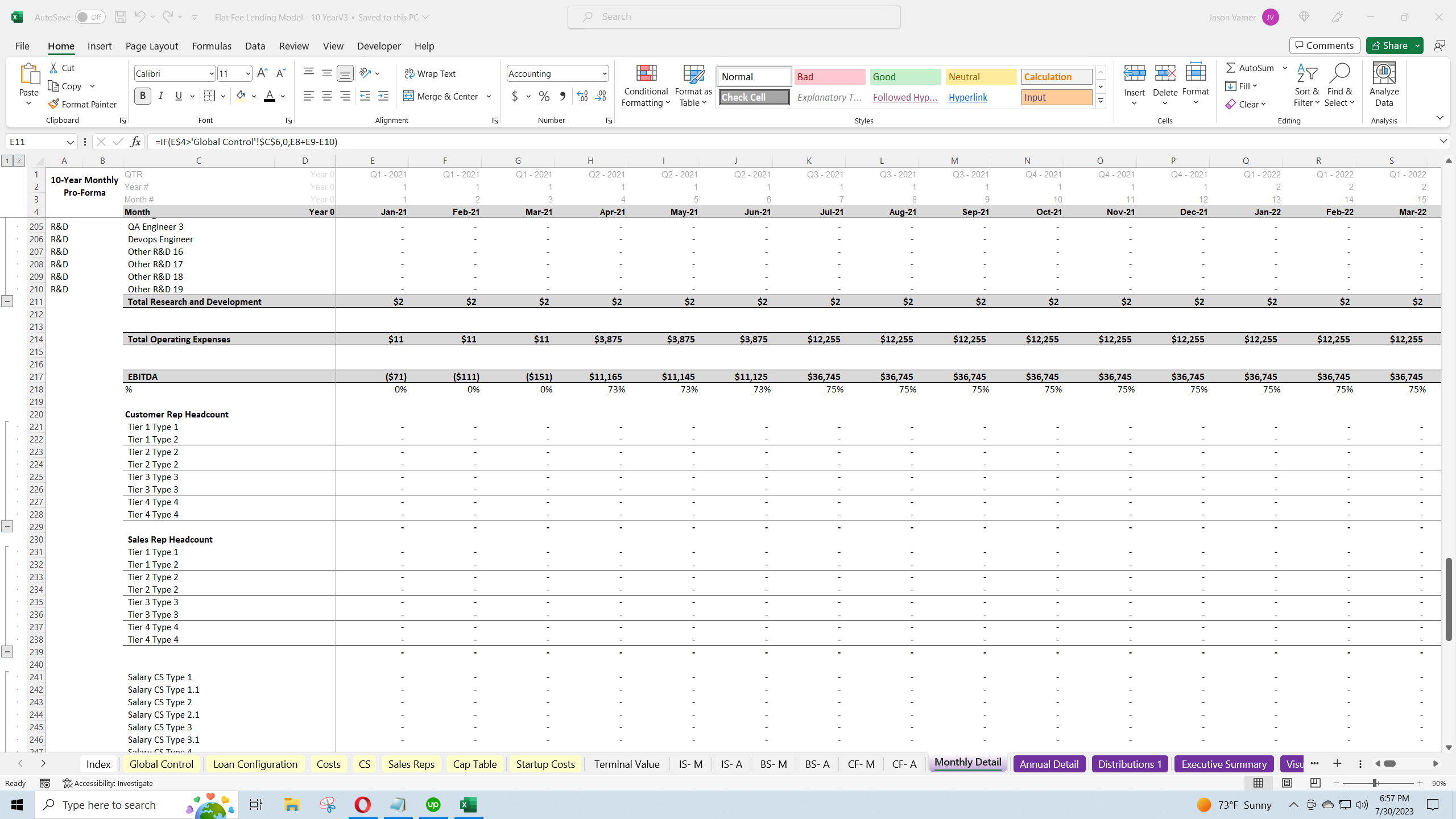

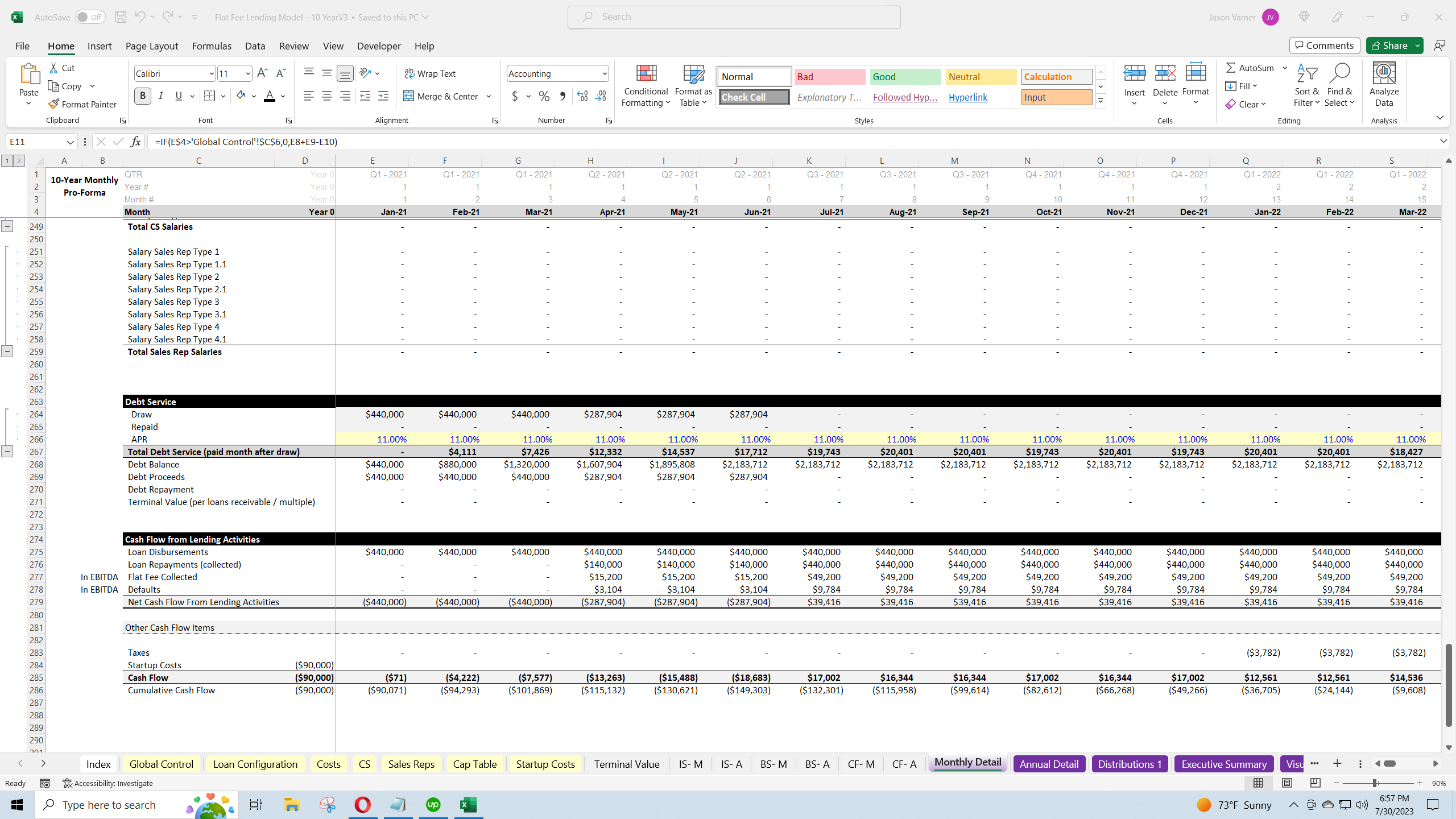

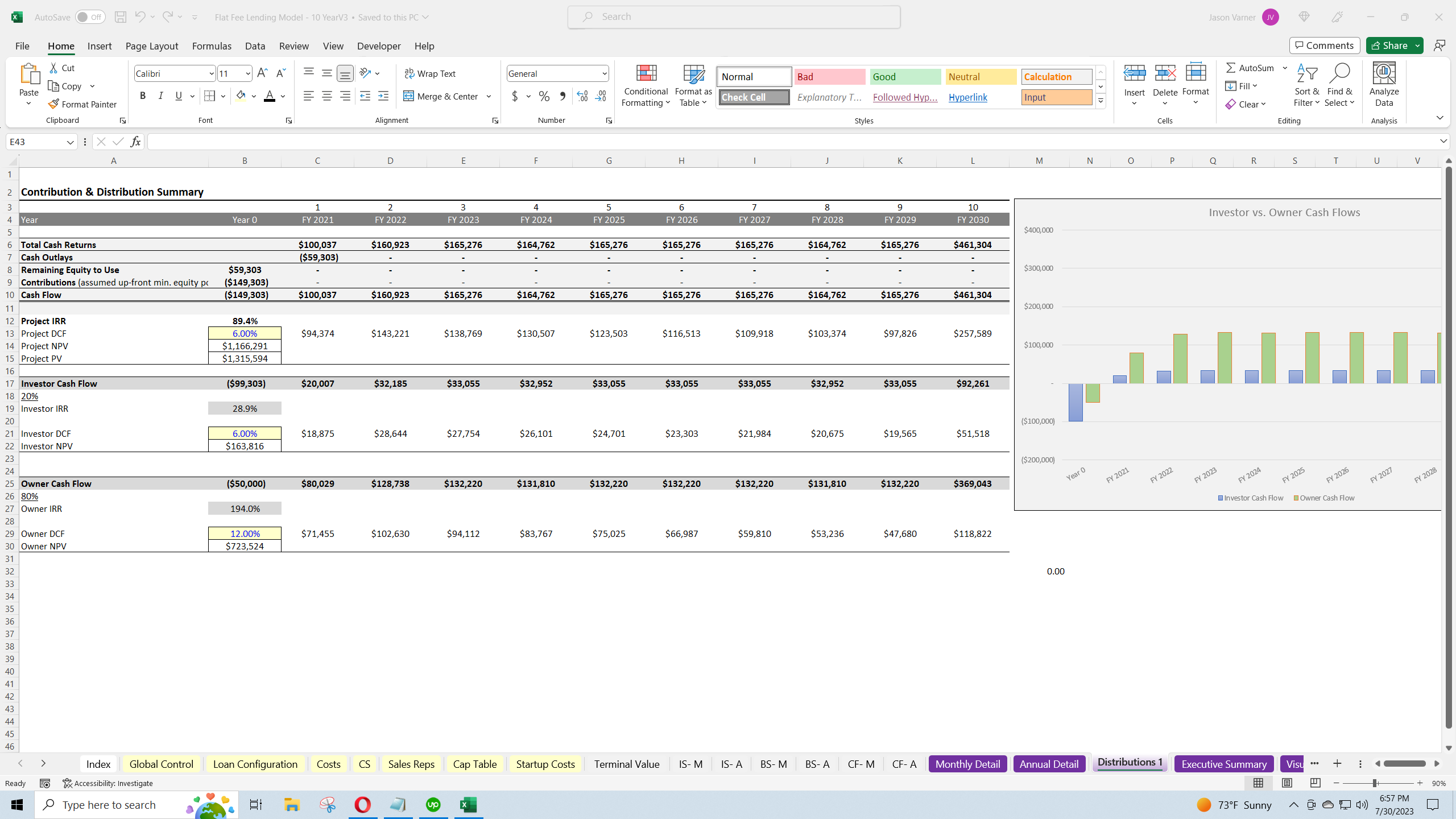

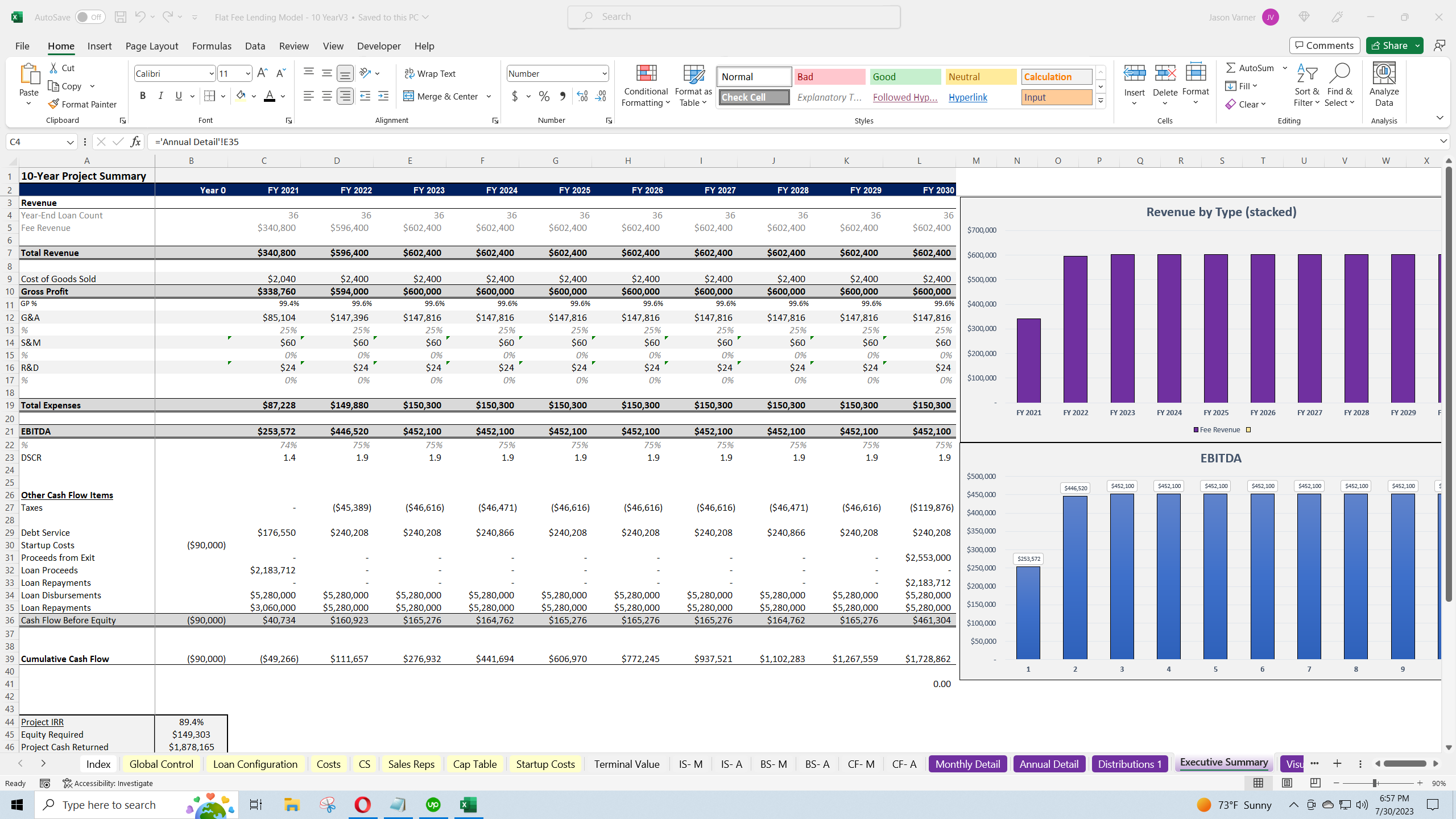

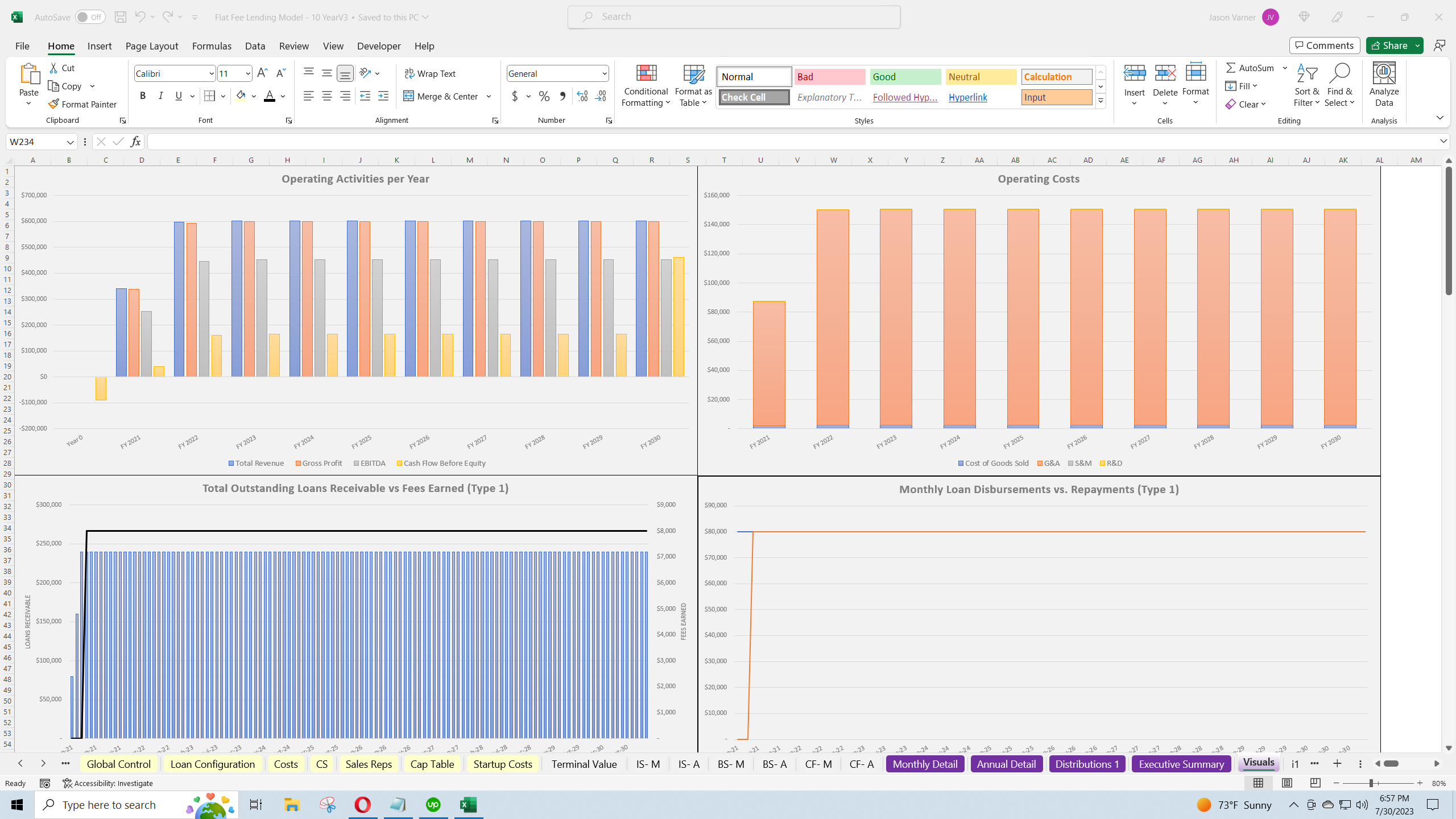

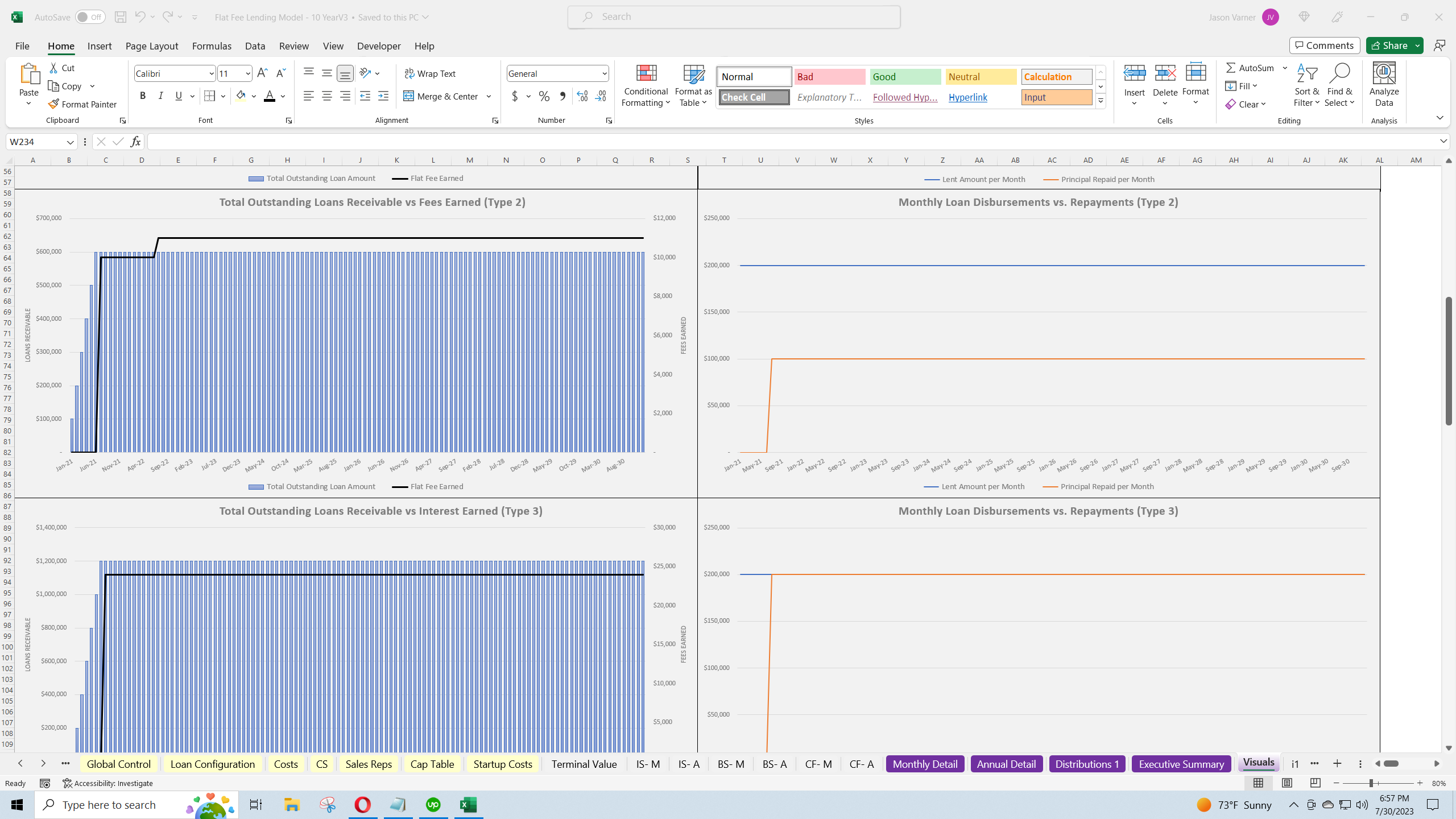

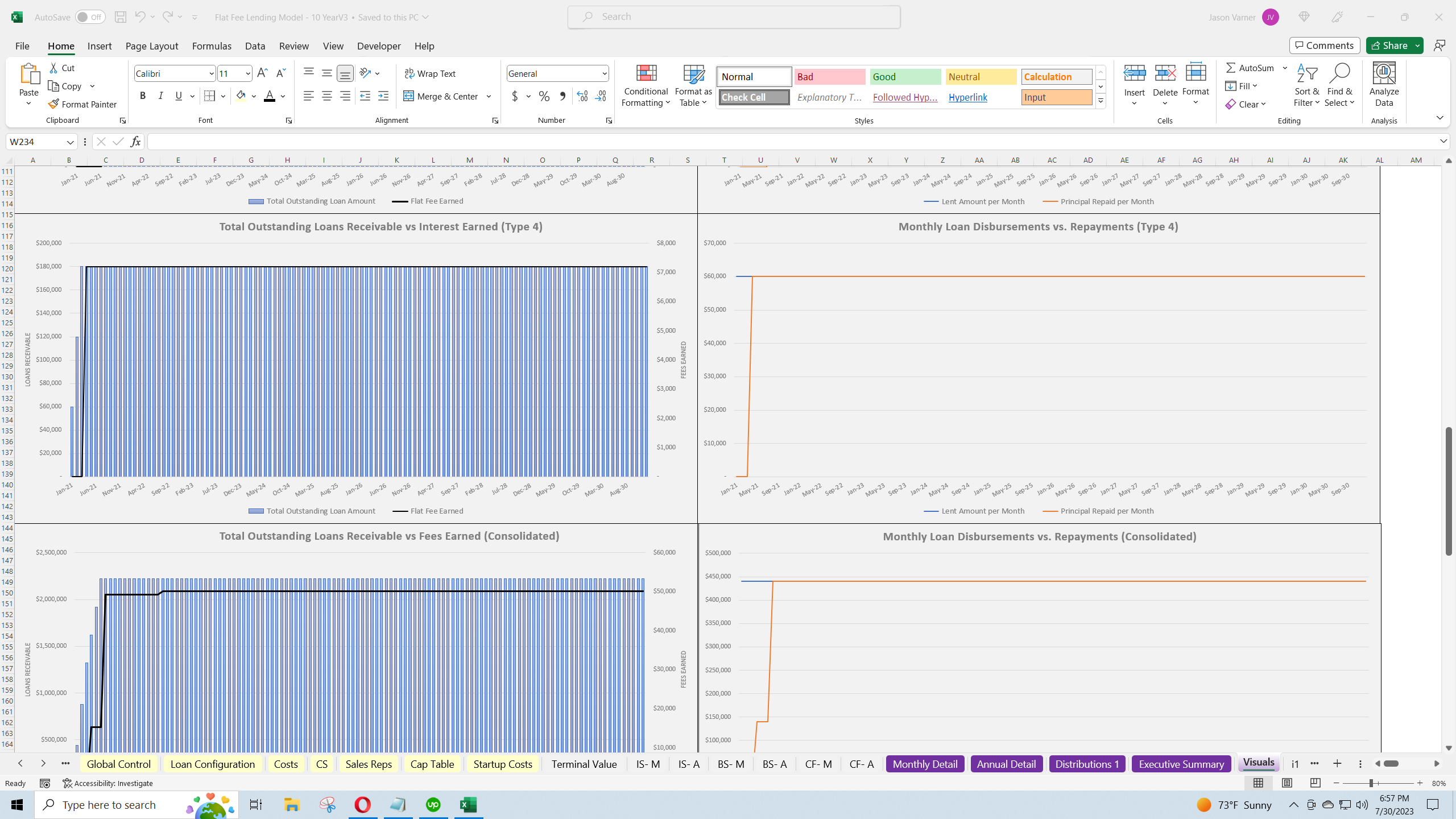

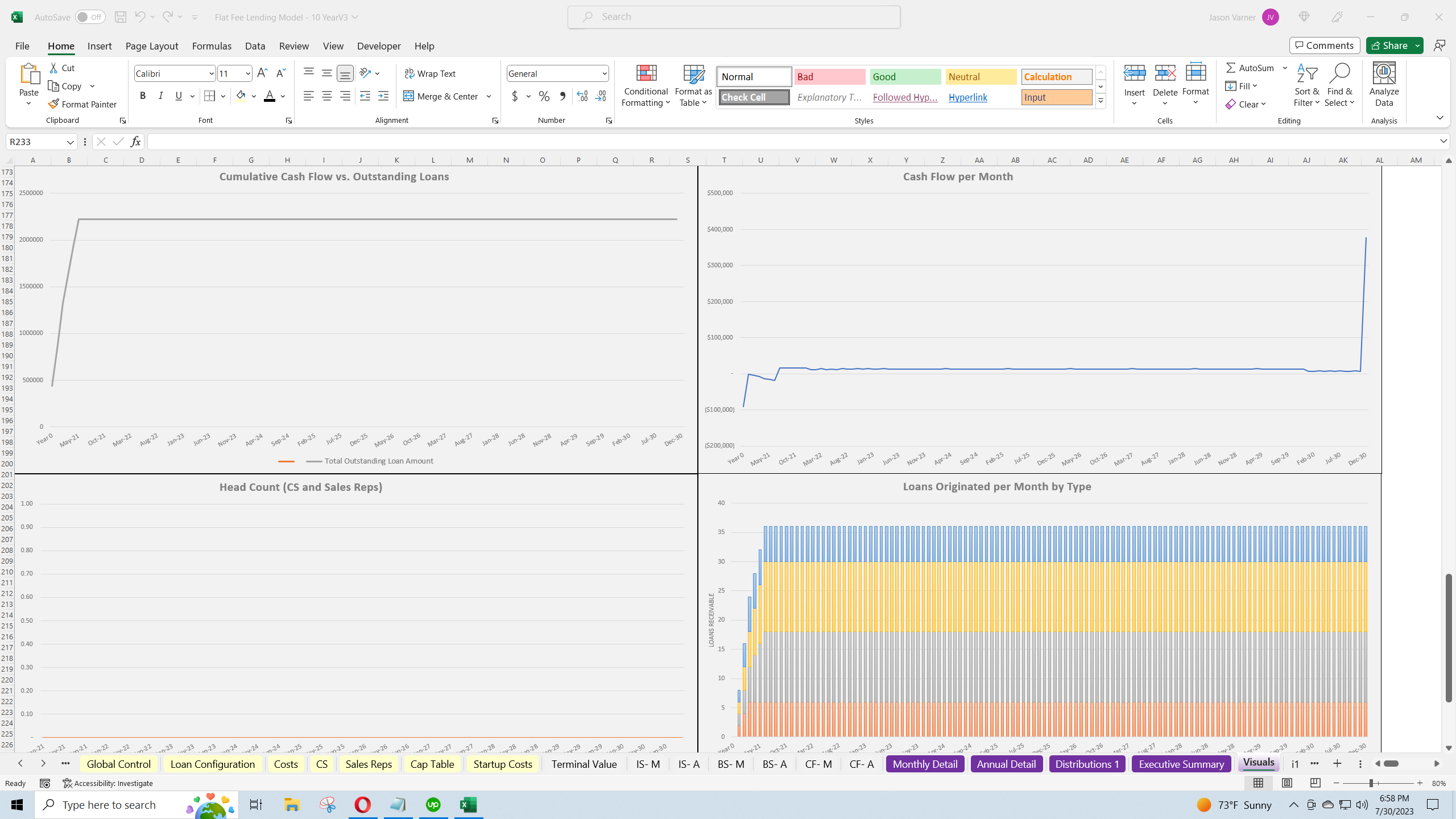

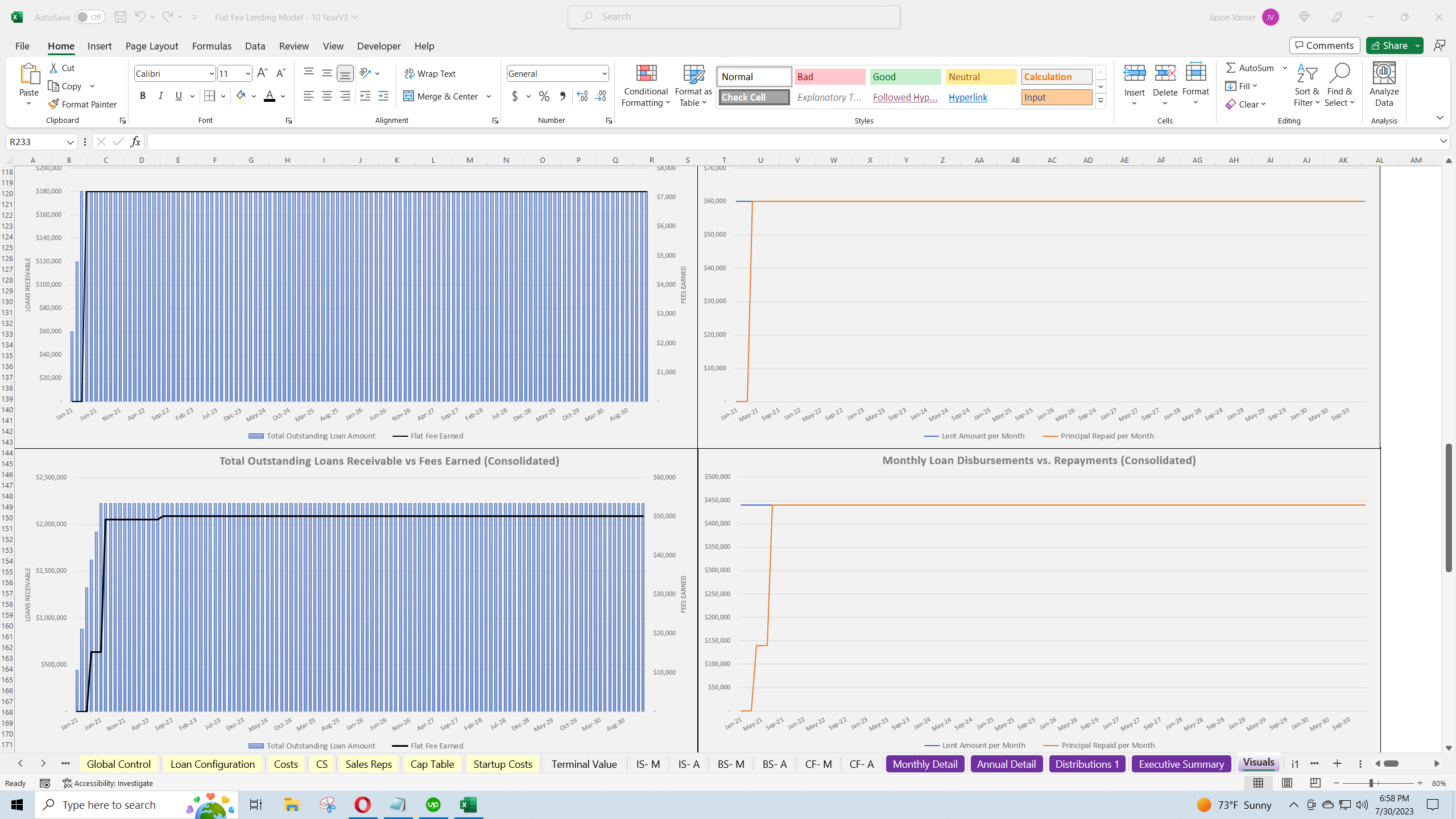

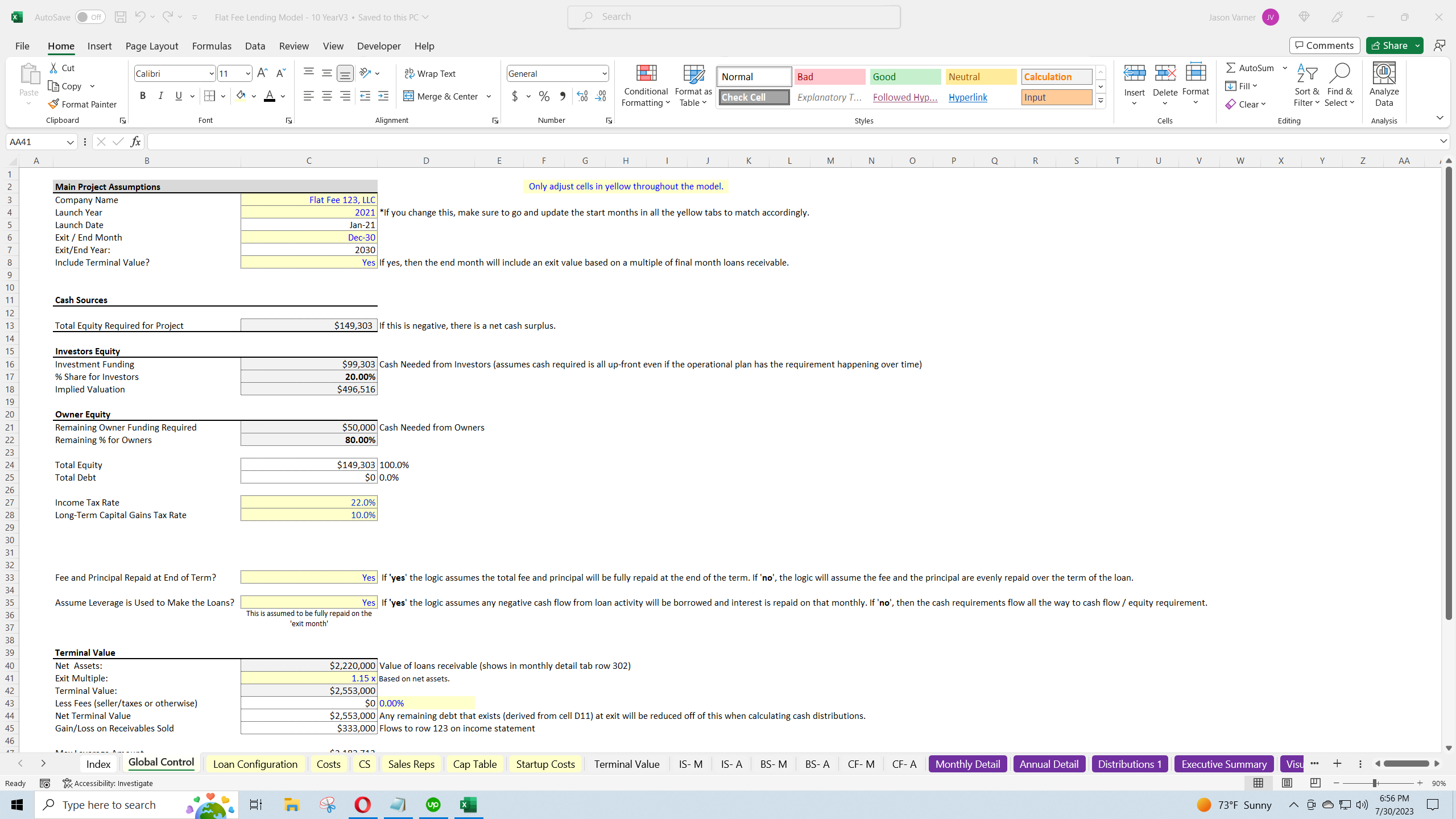

Flat Fee Lending Business: Startup Financial Model

Focusing on the specific logic and configurations required for the financial forecast of a flat fee lending business. Includes three statement model.

Further information

Input assumptions directly related to the flat fee lending business model and automatically produce a financial forecast for up to 10 years.

Flat fee / fixed fee lending businesses.